Utilities can generate lots of dividend income.

Utilities operate very boring businesses. They distribute electricity and natural gas to customers under government-regulated rate structures. There isn’t a lot of upside in this business (demand and rates are relatively steady), but there is also not much downside. Because of that, utilities generate pretty stable returns, a large portion of which comes from their high-yielding dividend payments.

Investors seeking to add more stability to their portfolio should consider buying a boring utility stock. Black Hills (BKH 0.15%), Consolidated Edison (ED 0.60%), and Duke Energy (DUK 0.37%) stand out to a few Fool.com contributors as great options for those seeking a high-yielding and sustainable dividend.

Black Hills is the mouse that roared

Reuben Gregg Brewer (Black Hills): When it comes to utility stocks, Black Hills, with a $3.9 billion market cap, is one that often slips under the radar screen. That’s a shame because the regulated natural gas and electric utility is a Dividend King with 54 consecutive years of annual dividend increases behind it. The average dividend increase over the past three-, five-, and 10-year periods are all around 5%, showing incredible consistency. Meanwhile, the yield is currently around 4.5%, which is toward the high end of the yield range over the past decade.

BKH Dividend Yield data by YCharts

In other words, Black Hills looks like it is a Dividend King that’s been put on the sale rack. There’s a good reason for that, however, because operating a utility is a capital-intensive business. The sharp rise in interest rates will increase Black Hills’ costs going forward. There’s no way around that, noting also that the utility tends to use more leverage than some of its larger peers.

That said, Black Hills’ customer growth has increased at nearly three times the rate of U.S. population growth. It operates in very attractive markets in Arkansas, Colorado, Iowa, Kansas, Montana, Nebraska, South Dakota, and Wyoming. And that suggests that regulators will, in time, adjust the company’s rate structure to account for the change in interest rates. If you have the patience to wait for that to happen, you can collect a historically high dividend yield from a fairly boring Dividend King utility.

The king of consistency

Matt DiLallo (Consolidated Edison): Consolidated Edison provides electricity and natural gas to customers in the New York City metro area. While utilities are boring businesses, they generate very predictable cash flow backed by steady demand and government-regulated rate structures. That provides Consolidated Edison with stable income to pay dividends and invest in maintaining and expanding its utility infrastructure.

The utility hit a major dividend milestone earlier this year. It delivered its 50th consecutive annual dividend increase. That’s the longest period of consecutive dividend increases among utilities listed in the S&P 500. It also ushered the company into the elite group of Dividend Kings. Consolidated Edison’s increased payout currently yields a little less than 3.5%, which is more than double the S&P 500’s dividend yield (around 1.3% based on dividend payments over the past year).

While the company expects to continue increasing its dividend, growth will likely be moderate. Consolidated Edison plans to target a dividend payout ratio of 55%-65% of its adjusted earnings to fund higher levels of investment amid the clean energy transition. That’s down from its prior target of 60% to 70%. It plans to retain more of its earnings to internally fund growth. This strategy should enable Consolidated Edison to grow its earnings per share faster in the future. That positions it to potentially produce higher total returns when adding its dividend income to the stock price appreciation it should deliver as its earnings grow.

Consolidated Edison’s dividend should become more sustainable over the longer term as it lowers its payout ratio and invests in supporting the clean energy transition. These features make it an attractive option for those seeking a very bankable income stream.

This utility’s narrowing focus should pay big dividends

Neha Chamaria (Duke Energy): Duke Energy is one of the largest regulated utilities in the U.S. and operates in growing places like Florida and the Carolinas, among others. In fact, the company sold its unregulated commercial renewable energy business in 2023 for $2.8 billion and became a fully regulated utility. The company said it’ll use the net proceeds of roughly $1.1 billion from the sale to pare down debt and strengthen its balance sheet.

2023 was also a strong year for Duke Energy as it added the largest number of customers in its history and boosted its five-year capital investment plan to $73 billion to drive its transition to clean energy. The utility giant is targeting net-zero carbon emissions from power generation by 2050 and has, therefore, planned massive investments to upgrade its electricity grid and expand its energy storage, renewables, natural gas, and nuclear energy assets in the coming years.

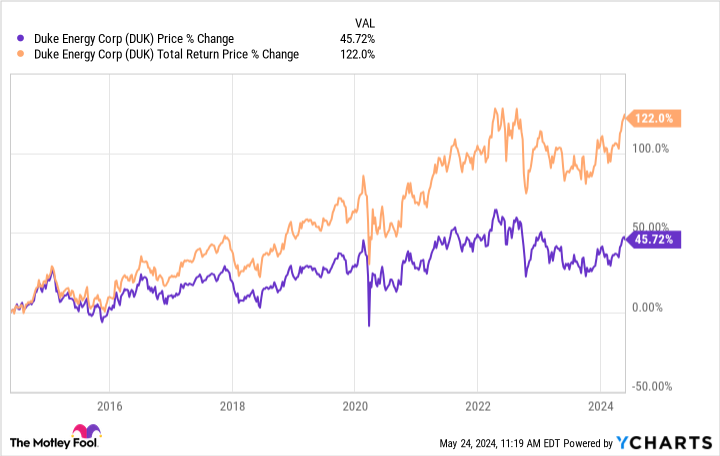

Backed by a fully regulated portfolio of assets in growing jurisdictions, Duke Energy expects to grow its adjusted earnings per share by 5% to 7% through 2028. When coupled with a dividend yield of 4%, management believes investors in Duke Energy could earn nearly 10% annualized returns. Duke Energy is also a bankable dividend stock. It has paid a dividend every quarter for 98 years and has grown its dividend over time. That dividend growth has hugely boosted shareholder returns so far. In the past 10 years, Duke Energy stock has more than doubled investors’ money when factoring in dividends.

With Duke Energy now fully pivoting to regulated businesses and fortifying its balance sheet, income investors have solid reason to consider this boring utility stock

Q2 2024 Earnings Call Transcript")