Eoneren

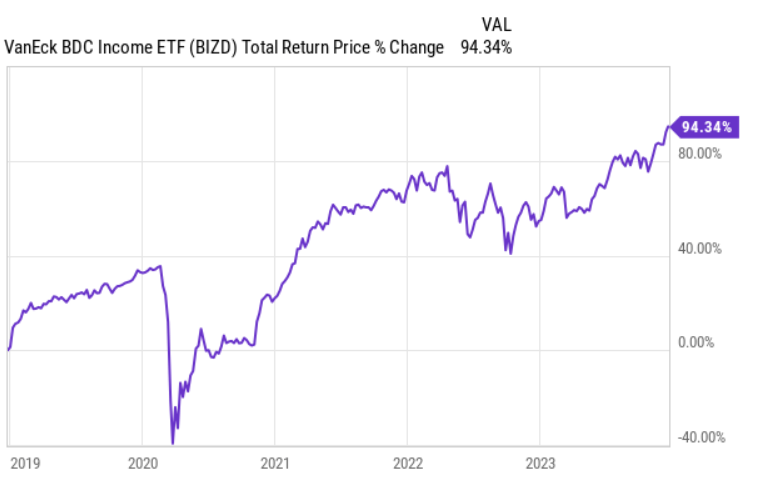

Since the recovery from COVID-19 and a shift in the interest rate policy, business development companies (BDCs) and private credit in general have performed extremely well.

YCharts

There are at least three structural forces that have formed very strong tailwinds for the sector:

- Constrained access to conventional financing as major banks are increasingly pulling back on their lending activities from riskier businesses amid tighter regulations, recent failures and looming recessionary risk.

- Elevated SOFR, which has allowed BDCs to require higher financing costs for the portfolio companies thanks to (commonly) the embedded floating rate component.

- Minimal write-downs as the credit quality of most below investment grade segment companies has remained sound, thus helping BDCs to preserve their NAV metrics.

As a result of these favourable dynamics and despite the recent run-up in the BDC share prices, the yields across the sector have stayed very attractive.

Global X Income Outlook September 2023

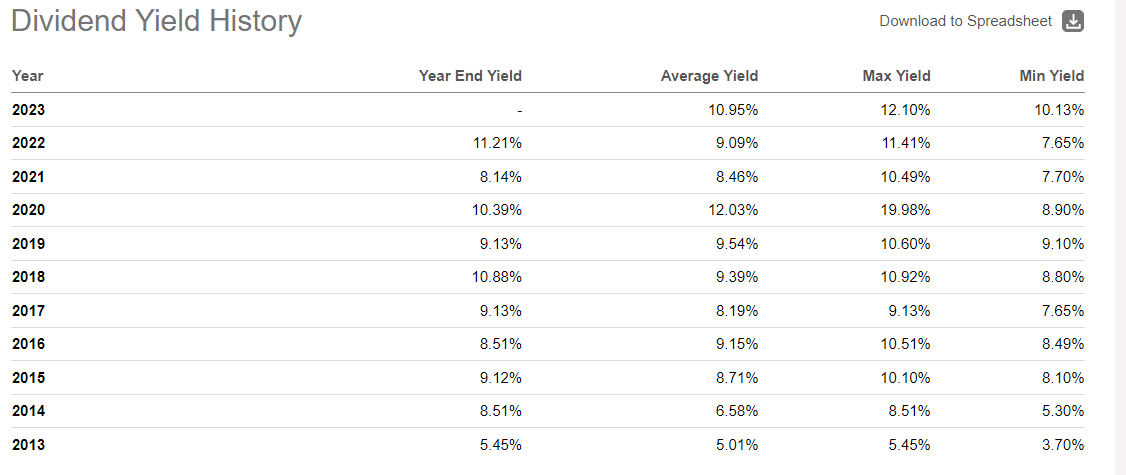

Even though the yields of most asset classes have marched higher offering more enticing current income, the distribution yield that stems from the average BDC exposure is still relatively attractive.

For example, the VanEck Vectors BDC Income ETF (BIZD) representing the overall BDC space currently yields 10.5%, which is clearly above the high yield bond benchmark.

What is even more interesting is that BDC yields are so attractive even after almost doubling in value in the past 3-year period. In fact, the yields, which we are experiencing now could be easily considered as one of the most appealing ones in the past decade.

