SweetBunFactory

If you ask me what I came to do in this world, I, an artist, will answer you: I am here to live out loud.”― Émile Zola.

Today, we put Amphastar Pharmaceuticals, Inc. (NASDAQ:AMPH) in the spotlight for the first time. The stock has more than doubled over the past 12 months. The stock got a nice boost from third quarter results as well as the overall rebound in the markets since late October. Insider selling also notably picked up in the month of November. Where will the stock go from here? An analysis follows below.

Seeking Alpha

Company Overview:

August Company Presentation

This drug manufacturer is located just east of Los Angeles in Rancho Cucamonga, CA and operates with two primary business units: Finished Pharmaceutical Products and Active Pharmaceutical Ingredient (API). The company develops, manufactures, and sells generic and proprietary injectable, inhalation, and intranasal products. The stock currently trades just over $58.00 a share and sports an approximate market capitalization of $2.8 billion.

August Company Presentation

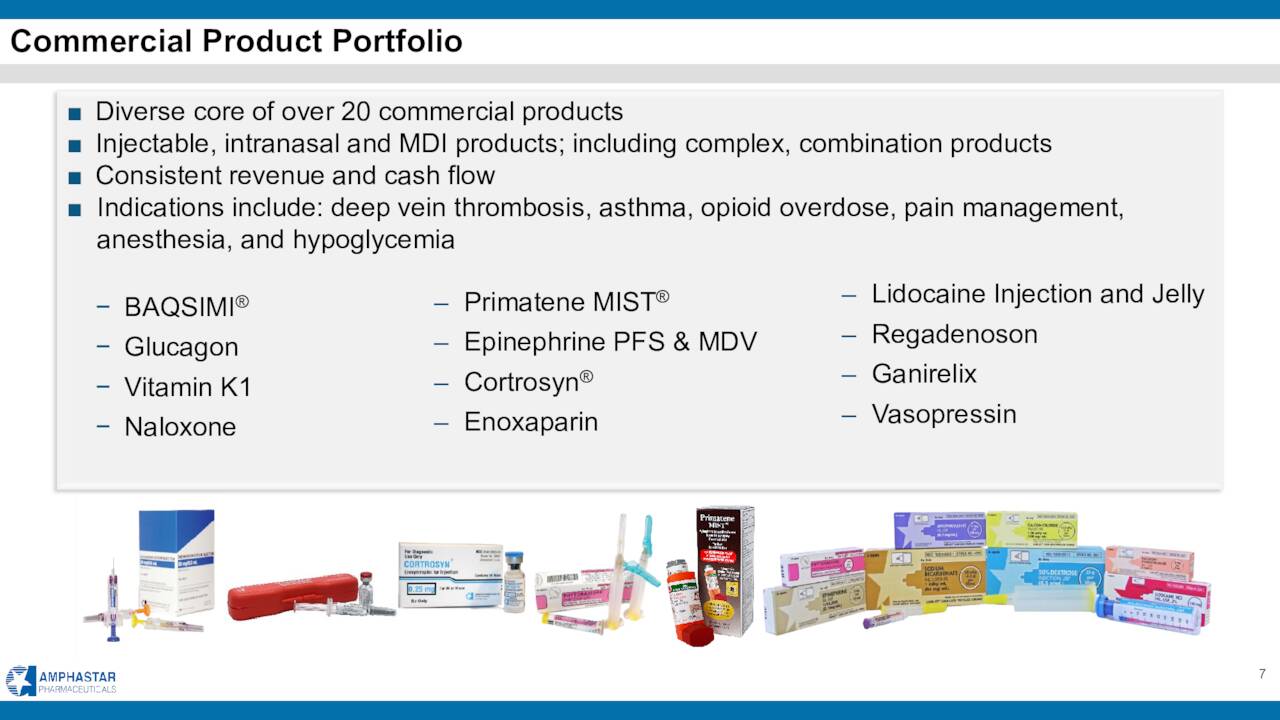

The company has several drugs on the market. Its two current best sellers are Primatene Mist and Glucagon. Primatene Mist is an over-the-counter epinephrine inhalation product for the temporary relief of mild symptoms of intermittent asthma. Glucagon is an important hormone that plays an essential role in regulating blood glucose.

