It’s not uncommon for investors to focus on the per-share price of a stock. It’s easy to confuse a low-priced stock with a cheap one, but that’s not always the case. There are plenty of stocks with low per-share prices that are expensive, and many with triple- or even quadruple-digit per-share prices that are cheap.

However, some stocks are cheap and have a low per-share price. The trick is to recognize which stocks are cheap because the business is broken, and which are cheap simply because the market is being impatient. Here are two great stocks that fit into the latter category, and each can be purchased for less than $70.

1. Twilio

Few stocks epitomize the wild volatility of the past few years more than Twilio (TWLO 2.66%). Over the past five years, this communications software company has seen its stock soar as high as $443 and fall as low as $43. Year to date, shares are up 38%; they trade for $68 at the time of this writing.

Some of this volatility was due to the overall market’s exuberance during 2020 and 2021, followed by the long bear market during 2022. However, some business fundamentals for Twilio drove these results as well.

Historically, Twilio prioritized growth over profitability. This was fine when interest rates were at or near zero and the market was rewarding growth. But times have changed, and unprofitable, high-growth stocks are being scrutinized more by the market.

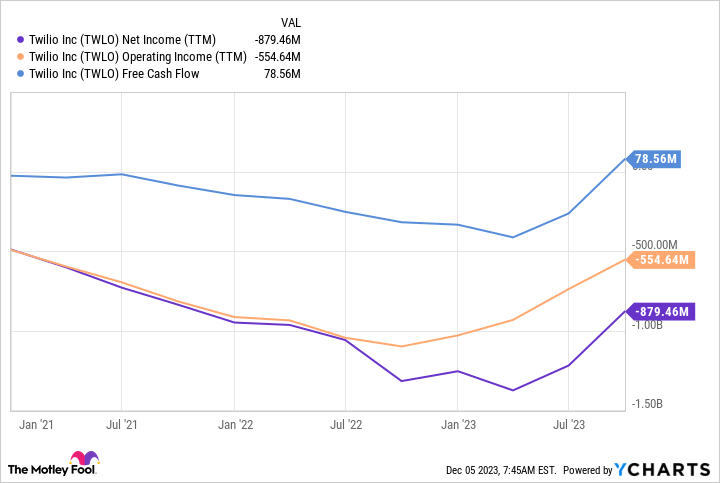

Fortunately for Twilio, it shifted its business to adjust, and the trends have been positive. For example, notice the turnaround in operating income, net income, and free cash flow over the past year. This is made more impressive by the fact that revenue growth slowed at the same time.

TWLO Net Income (TTM) data by YCharts

To be clear, Twilio still has some work to do to get to profitability, but a path to getting there is becoming clearer. With shares trading for just 3 times sales, the valuation looks compelling enough to buy some shares and watch the march toward profitability continue to play out.

2. PayPal

Fintech company PayPal (PYPL 0.79%) has had an almost identical last five years to Twilio. The stock peaked in mid-2021 at $308 and bottomed recently at $50.

Year to date, shares are down 19%. After some particularly strong quarters of performance during the pandemic, PayPal’s trajectory headed in the wrong direction, as did its stock price.

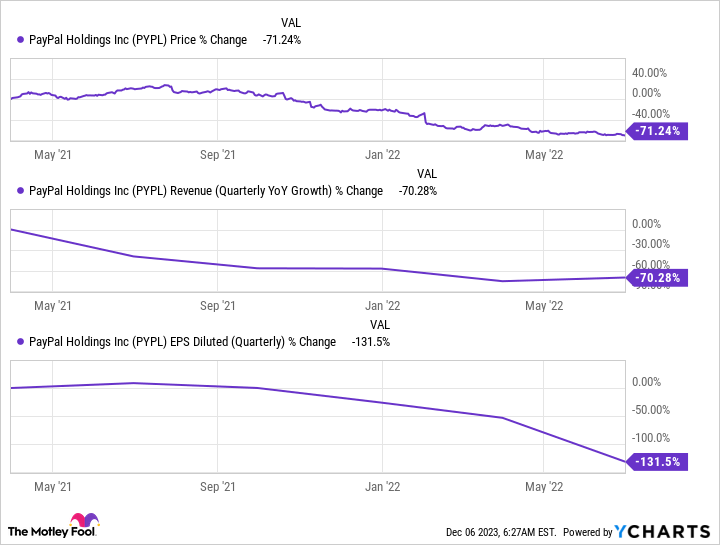

Here is the percentage change in the stock price, quarterly revenue growth, and quarterly earnings per share from the first quarter of 2021 through the second quarter of 2022.

While revenue growth remained stuck in the single digits, PayPal has gotten its profitability straightened out. After bottoming out at a net loss of $0.29 per share in Q2 of 2022, PayPal recovered nicely, and in the recently reported Q3 of 2023, earnings per share were $0.93.

Considering the reach of PayPal’s products, it’s not difficult to see how the company could reaccelerate its revenue growth and get the stock price rising again. According to new CEO Alex Chriss, more than 70% of the adult population in the United States has used PayPal in the last five years. That’s an incredible statistic and should be a strong base to build upon as Chriss looks to direct the company in a new direction.

That new direction includes reducing expenses and refocusing the business in several key ways. The top two priorities of the new management team are to better the PayPal checkout feature and better PayPal’s approach to small and medium-sized businesses.

PayPal’s large customer base and new leadership give me hope for the future of the company. Its rock-bottom valuation also provides a decent margin of safety. PayPal trades for 2.2 times sales and 17 times earnings, both near all-time lows for the company. Any meaningful acceleration of the business could make today’s valuation look appreciate a bargain.

Jeff Santoro has positions in PayPal and Twilio. The Motley Fool has positions in and recommends PayPal and Twilio. The Motley Fool recommends the following options: short December 2023 $67.50 puts on PayPal. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")