Seeking Alpha

In other words, it seems that BDCs are finding themselves in a perfect goldilocks scenario with macro-level tailwinds in place that are complemented by historically attractive entry yields.

It’s only when the tide goes out that you discover who has been swimming naked

Earlier this year, Howard Marks gave an interview in which he reminded us of the potential consequences of riding the positive wave together with the overall market.

Howard Marks (billionaire, who is known for his private credit focus and is the co-founder of Oaktree Capital) has pinpointed that the boom in private credit will sooner or later be tested amid higher interest rates and a slowing economy.

The real question is whether the recent surge in the BDC lending activity was accommodated by a sound investment underwriting methodologies, which could protect BDCs of recognizing major write-downs once the struggles start to occur in the system. In this respect, Marks added:

Did the managers make good credit decisions, ensuring an adequate margin of safety, or did they invest fact because they could accumulate more capital? We’ll see.

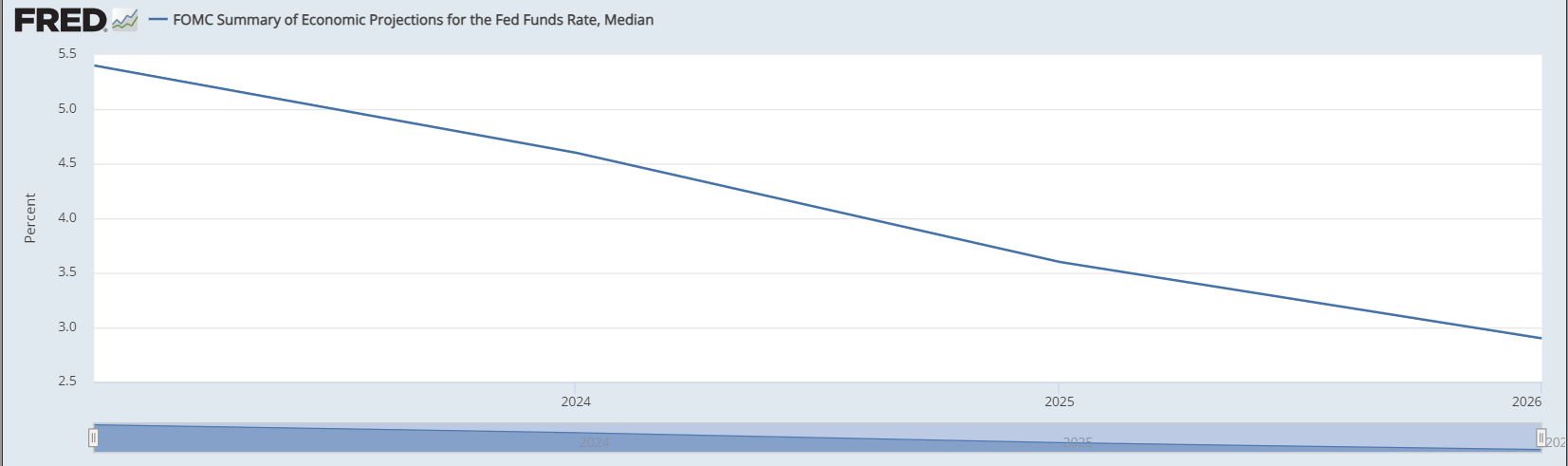

Interestingly, that the top-tier credit rating agency shares similar concerns. Fitch has provided a relatively negative 2024 outlook for BDCs referring to the deteriorating NAV base due to expected weakening in asset-quality metrics and increased debt-service costs resulting from higher interest rates for borrowers.

On top of this, I would add the current consensus of gradually normalizing interest rates, which should add an extra layer of pressure for BDCs to protect their yield levels.

FOMC; St. Louis Fed

All of this boils down to two fundamental questions:

- Will BDCs be able to sustain their NAV values in case of elevated corporate defaults in the economy?

- Will BDCs be able to keep the dividends at these attractive levels in case the Fed decides to cut interest rates aggressively over the foreseeable future?

Two BDCs to benefit from the current tailwinds in 2024, while keeping the risk profile in check

There are several principles, which, in my opinion, are critical to incorporate in BDC allocations against the backdrop of the aforementioned dynamics.

The essence is that on the one hand you want to have an exposure towards BDC factor to capture high dividends and benefit from the favourable environment, but on the other hand you want to make sure that the portfolio does not include some land mines that have been assumed in the process of growing the NAV base.