August Company Presentation

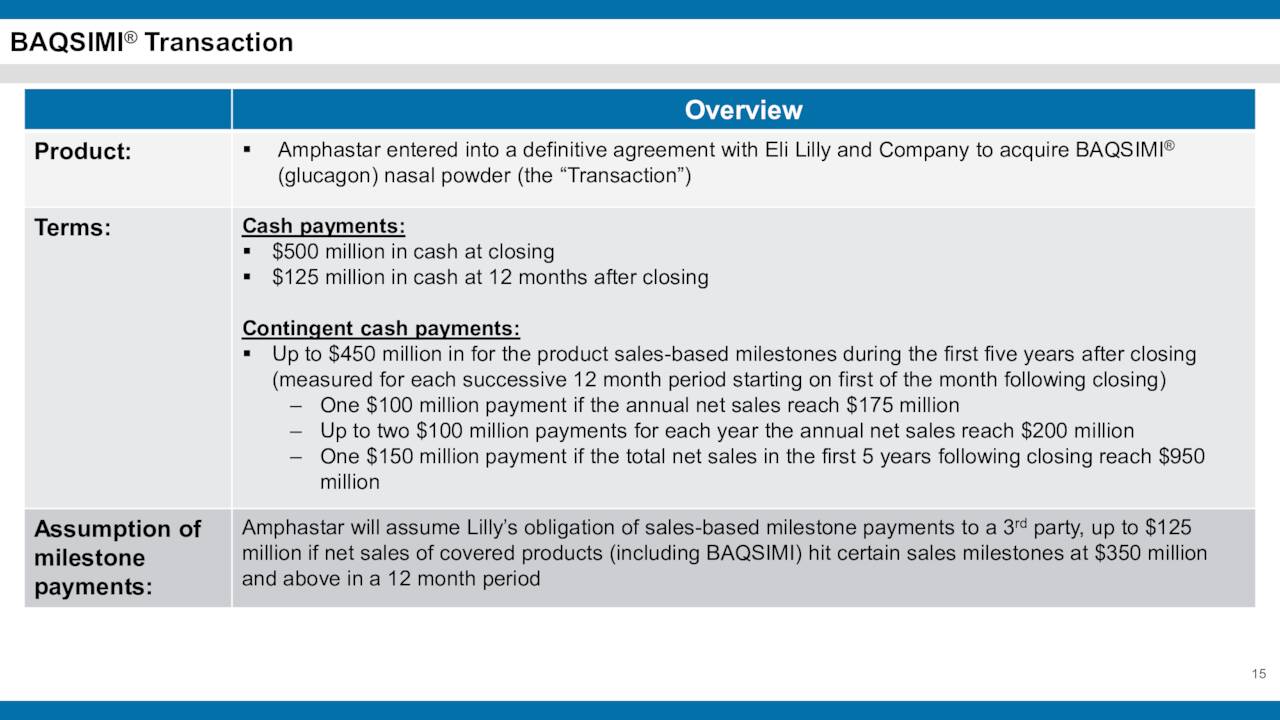

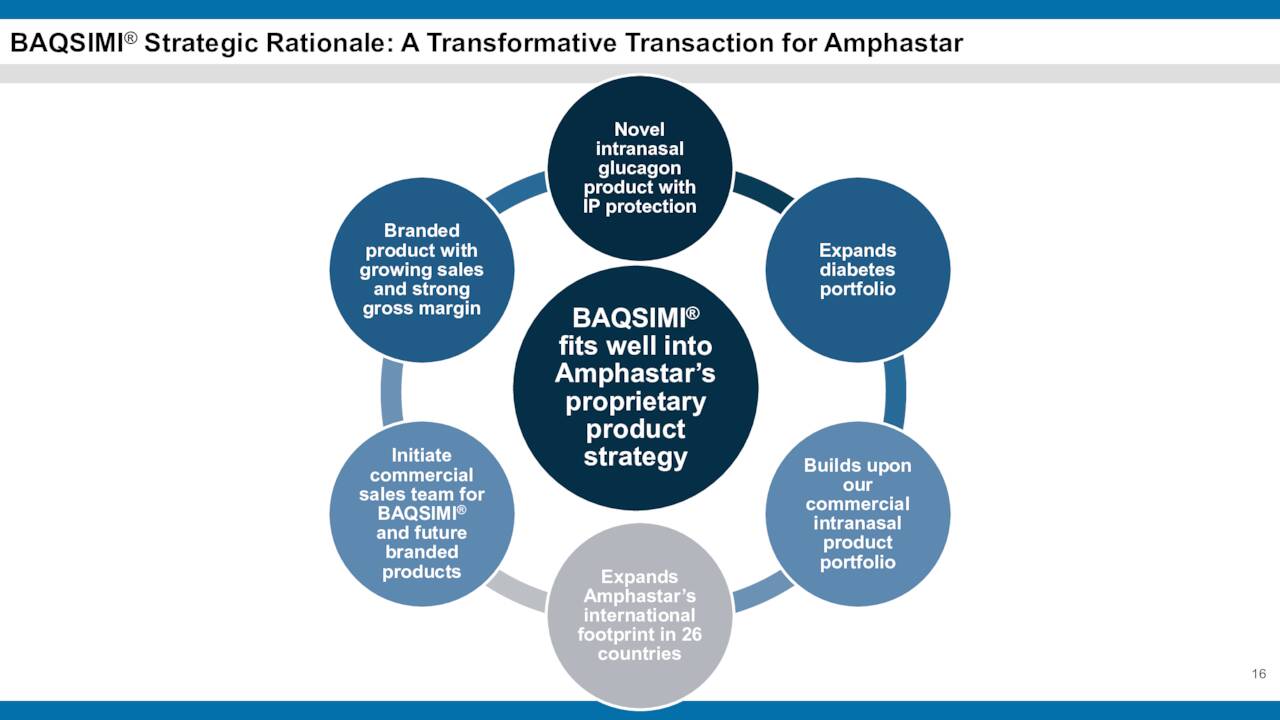

In spring, Amphastar made a major move to bolster its diabetes drug portfolio. The company announced it will acquire diabetes therapy Baqsimi from Eli Lilly (LLY) for $500 million upfront cash and additional