No recession, no problem? Investors appear to be banking on the Federal Reserve embarking this year on a historically aggressive round of interest rate cuts even as the economy avoids a recession.

Fed policy makers have seen this movie before and didn’t care for the ending and investors may want to review the plot and adjust their expectations, said Nicholas Colas, co-founder of DataTrek Research, in a Tuesday note.

Fed-funds futures traders are pricing in five to six rate cuts of a quarter percentage point between now and the end of the year, in contrast to the Fed’s Summary of Economic Projections, also known as the “dot plot,” which calls for only three quarter-point rate cuts in 2024.

Economists have tied the aggressive rate-cut pricing to expectations the Fed will look to keep real, or inflation-adjusted, rates steady if inflation continues to decline. The Fed is widely expected to leave the fed-funds rate at 5.25%-5.50% when it concludes its two-day policy meeting Wednesday, with the market pricing in a better than 50% chance of a cut by the next meeting in March.

Related: Why analysts say the Fed risks clogging the financial plumbing without a policy change

Meanwhile, stocks have returned to all-time highs, with the S&P 500

SPX

and Dow Jones Industrial Average

DJIA

each logging their sixth record close of 2024 on Monday.

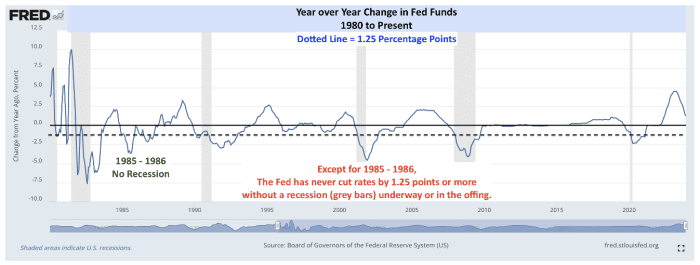

DataTrek took a look back at past easing cycles to see how market expectations for a decline of at least 1.25 percentage points over the coming year lined up with past easing cycles. As shown in the chart below, they found only one instance in the last 44 years in which the Fed cut rates by 1.25 percentage points or more within a year when a recession wasn’t under way or seen clearly in the offing.

DataTrek Research

It occurred in 1985-86. The Fed had lifted the fed-funds rate to 11.6% in August 1984 before beginning a mid-cycle easing program that took it to 5.9% by October 1986.

Those cuts added fuel to a stock-market rally, with the S&P 500 up 31% in 1985, up 18% in 1986, and up another 31% through the end of September 1987, Colas noted.

Students of market history know what happened next. Black Monday — Oct. 19, 1987 — saw the S&P 500 plunge more than 20% in a single day, while the Dow dropped 23%. The S&P 500 ended the fourth quarter of 1987 with a loss of 23%.

“The Fed knows the cautionary tale of 1985–1986 and, at lower absolute policy rates now, they have even more reason to be cautious about the pace of rate cuts in 2024,” Colas wrote. “Without an imminent recession, there is simply no precedent for +1.0 points of rate cuts this year.”

Moreover, “stocks are already doing well enough that the risk of sparking an unsustainable rally (a la 1987) is very high indeed,” he wrote.

Colas acknowledged the possibility that fed-funds futures are “trying to tell us something” about the potential for a recession.

Indeed, the seeming contradiction between fed-funds and other markets has attracted plenty of attention. Strategists at Deutsche Bank earlier this month noted that the degree of cuts factored in by the market have almost always been accompanied by recession, while the mid-1980s episode came after rates had been hiked into highly restrictive territory as the Paul Volcker-led Fed squeezed inflation into submission.

In One Chart: Why stock-market bulls should be careful what they wish for on Fed rate cuts

Colas, however, doubts the short-term rates market is sending up an economic warning flare.

Fed-funds futures traders “are likely betting that the Fed will want to become less restrictive as inflation continues to decline,” Colas said. “By the math, that’s fair enough. It does not, however, fit with either the historical data or the Fed’s institutional memory.”

Q2 2024 Earnings Call Transcript")