Dividend stocks can be a popular subset of the stock market for many investors, especially those in or near retirement. After all, an income stream that results from doing nothing more than owning a great company does sound attractive. That said, not all dividend-paying companies are equal, and it makes the most sense to identify strong businesses that also pay dividends.

For those with limited funds, here are three companies with strong track records and bright futures that pay a healthy dividend and can be purchased for less than $50.

1. Bank of America

Bank of America (BAC -1.55%) is one of the largest banks in the U.S., which gives it some advantages. For one, its large, diversified customer base insulates it a bit from the kind of bank run we saw last March that led to the downfall of a few smaller regional banks.

Bank of America also pays a nice dividend, currently yielding 2.8%. This easily outpaces the S&P 500‘s average dividend yield of 1.5%.

One of the highlights of Bank of America’s most recently reported quarter was its net interest income (NII). This metric grew to $14.5 billion year over year, good for an increase of 4%. This is due to higher interest rates and the bank’s increased interest income on its investments.

Equally important is that the bank had a slight increase in net interest margin as well. This is the difference between what it makes on interest and what it pays to its customers in interest. Because such a large part of its business is low-interest consumer banking accounts, Bank of America can raise the interest it pays to customers more slowly than the interest it earns on its loans and investments.

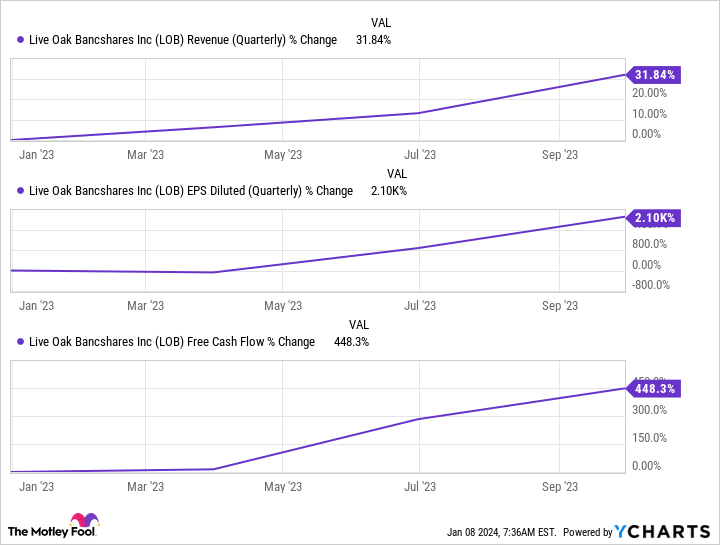

2. Live Oak Bancshares

Moving to a smaller bank, Live Oak Bancshares (LOB -1.96%) has a unique business model that helps it stand out among a sea of regional banks. Live Oak specializes in small business lending but in a very specific and purposeful way. By lending only in industries it knows well, it can make smart loan decisions and limit potential loan defaults.

Live Oak is also a digital bank, with no physical locations and a robust online presence. This eliminates the expense of having to own and operate branches.

Live Oak had a strong 2023, with its stock increasing by 51% during the year. This is especially impressive, considering at one point, it was down more than 30% after the March 2023 mini-banking crisis. The year-long growth in the share price makes sense, considering nearly all of Live Oak’s financial results improved over the year.

Here’s the increase in revenue, earnings per share, and free cash flow through the first nine months of 2023.

LOB Revenue (Quarterly) data by YCharts

Total loans and leases, total assets, and total deposits also grew steadily through the first nine months of the year. Net interest margin, the gap between interest earned and interest paid, is also significantly higher than Live Oak’s large bank peers. As of Q3 2023, Live Oak’s net interest margin was 3.4%, compared to a 2.7% average for several large banks like Bank of America.

3. EPR Properties

With a dividend yield of 6.9%, EPR Properties (EPR -0.58%) is a compelling investment to consider due to its dividend alone. Fortunately, the company offers even more to its shareholders.

EPR is a real estate investment trust (REIT), which means it is obligated to pay out at least 90% of its taxable income to shareholders as a dividend. The REIT specializes in entertainment real estate and owns things like movie theaters, golf courses, and ski resorts.

EPR had a strong 2023, with its stock up 28% after falling by 21% in 2022. The 2022 drop was due in part to EPR’s exposure to movie theaters, which account for about 40% of its real estate portfolio. Specifically, EPR had to deal with a bankruptcy proceeding for the parent company of Regal Cinemas, a major tenant, which understandably held the stock back for some time.

Fortunately, that is now in the rearview mirror, and EPR is making general efforts to diversify away from movie theaters to spread its risk profile out among a more diverse set of entertainment properties. The percentage of theaters dropped from 41% of the portfolio in Q3 2022 to 39% in Q3 2023, and the company’s goal is to reduce that percentage even further over time.

EPR’s revenue rose by 17% in Q3 2023, and its adjusted funds from operations (which can be thought of as a substitute for earnings per share when evaluating a REIT) increased by 28%. These results also accelerated compared to the Q2 year-over-year results. It seems like EPR is back on track, and with its impressive dividend yield, now may be a great time to buy shares.

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Jeff Santoro has positions in EPR Properties and Live Oak Bancshares. The Motley Fool has positions in and recommends Bank of America and Live Oak Bancshares. The Motley Fool recommends EPR Properties. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")