potential sales milestones of $450 million. Baqsimi produced nearly $140 million worth of sales globally in 2022.

August Company Presentation

August Company Presentation

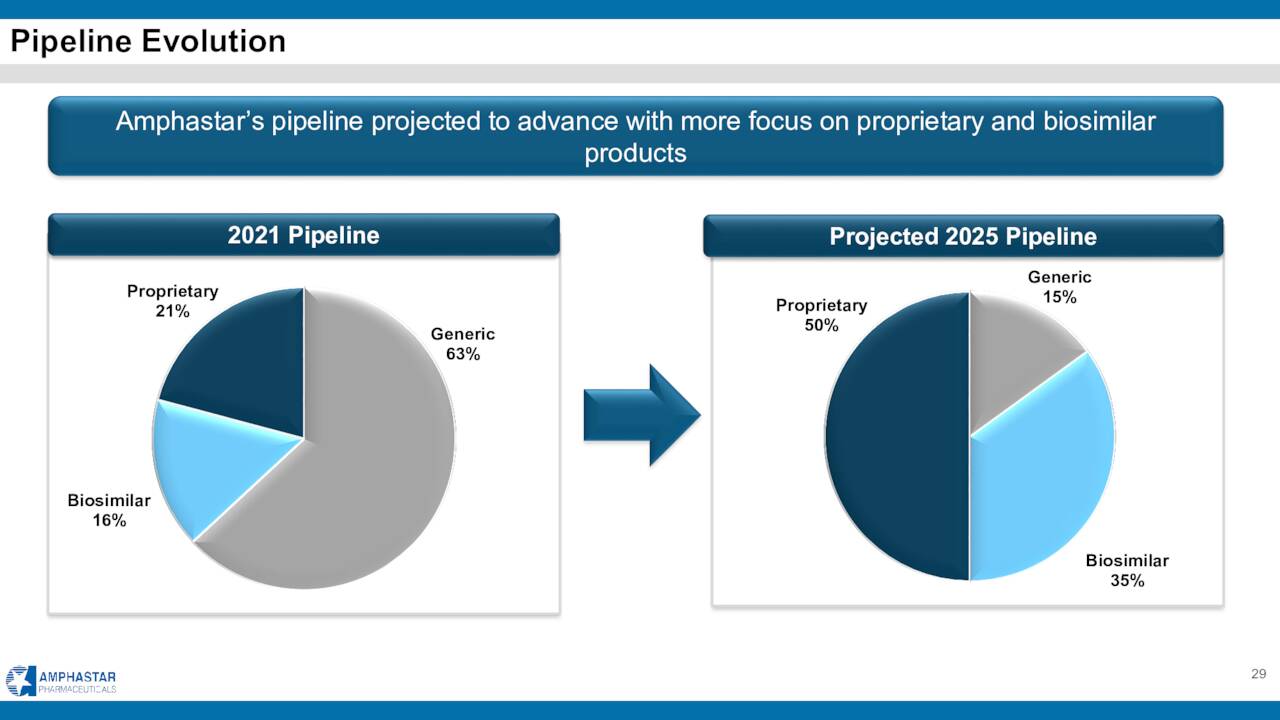

The Baqsimi purchase was a big part of the company’s strategy of moving to a more proprietary product portfolio.

