Nutanix (NTNX -0.47%) investors have witnessed a remarkable turnaround in the company’s fortunes this year, with shares of the enterprise cloud platform provider jumping an impressive 48% in 2023 thanks to its consistently solid growth.

The company is known for providing hyper-converged infrastructure (HCI) to clients so that they can integrate the different components of data centers, including computing, networking, storage, and management, into a software-defined platform. It was struggling in early 2022 thanks to hardware shortages that kept it from fulfilling its subscription contracts. But the scenario has changed big time in recent quarters.

Let’s take a closer look at what drove the terrific surge in Nutanix’s stock price this year.

Nutanix is making the most of a massive opportunity

Nutanix released fiscal 2023 fourth-quarter results (for the year ended July 31, 2023) on Aug. 31. The company’s revenue increased 18% for the fiscal year to $1.86 billion. Meanwhile, its fiscal Q4 revenue increased at a faster pace of 28% year over year to $494 million.

More importantly, Nutanix’s revenue pipeline improved at a healthy pace last quarter. This was evident from a 44% year-over-year spike in the annual contract value (ACV) billings to $279 million. According to Nutanix, ACV billings refer to the sum of the annual contract value of all contracts billed during the quarter. The faster growth in this metric compared to Nutanix’s revenue is a good thing, as this indicates that the company has been signing more contracts and setting up a solid future pipeline.

The growth in Nutanix’s billings also explains why its annual recurring revenue (ARR) increased 30% year over year in the fourth quarter to $1.56 billion. This also means that Nutanix is getting almost 84% of its total revenue from recurring sources, and that should help the company maintain its robust growth levels for a long time.

The key reasons why Nutanix is seeing healthy growth in the metrics discussed above include its growing customer base and an increase in spending by existing customers. The company finished the previous quarter with 24,550 customers, an increase of 9% over the prior year. But more importantly, Nutanix witnessed much faster growth in its large customer base.

The number of customers with more than $1 million in lifetime bookings increased 19% year over year to 2,183. Meanwhile, there was a 29% year-over-year spike in the number of customers with more than $10 million in lifetime bookings.

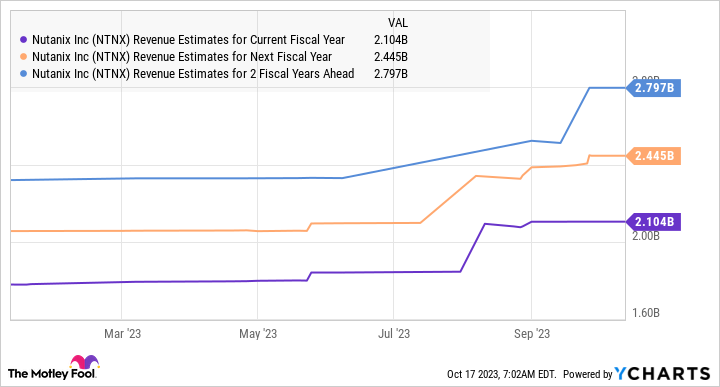

Nutanix investors can expect this impressive momentum to continue in the long run, as the company targets a massive addressable opportunity worth $30 billion in the HCI market. What’s more, Nutanix is one of the top players in the HCI market with a share of 25%, according to IDC. As a result, it is not surprising to see that the company’s growth is anticipated to remain healthy over the next couple of years following fiscal 2024’s projected revenue increase of 13% to $2.1 billion.

NTNX Revenue Estimates for Current Fiscal Year data by YCharts

How much upside can investors expect?

Nutanix stock currently trades at 4.8 times sales, which is slightly higher than its five-year average price-to-sales ratio of 4.2. But there is a good chance that the company’s growth could be better than what analysts anticipate given the large addressable opportunity on offer, as well as Nutanix’s solid share of the HCI market. So Nutanix’s sales multiple seems justified considering its bright prospects.

Assuming Nutanix does hit $2.8 billion in revenue in fiscal 2026, according to the chart above, and maintains its sales multiple of 4.8 after three years, its market cap could jump to $13.4 billion. That would be a 45% jump from current levels. But don’t be surprised to see this tech stock deliver stronger gains thanks to its improving customer base, higher spending by its existing customers, the long-term HCI opportunity, and its handsome share in this market.

Q2 2024 Earnings Call Transcript")