DusanBartolovic/E+ via Getty Images

As investors are approaching a likely turn in the Fed policy trajectory, there is a growing consensus that the time for floating-rate securities is behind us. Many investors believe that once the Fed begins to cut rates, it will fuel a fire under longer-duration, fixed-coupon assets, causing them to outperform. In this article, we discuss some of the misconceptions behind this view and discuss why floating-rate securities remain very appealing assets in the current market.

The Case For Floating-Rate Assets

In our view, there are three factors to think about when considering terming out duration or moving from floating-rate to fixed-rate securities.

First is that the Fed could easily take their time to push rates lower. This is because financial conditions have eased quite a bit already since the Fed has signaled the peak in the policy rate. As the market priced in expectations of lower cost of capital, markets have rallied with credit spreads tightening, equity prices rising and longer-term rates and volatility falling.

This has, in effect, reversed some of the Fed’s hikes. Moreover, recent data has pushed back on the view that the Fed was going to imminently take the policy rate lower. Payrolls blew everyone out of the water, coming in above every single forecast, with previous months’ readings revised higher. This was followed up by a spike in average hourly earnings which rose 0.6% or double the expected gain. Finally, the ISM prices paid component jumped by the largest amount in over a decade.

This strong run of data clearly runs counter to what the Fed is trying to achieve, which means that the likelihood that the policy rate will remain stable for longer has gone up substantially. The market has already shaved off 1-2 hikes this year from earlier estimates, and this trend could continue.

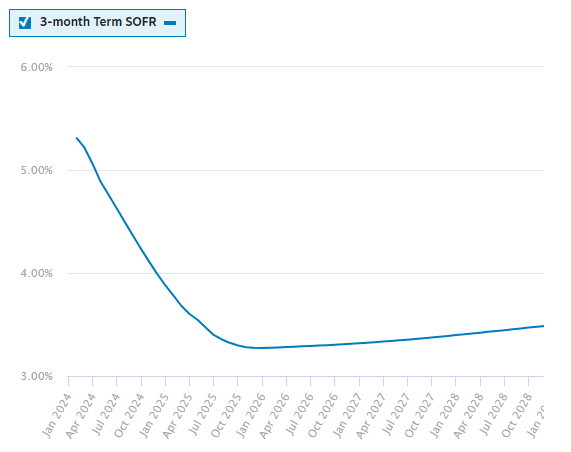

Two, whenever things are “obvious” (i.e., that Fed policy rate cuts will drive a rally in longer-term rates) we need to consider what is already priced by the market. In other words, there is rarely a free lunch. Here we see that markets are already pricing in substantial cuts over the next couple of years. For instance, while SOFR is now around 5.3%, by Sep-2025 it’s expected to be 3.3%.

Systematic Income Preferreds Tool

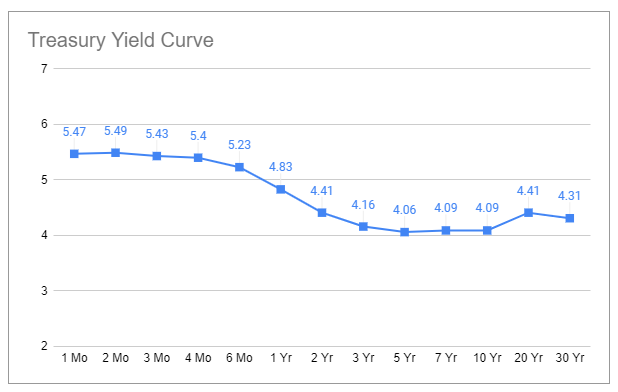

This significant drop is priced into long-term rates. For instance, the typical corporate bond has a Treasury base rate (before its relevant credit spread) of 4.2-4.1% despite the policy rate being north of 5%.

Systematic Income Preferreds Tool

Many investors think that when the Fed begins to cut rates, it will cause “rates” to move lower, buoying the prices of fixed-coupon securities. This is a basic misunderstanding of how markets work, as well as a conflation of short-term and long-term rates. The latter point is a pet peeve of ours, and we often half-joke that analysts should be banned from speaking about “interest rates” since short-term and long-term rates can behave very differently from each other.

