Investors are warming up to Ulta Beauty (ULTA -0.94%) stock again. Shares of the spa and beauty products retailer jumped in late November after management announced surprisingly strong third-quarter results. Wall Street was even more excited about the chain’s improving short-term outlook as spending trends strengthened.

Let’s look at why the latest operating update makes Ulta Beauty stock look even more attractive right now.

1. Beating expectations

The big concern heading into this report was that Ulta Beauty would struggle to grow after posting huge sales gains a year ago. Yet comparable-store sales rose 5% in the quarter that ran through late October, on top of a 15% spike in the year-ago period. Management admitted it was surprised by that achievement. “Sales, gross profit, and [earnings per share] all exceeded our internal expectations,” CEO Dave Kimbell said in a Nov. 30 press release.

Yet there were some growth challenges evident in this report, too. Ulta continued to see declining spending levels that were offset by higher traffic. Price cuts are necessary, in other words, to keep the retailer’s aisles busy. Still, that approach seems to be keeping Ulta in its leadership position even as rivals try to steal its market share.

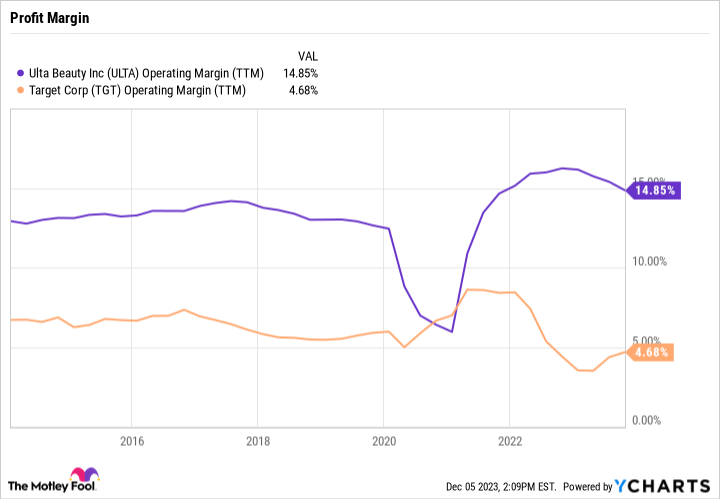

2. Stable profitability

The stock had sold off for much of 2023 on fears that Ulta’s profit margin would fall hard after setting a record in 2022. Target is merely aiming to return to its pre-pandemic profitability, after all, essentially erasing the gains that shareholders saw during those high-growth years in 2020 and 2021.

ULTA Operating Margin (TTM) data by YCharts

That’s not happening with Ulta Beauty, though. Gross profit margin inched down only slightly this past quarter, declining from 41% of sales to 40%. Operating income landed at $1.15 billion, or 15.2% of sales compared to 17% of sales a year earlier. Ulta is still on track to hold that 15% profitability level, which is more than double the 6% that Target is working to reach. It’s a great sign for the business that Ulta can preserve most of its pandemic-fueled margin boost even in a slower-growth selling environment.

3. The solid outlook

In late November, Ulta executives raised the low end of their 2023 guidance on both the top and bottom lines. But sales are still on track to land at about $11.1 billion this year compared to $10.2 billion last year. The earnings forecast received a similarly modest upgrade. Together, these revisions mainly ease investors’ fears that demand trends are worsening more than they create euphoria about soaring growth on the way.

Still, Ulta Beauty is a far stronger, more profitable business than it was before the pandemic struck. And its shares remain attractively valued after their weak performance in 2023. You can buy the stock for 2.2 times annual sales right now, down from nearly 3 times sales earlier in the year.

Patient investors might be able to get an even better deal if stocks proceed lower in the coming months. But that’s no reason to avoid Ulta Beauty shares right now. With solid growth, excellent profitability, and an improving outlook, this retailer seems well-positioned to deliver good shareholder returns in 2024 and beyond.

Q2 2024 Earnings Call Transcript")