Toast (TOST 3.44%) is a little rough around the edges. The company has made a few notable missteps in recent quarters, adding friction to what could have been a triumphant rebound.

Instead, Toast’s stock still trades 66% below the all-time highs it set just before the inflation crisis started in 2021. The fast-growing provider of software tools and payment services for restaurant management is unprofitable and a downright controversial investing idea.

Even so, I think Toast is a fantastic growth stock to buy right now. Let’s explore the pros and cons of this disputed investment idea.

Why Toast’s stock is down

I mean, I get it. Toast introduced an unpopular consumer-to-Toast fee for processing online orders last summer, backing down only after substantial tumult among dissatisfied restaurant customers.

More recently, the company removed about 10% of its employees from the payroll. Management said that Toast had grown some parts of its team too quickly in the last three years, so a cost-cutting restructuring was in order. The move will result in severance-related charges of roughly $50 million in the first quarter of 2024 and lower annual operating costs by more than $100 million. If nothing else, the job cuts shone a spotlight on an imperfect estimate of Toast’s near-term workforce requirements.

Oh, and the company is under new (but very familiar) management. Co-founder Aman Narang took over the CEO office at the start of this year. It’s not a huge change, since Narang has been serving on Toast’s board of directors since founding it in 2012 and former CEO Chris Comparato also stayed on the board after the C-suite shift. Still, high-level changes can be uncomfortable and many investors see them as a sign of weakness.

So Toast recently misjudged the impact of a new fee, corrected a long-standing error in hiring practices, and picked a different CEO. Should you trust this company when it tells you how to run a café or when it’s appropriate to comp a meal?

More to the point, can you trust this unpredictable business to take good care of the hard-earned dollars you’re investing in its stock?

Yes, I get it. Toast has made some mistakes, and the stock price is arguably down for good reasons.

Why I see more opportunity than threat in this investment

Absolute perfection doesn’t exist. Getting a run out of every third pitch can get you into baseball’s hall of fame. reasonable mistakes can’t be deal-breakers, or I’d never buy any stocks at all.

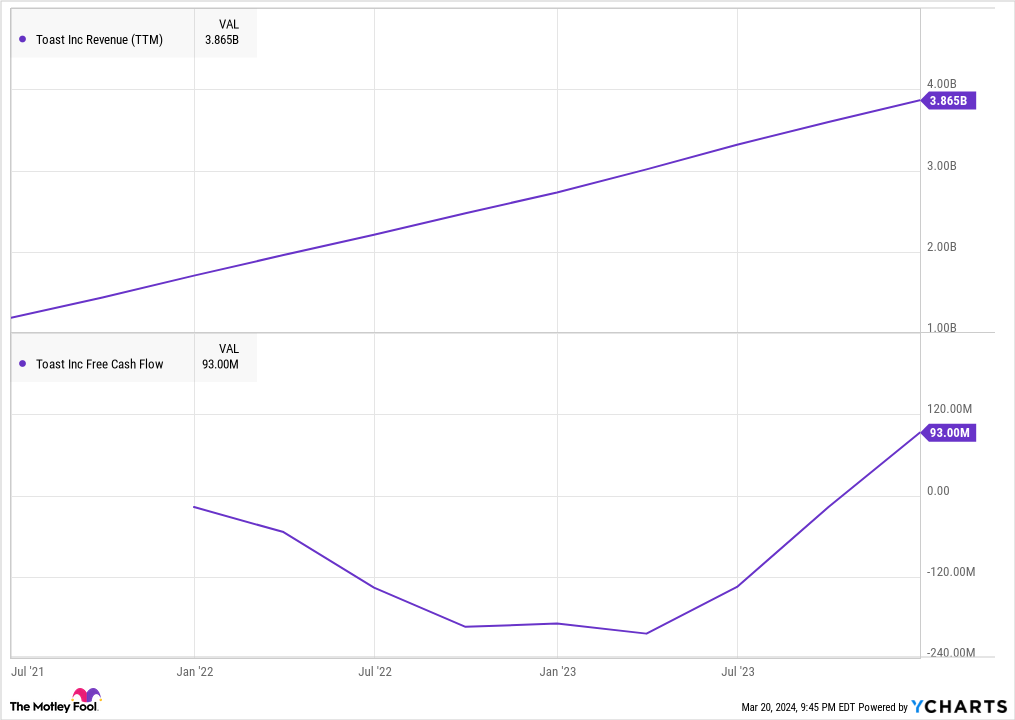

So I realize that Toast’s track record falls far short of perfection, but that really gives the company more room for improvement. And it’s actually a good start so far — have you seen Toast’s revenue growth and cash profits lately?

TOST Revenue (TTM) data by YCharts

Toast’s annual sales have more than doubled in two years and nearly quadrupled since 2020. The company boasts 106,000 customer locations and managed $126 billion of payment service transactions in 2023. As you can see in the chart above, free cash flows have turned positive recently.

And Toast is adding new customers on a premium scale. The latest big-name addition to the customer list was Caribou Coffee, the coffee-shop arm of the privately held Panera Bread group. If the Toast system pays dividends in these 811 locations, I’d expect sister companies Einstein Bros. Bagels (690 locations) and Panera (2,186 stores) to follow suit someday. This could be the start of a beautiful business relationship, and I’m sure Toast is talking to other household names behind the scenes, too.

I like Toast’s risk/reward equation

So this flawed little business is clearly doing something right. Perfection is only a dream but Toast’s real-world performance is more than good enough for me. In the meantime, its stock trades at the bargain-bin valuation of 3.3 times sales. Slower-growing sector peers such as Shopify and SoundHound AI are fetching several times that valuation ratio today. I should mention that SoundHound is a business partner, providing voice-control functions to Toast’s point-of-sale and drive-thru functions.

Long story short, Toast isn’t getting the market respect it deserves. The shares you pick up at a modest price-to-sales ratio today should deliver market-beating returns for years to come, as investors start to forgive the company for its early mistakes. I’m accepting the very real risk that Toast could commit more business errors in the future, but then again, no investment is risk-free.

In this case, the upside of Toast’s robust growth story far outweighs the modest downside of potential potholes in the road ahead. Hence, Toast looks like a great buy at today’s reasonable share price.

Anders Bylund has positions in SoundHound AI. The Motley Fool has positions in and recommends Shopify and Toast. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")