Dividend Kings are unquestionably among the top picks for income-seeking investors. These are companies that have increased their payouts for at least 50 consecutive years, which strongly suggests they have resilient businesses and can generate consistent profits and cash flow.

Many Dividend Kings are worth investing in, but let’s discuss just two today: Abbott Laboratories (ABT -2.08%) and Johnson & Johnson (JNJ -1.10%). These leaders in healthcare have been rewarding shareholders for decades and should continue to do so for a long time. Here is why.

1. Abbott Laboratories

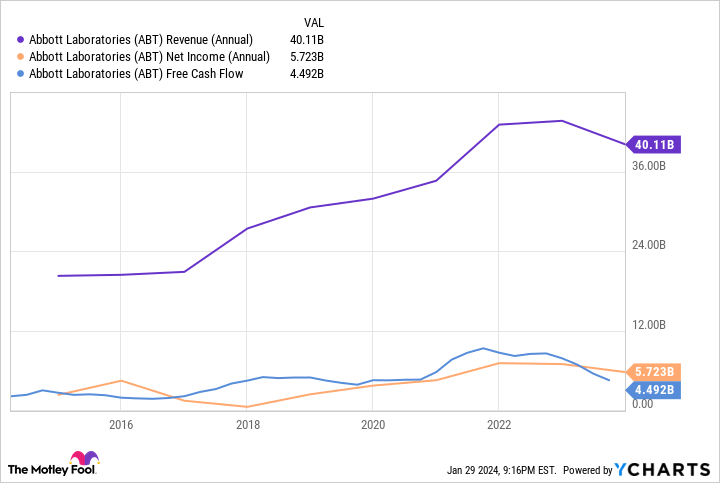

At first glance, Abbott Laboratories doesn’t seem to be doing well right now. In 2023, the company’s sales declined by 8.1% to about $40.1 billion. Adjusted net earnings per share (EPS) came in at $4.44, down from the $5.34 reported in the previous fiscal year.

However, this relatively poor performance can be attributed to the company’s coronavirus diagnostics segment. Sales of COVID tests declined substantially last year. Excluding this segment, Abbott’s revenue increased by 11.6% year over year organically.

More importantly, the company still has multiple growth avenues, so last year’s performance doesn’t indicate what the future holds. Consider the company’s work in diabetes care, most notably with its continuous glucose monitoring (CGM) franchise, the FreeStyle Libre.

Once again, it was the star of the show for Abbott last year. Libre sales in 2023 increased by 24% year over year to about $5.3 billion.

CEO Robert Ford said the following about the FreeStyle Libre during the company’s fourth-quarter earnings conference call: “In terms of sales dollars, Libre has become the most successful medical device in history, and it has outpaced market growth in 13 out of the last 16 quarters.”

Yet there is still a massive opportunity remaining in this field. There are more than half a billion diabetes patients (and rising) in the world, of whom only about 1% use CGM technology that enables them to constantly monitor their blood glucose levels, a crucial task for people with diabetes.

The lion’s share of diabetes patients are from developing countries or emerging markets, and Abbott hasn’t launched its FreeStyle Libre in many of those nations yet, so this shows the kind of long-term potential available to the company.

And it’s just one example. Abbott’s track record proves that it is an innovative company with what it takes to navigate the tricky and highly regulated healthcare industry.

Its financial results have been up and down in the past few years due to the effects of the pandemic, but the company has generally recorded consistently growing revenue, profits, and cash flow.

ABT revenue (annual) data by YCharts.

The Dividend King is currently on its 52nd consecutive year of payout increases. Abbott should continue rewarding its shareholders with regular dividend hikes for a long time.

2. Johnson & Johnson

Johnson & Johnson also has its share of problems, especially on the legal front. A new law in the U.S., the Inflation Reduction Act, could pose some issues for the company. This and other legal developments affected Johnson & Johnson’s performance on the stock market last year.

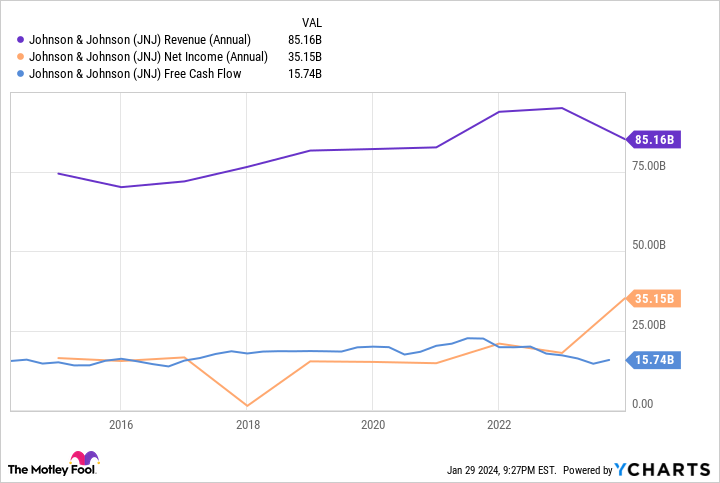

However, the drugmaker’s financial results remain pretty strong. In the fiscal year 2023, sales of $85.2 billion increased by 6.5% year over year.

Even putting aside the effects of acquisitions and divestitures, the pharma company’s sales jumped by 5.9%. Meanwhile, Johnson & Johnson’s adjusted EPS came in 11% higher at $9.92.

Management shed its consumer health business last year since it had, for a long time, become deadweight on its bottom line. The company’s goal is to focus more on its pharmaceutical and medical-device units. Within the former segment, Johnson & Johnson also suffered from declining sales of coronavirus products (specifically, vaccines) last year, but that’s a temporary problem.

Its pharmaceutical pipeline features 90 ongoing programs that sometimes lead to brand-new approvals. Last year, the company earned the green light for a novel cancer therapy, Talvey, which treats multiple myeloma in patients who have previously undergone four lines of therapy. The company sees peak sales potential of at least $5 billion for this new medicine, and there will be more.

The drugmaker also has multiple opportunities within its medical device division, including its Hugo robotic-assisted surgery system. Johnson & Johnson’s long-term results look solid despite the abnormality of the pandemic years.

JNJ revenue (annual) data by YCharts.

Meanwhile, the healthcare giant has raised its dividends for 61 years in a row, a fantastic streak that spans many recessions and countless other headwinds. In short, Johnson & Johnson is an incredibly reliable dividend payer, and that is unlikely to change anytime soon.

Q2 2024 Earnings Call Transcript")