Short-term rates are anchored directly off Fed’s actions while longer-term rates are more-or-less free to move about based on various factors such as expectations of what the Fed will do in the future, supply / demand, inflation risk premium etc.

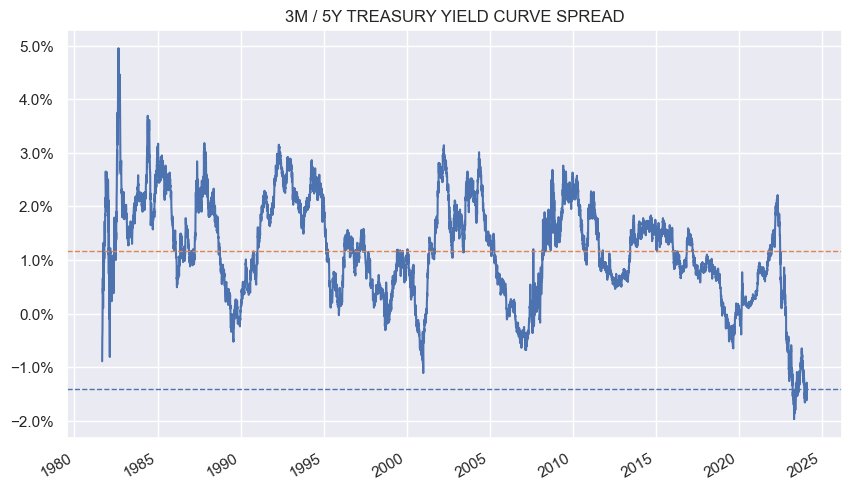

The key point is that longer-term rates already anticipate or price in the expected drop in short-term rates (in addition to several other secondary factors). This is precisely why the yield curve is so unusually inverted (i.e. why long-term rates are below short-term rates). For example, historically the 3-month / 5-year yield curve spread is roughly 1.1% (i.e., 5-year Treasury yields are on average 1.1% above 3-month Treasury yields). However, right now 5-year Treasury yields are 1.4% below 3-month yields – a gap of around 2.5% from the historic norm.

Systematic Income Preferreds Tool

Moreover, even if we accept that over the next two years, short-term rates will fall to 3.3%, in line with market expectations, that rate will be 0.8% below today’s 5Y Treasury yield (US5Y), rather than the average 1.1%.

In our view, longer-term rates could fall further not if the Fed simply cuts rates, but if the market thinks that more rate cuts are likely forthcoming than what is current priced in (about 8 are priced in right now). This could happen if we see more than the expected amount of disinflation or, alternatively, if the economy hits a speed bump and careens into a recession, pushing the Fed to bail it out with speedier rate cuts.

Three, the risk to longer-term rates is fairly well-balanced. Floating-rate securities were less appealing when the yield curve nearly flattened late last year, even as inflation was clearly moving over the hump and the Fed was looking through to rate cuts over the following year. Now, with longer-term rates well below short-term rates, there is appreciable risk to a back-up in longer-term rates. This could be either due to the Fed taking its time with rate cuts or due to the economy or inflation heating back up. Floating-rate securities would hold their value much better in this not-at-all unlikely scenario.

Some Ideas

We hold a number of floating-rate securities and funds across our Income Portfolios.

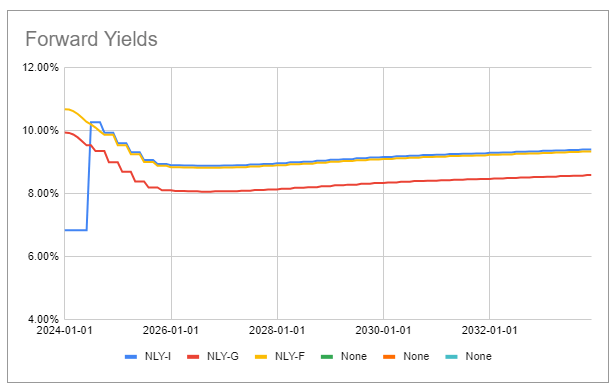

We continue to like the Agency mortgage REIT Annaly Series F preferred (NLY.PR.F), trading at a stripped yield of around 10.6%. Despite all the tumult in the mortgage REIT space over the last couple of years, its equity / preferred coverage ratio is only a bit below its Dec-2019 level. The company has been able to mitigate a large drop in book value (that we have seen across the broader Agency mortgage REIT space) by equity issuance and preferred redemptions.

