Just_Super

If voting made any difference they wouldn’t let us do it.”― Mark Twain

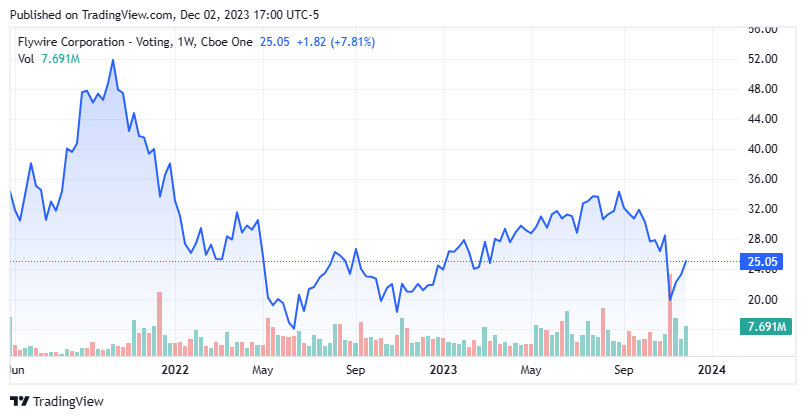

Today, we put Flywire Corporation (NASDAQ:FLYW) in the spotlight for the first time. This fast-growing integrated payment processor is down from the levels it came public at in 2021. However, Flywire is posting impressive sales growth and moving quite nicely towards consistent profitability. An analysis follows below.

Seeking Alpha

Company Overview:

This payments enablement and software company is headquartered in Boston, MA. Flywire provides a payment platform and network, and vertical-specific software that enable clients to get paid and helps their customers to buy from their clients. This platform helps ease payment flows across multiple currencies, payment types, and payment options; and provides direct connections to alternative payment methods, such as Alipay, Boleto, PayPal/Venmo, and Trustly.

Company Website Company Website

The company offers integrated digital solutions for domestic and cross-border payments. Flywire supports more than 3,500 clients via different payment methods in more than 140 currencies across 240 countries and territories. The stock trades for just north of $25.00 a share and sports an approximate market capitalization of $2.8 billion.

The company is particularly focused on growing in the education, healthcare, and travel sectors and enabling B2B transactions. Flywire continues to make small strategic acquisitions towards building out its platform and customer base. Flywire purchased Cohort Go, an international education payments provider, in the summer of 2022 and last month acquired StudyLink, an Australian provider of international student admissions, application, and agent management software.

Third Quarter Results:

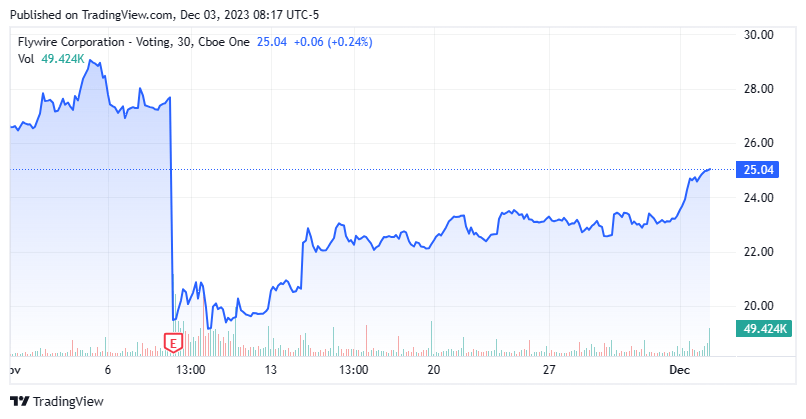

The company posted its Q3 numbers on November 7th. Flywire Corporation delivered a GAAP profit of 8 cents a share as revenues rose just under 30% on a year-over-year basis to $123.3 million. Net income for the quarter was $10.6 million, compared with a loss of $4.3 million in 3Q 2022. Revenue would have been slightly higher if not for the strong dollar. The stock fell sharply on Q3 results but has since recovered a good portion of those losses.

Seeking Alpha

The company’s Total Payment Volume rose 26% from 3Q 2022 to reach $8.9 billion this quarter. Adjusted EBITDA for the quarter increased just over 50% from the same period a year ago to $27.5 million. The company signed 185 new clients in the quarter and was particularly active in the travel sector in this regard. Management provided FY2023 sales guidance of between $394.1 million and $399.3 million.

Analyst Commentary & Balance Sheet:

Since third-quarter results were posted, eight analyst firms including RBC Capital, Wells Fargo and Goldman Sachs have reissued or assigned Buy/Outperform ratings on the stock. Price targets proffered range from $29 to $41 a share. Morgan Stanley has maintained its Hold rating and $27 price target on Flywire Corporation.

Two weeks before third-quarter results hit the wires, UBS initiated a Buy rating on FLYW noting the company’s defensive end markets “are supportive of durable growth in the near-term against an uncertain macroeconomic backdrop” and is also projecting 30% sales growth in 2024 and 2025 and a sales CAGR rate of 25% for 2026-2028.

Approximately six percent of the outstanding float in the shares is currently held short. Several insiders have been frequent and consistent sellers of the stock throughout 2023 and have disposed of just over $1.7 million worth of equity so far in the fourth quarter. Flywire Corporation ended the third quarter with just under $640 million in cash and marketable securities according to the 10-Q filed for the quarter. Flywire has no long-term debt. The company raised some $260 million via a secondary offering in August.

Verdict:

Flywire Corporation lost 36 cents a share in FY2022 on just under $290 million worth of revenue. The current analyst firm consensus has the company paring losses to 15 cents a share in FY2023 as sales rise just past $380 million. In FY2024, they project the company will see a very slight profit as revenues rise to nearly $490 million.

There is a lot to appreciate about Flywire. The company has posted impressive revenue growth and is moving toward consistent profitability. Flywire has a solid balance sheet and no debt. The company should have many years ahead of solid revenue growth, both organically and via small strategic acquisitions.

The question around Flywire as far as investment is about valuation. Is what basically a payment processor worth over seven times likely 2023 sales? Granted, the stock is cheaper if one accounts for the net cash on its balance sheet. I am on the fence around Flywire. If the shares fell back to the $20 level, I would probably establish a starter position in this name, but I am not going to chase the recent rally for now.

A government big enough to give you everything you want is a government big enough to take from you everything you have.”― Gerald R. Ford

Q2 2024 Earnings Call Transcript")