To have this in place, I have applied the following criteria in cherry-picking the right BDCs:

- No exposure to VC-type businesses, which have not yet reached cash flow neutrality and still are in a need of constant funding to survive.

- No exposure to life science segment, which increases the risk exposure as the probability of business success is inherently unpredictable.

- Focus in debt-like investments with very tiny allocations into equity (and preferably first lien).

- External leverage below industry average so that in the case of nonaccruals, the effects are not magnified too much.

Let’s now explore two BDCs, which match the aforementioned criteria and, in my view, embody solid prospects to deliver nice yield without introducing too much volatility and unpredictably in the portfolio.

#1 Gladstone Capital with a dividend yield of 9.5%

Gladstone Capital (GLAD) is one of those BDCs, which prefers convention and relatively predictable businesses. For example, if we look at GLAD’s investment policy, we will notice that a focus is put on defensiveness and not speculative VC-type funding:

- Proven business model

- Limited market and/or technology risk

- Potential to expand cash flow

- Diversified customer relationships

As a result, most of the sector exposures are associated with predictable segments of the economy, where lending can be made in a relatively more predictable manner.

GLAD Website Presentation

As a testament of GLAD’s conservative stance serves the historical track-record on the recognized write-downs.

GLAD Website Presentation

While most BDCs record 1.5-3% in non-performing loans, the fact that GLAD has managed to write down loans at about 50 basis points in the recent past is truly great.

As of Q3 2023, GLAD had more than 90% of its investments located in a combination of first and second lien debt instruments rendering quite low reliance on inherently unpredictable dividend income.

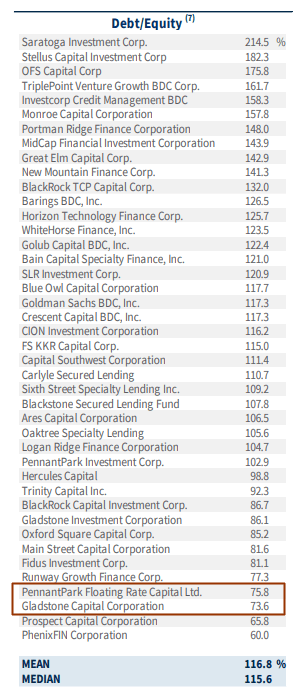

Finally, in terms of the external leverage GLAD carries one of the most resilient balance sheets in the BDC space. According to a recent Raymond James BDC report, BDCs on average apply 116% of leverage to magnify the underlying yields. GLAD is significantly below that with the leverage level of 75%.

#2 PennantPark Floating Rate Capital with a dividend yield of 10.3%

PennantPark Floating Rate Capital (PFLT) is another greatly structured BDC that is in a solid position to withstand any stress in the BDC segment and keep the dividend stability in check.

Just as for GLAD, PFLT’s portfolio focus is on cash generating companies with transparent and stable business models. In other words, no focus to speculative companies that would make it more difficult to weather any forthcoming BDC-wide storm (e.g., deteriorating asset quality).

PFLT Investor Presentation

As we can see in the table above, PFLT is not only rather diversified, but also protected from overly speculative type of businesses.

The majority of the AUM is invested in debt structures such as first and second lien instruments with the JV and equity component consuming ca. 5% of the total allocations.

Moreover, similar to GLAD, PFLT has assumed a relatively balanced reliance on the external leverage load.

Raymond James

In the context of the overall BDC segment, PFLT together with GLAD are classified as BDCs with one of the lowest debt to equity ratios.

Finally, the historic credit loss ratio of PFLT stands at only 15 basis points, which is even lower than in GLAD’s case. For instance, in the most recent quarter, PFLT was not forced to make any write down at all, thus confirming the resilient characteristics of its portfolio.

In closing

While the BDC segment has been a clear beneficiary of the prevailing macro environment and the growth prospects should theoretically remain sound, there are some valid concerns of overheating.

Even the well-known billionaire Howard Marks, who is recognized as one of the greatest masters in private credit, has highlighted potential red flags for BDCs. A top tier credit rating agency Fitch sends similar signals for 2024 (e.g., potentially deteriorating portfolio quality, which could come back to haunt those BDCs, which have relaxed their investment underwriting standards to maximize the current benefit of an attractive environment).

GLAD and PFLT are my top picks for 2024 that embody some of the most resilient portfolio characteristics and should be able to protect their high yielding dividends and NAV values in case of market distress.

Q2 2024 Earnings Call Transcript")