Systematic Income Preferreds Tool

Another security worth a look is the 2028 subordinated bond from Zions Bank (ZIONL), now accruing at the equivalent of 3-month Libor + 3.89% or about 9.19%. This is plainly too high for the credit risk of the bank as well as relative to its preferreds. ZIONL is trading only a touch over par in stripped price terms so any hit on redemption would be small and would be covered by the remaining accrued in most cases.

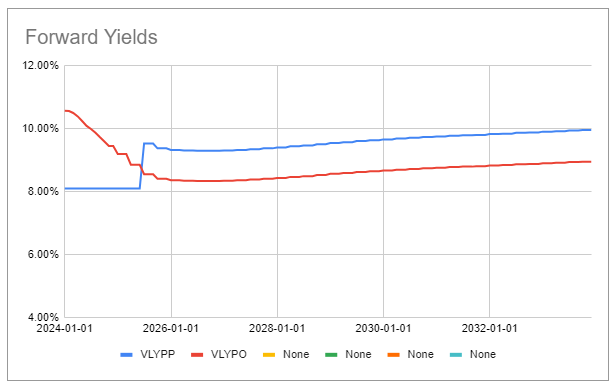

Investors with a higher level of risk appetite should have a look at the Valley National Bancorp Series B (VLYPO), trading at a 11.1% yield. The company’s earnings disappointed, causing a drop in the price of the preferreds and common. Given the recent NYCB debacle and last year’s memories of bank failures, markets shoot first and ask questions later, at least for bank securities. The bank’s loan book is about half in CRE with significant exposure in NY/NJ and Florida, though much of that is in multi-family which is less of a concern. The office loan book is well diversified with a 53% LTV – fairly conservative. Loan provisions did increase but modestly to $21m and non-accrual loans are below 0.6%. The forward yields of the bank’s two preferreds are shown below and offer decent risk/reward in our view.

Systematic Income Preferreds Tool

Outside of preferreds, we like the Janus Henderson B-BBB CLO ETF (JBBB) with a 9.25% yielding portfolio, which works out to around 8.75% after fees. This is not bad for a 99.4% investment-grade holding portfolio, no leverage and no first loss on defaults within the collateralized loan obligation, or CLO, tranches. Recall that CLOs tend to have higher-quality portfolios than the broader bank loan market because of the rules that limit the amount of loans rated CCC.

In the BDC space, we like the Golub Capital BDC (GBDC). The company has a 12.7% net income yield on price. Its dividend policy is convoluted with a $0.39 base dividend, supplemental dividend based on half of the excess net income and another $0.05 likely to come over the next three quarters if its current merger with another private Golub BDC is approved. The company has delivered a strong 13.3% total NAV return over the past year and has recently reduced various fees, which have sustainably boosted its net income. Its portfolio quality remains robust.

A security to keep an eye on is the Allstate 2053 bond (ALL.PR.B). It is currently redeemable and trading a few percent over par with a yield of around 8.2%. A stripped price closer to $25 would result in no hit in case it is redeemed.

Takeaways

Our base case remains that the Fed will start cutting around the middle of this year. However, this doesn’t mean that floating-rate securities are unattractive. In fact, the Fed is unlikely to be in a rush to move the policy rate lower and even if it does, it will take time. And even at the end of its expected cycle of cuts, floating-rate assets will remain attractive by historical norms versus their longer-term counterparts. Separately, the coming Fed rate cuts are unlikely to boost fixed-rate securities, as the rate cuts are already priced in. If anything, fixed-rate securities are now more vulnerable to a rate back-up if inflation or the Fed prove too stubborn for the market’s base case. Ultimately, both floating-rate and fixed-rate securities have a place in a diversified income portfolio, so it’s too early to bid goodbye to the former.

Q2 2024 Earnings Call Transcript")