August Company Presentation

Third Quarter Results:

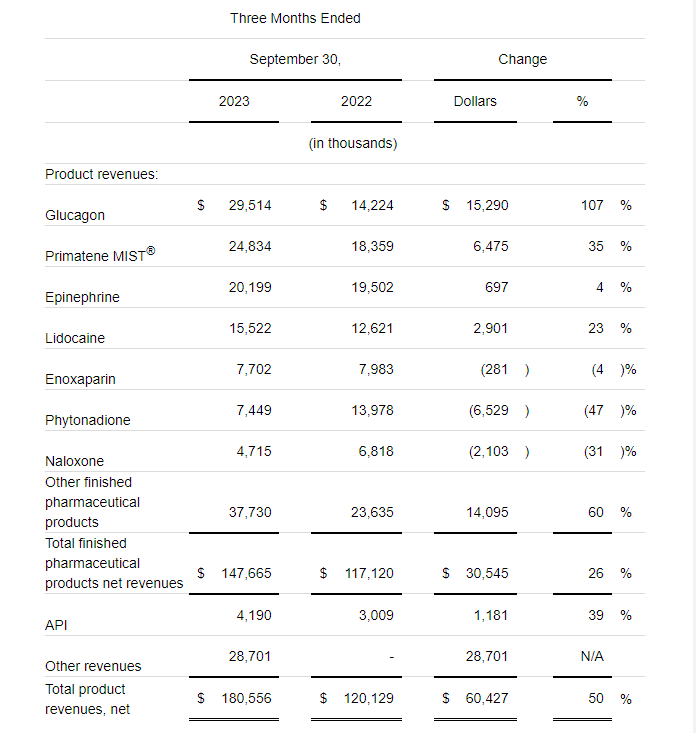

The company posted its Q3 numbers on November 8th. The company had a non-GAAP profit of $1.15 a share, 46 cents a share above the consensus. GAAP net income came in at $49.2 million or 91 cents a share, a 200% increase from the same period a year ago. Revenues rose just over 50% on a year-over-year basis to $180.6 million, some $6 million north of expectations.

Seeking Alpha

As you can see above, Amphastar saw solid growth from several of its key product candidates led by Glucagon and Primatine MIST. Amphastar also booked net economic benefit of $28.7 million from BAQSIMI. This was calculated based on a Eli Lilly sales of $48.7 million less their expenses of $20 million. Amphastar will continue to book revenues on a net basis until the company begins distributing BAQSIMI in 2024.

