If you’re on the lookout for a high-yield stock, you’ll probably find the 17.7% dividend yield at AGNC Investment (AGNC 1.50%) highly attractive. But be careful: Historically, that yield has burned more than one investor. Here are three important things to know before you decide to buy AGNC Investment today.

1. AGNC is not a traditional REIT

Technically speaking, AGNC Investment is structured as a real estate investment trust (REIT). Traditional REITs are fairly simple businesses to understand, given that they own physical properties, rent them out, and pay dividends from the cash flows they generate along the way. While REITs can get themselves into trouble if they use leverage too aggressively or they own properties that are out of favor, such as offices are today, the REIT sector is a fairly predictable one where investors can find reliable and attractive dividend yields.

Image source: Getty Images.

AGNC, however, is not a traditional REIT. It’s a mortgage REIT, which is a far more complex animal. To simplify, AGNC owns mortgages that have been bundled into bond-like investments, often called something like a collateralized mortgage obligation (CMO). So it basically owns a bunch of loans. And the business model is built on using leverage, often backed by the CMOs in the portfolio. The goal is to earn more in interest from the CMOs than the interest costs being paid. In some ways, mortgage REITs are more like a mutual fund than a traditional landlord.

Only investors with the time and will to dig into the mortgage REIT business should be treading into the sector. And even then, you should tread with caution.

2. AGNC has a history of dividend cuts

There are a lot of things that can go wrong in the mortgage space that will upend a mortgage REIT’s dividend-paying ability. Changes in interest rates, repayment rates, the housing market, and investor sentiment can all play a role. That’s not to suggest that such issues aren’t a factor for traditional REITs, but they just seem to have a much bigger impact on mortgage REITs.

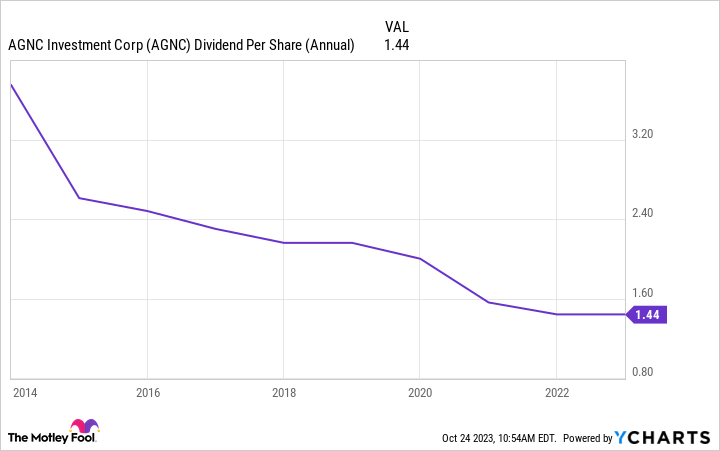

AGNC Dividend Per Share (Annual) data by YCharts

To put a number on that, as the preceding chart shows, AGNC’s dividend has been in steady decline over the past decade. That’s at a time when most traditional REITs had been performing fairly well, with a large number of regular dividend increases from some of the best-known REITs, such as Realty Income (O 0.68%), Federal Realty (FRT 0.76%), and AvalonBay (AVB -2.43%).

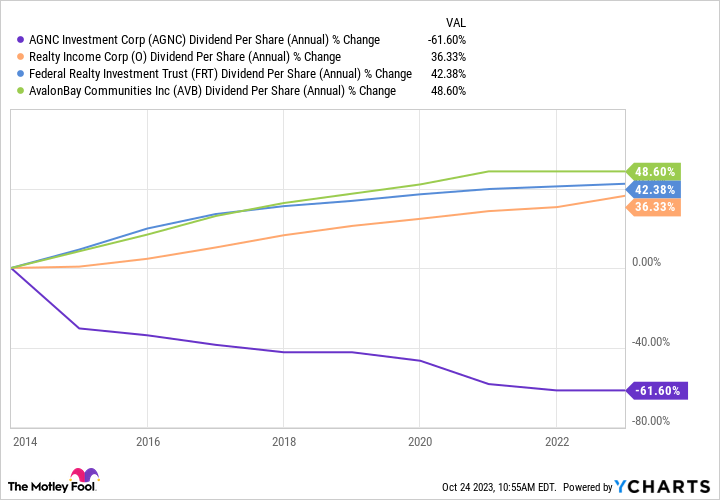

AGNC Dividend Per Share (Annual) data by YCharts

Sure, AGNC’s dividend could turn higher at some point. But is the risk that it doesn’t worth it? That’s especially true if you’re trying to create a reliable passive income stream to help support you in retirement.

3. AGNC’s dividend yield is high, but that’s not a good thing

The really pernicious thing here, however, is that AGNC’s dividend yield has usually been above 10% over the entire 10-year period in which the dividend was heading regularly lower. Dividend yield is a simple math equation that divides the annual dividend by the share price. So the reason the yield has remained so high even as the dividend has been cut is that the share price has declined, too.

Step back and think about that for a second. If you bought AGNC because of its high yield, you would have suffered a string of dividend cuts and a declining share price. So you’d have less income and capital losses, which is pretty much the worst possible outcome a dividend investor could possibly achieve. Given that history, most investors should probably avoid AGNC.

Only for the right kind of investor

AGNC Investment isn’t really appropriate for most investors, but it isn’t really created for most investors. Institutional buyers such as insurance companies and pension funds, focused on total return and diversification, might actually find the stock of value within a much larger portfolio. But dividend investors trying to create a passive income stream have, for many years, only been hurt by chasing this high-yield stock. If you’re buying it today, you might want to step back and reconsider the risks.

Reuben Gregg Brewer has positions in Federal Realty Investment Trust and Realty Income. The Motley Fool has positions in and recommends Realty Income. The Motley Fool recommends AvalonBay Communities. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")