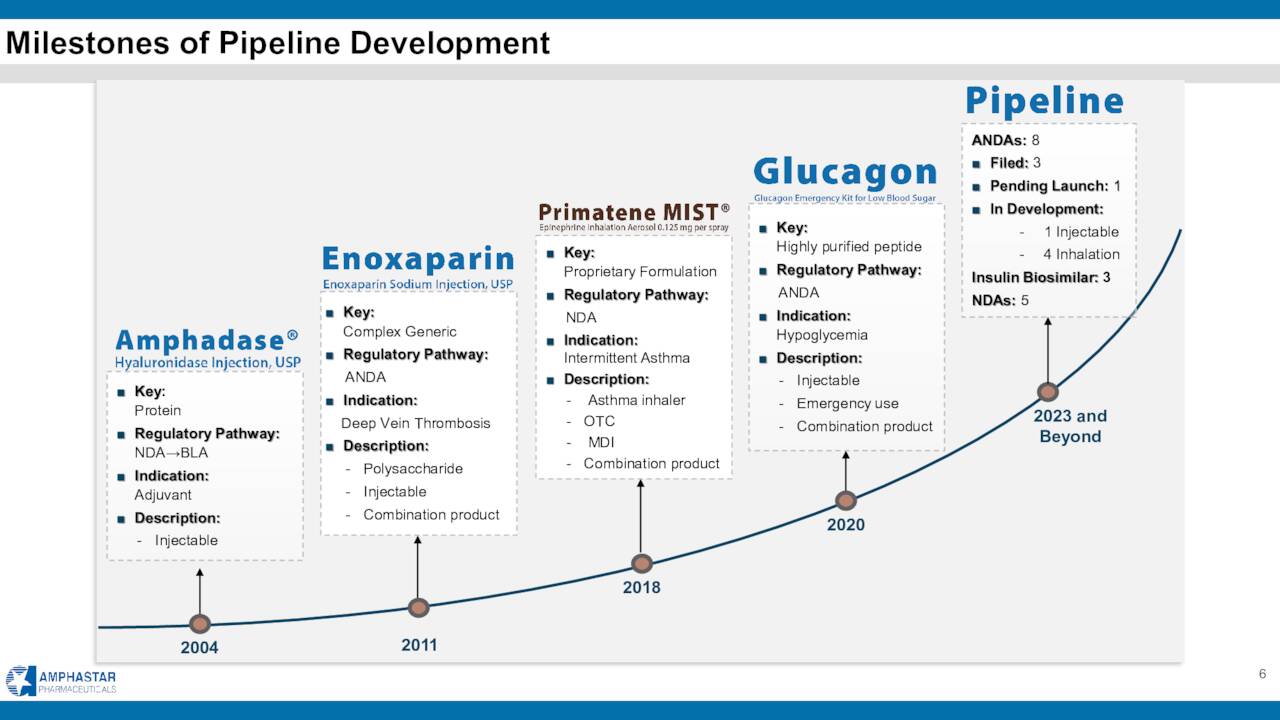

In addition, at the end of the quarter management stated on its third quarter press release that Amphastar had:

Three ANDAs on file with the FDA targeting products with a market size of over $3 billion, three biosimilar products in development targeting products with a market size of over $10 billion, and six generic products in development targeting products with a market size of over $8 billion.”

August Company Presentation

Analyst Commentary & Balance Sheet:

The analyst community is currently mixed on Amphastar’s current prospects. Since third quarter results were posted, DBS ($55 price target) and Piper Sandler ($71 price target) have maintained Buy ratings on the stock. Needham maintained its Hold rating and Bank of America imitated the shares with a Neutral rating and $63 price target. The analyst at BofA stated:

“Amphastar’s valuation is high relative to traditional generic peers and sees Amphastar’s acquisition of the drug Baqsimi as bringing more durable growth and margin expansion to the company.”

He also projects peak sales of Baqsimi of $275 million to $300 million by 2030. It should be noted that management is projecting $250 million to $275 million in peak sales from Baqsimi.

Just under eight percent of the outstanding float in the shares is currently held short. Numerous insiders have been selling shares throughout 2023. However, selling has picked up recently as the stock has moved higher. Since the start of November, a half dozen insiders have sold approximately $4.5 million worth of equity collectively.

The company closed the third quarter with just over $300 million in cash and marketable securities on its balance sheet. Amphastar listed nearly $640 million worth of long-term debt on its third quarter 10-Q. In mid-September, the company offered $300 million in Senior Convertible notes at two percent that mature in 2029. Approximately $200 million of the proceeds were used to pay down existing debt and another $50 million was used to buy back stock. The maneuver helped eliminate all of the company’s variable rate debt, which should reduce interest costs in the coming years.

Verdict:

The company posted $1.97 a share in earnings in FY2022 on $499 million of revenue. The current analyst firm consensus sees a big jump in profit in FY2023 to $3.36 a share as sales jump to $640 million. The expect sales to rise a further 24% in FY2024 as earnings increase to $3.71 a share.

I have to agree with BofA’s analyst in that Amphastar Pharmaceuticals, Inc. shares seem more or less fully valued here at just over 17 times FY2023E earnings. Generic drug maker ANI Pharmaceuticals (ANIP), which should see 50% sales growth in FY2023 followed by five percent sales growth in FY2024, is trading at just under 12 times FY2023E earnings as just one comparison point.

Therefore, I have no investment recommendation on Amphastar Pharmaceuticals, Inc. However, if the shares return to their pre-Q3 earnings release level in the high $40s, I would then probably start to build a position in AMPH at that lower entry point.

Wisdom comes from experience. Experience is often a result of lack of wisdom.”― Terry Pratchett.

Q2 2024 Earnings Call Transcript")