Olivier Le Moal

Intro

We wrote about TD SYNNEX Corporation (NYSE:SNX) back in June of last year when we were attracted to the company’s cheap sales and bullish forward-looking earnings revisions. A significant number of synergies were expected to come from the merger of Tech Data and Synnex (which took place in September 2021) which led us to stamp a ‘BUY’ rating on the stock at the time. However, shares unexpectedly have failed to gain any type of traction over the past 18 months as shareholders have only gained a 5.81% return on investment when dividend payments are included. This unattractive return demonstrates a sizable opportunity cost as the S&P 500 has returned over 18% since June’2022. Suffice it to say (for similar reasons we laid out in that article 18+ months ago), that shares continue to look very cheap from a valuation perspective but this remains only one side of the story. From a positive standpoint initially, as we see below, SNX remains very cheap from a sales, assets, cash-flow, and earnings perspective.

Valuation Remains Cheap

| Trailing Multiple | Trailing | Sector Median |

| Price To Sales | 0.17 | 3.10 |

| Price To Book | 1.18 | 3.25 |

| Price To Cash/Flow | 6.43 | 20.94 |

| Price To Earnings | 15.43 | 27.55 |

Furthermore, when one digs down into SNX’s cash-flow statement, we see (due to low capex requirements and sound working capital practices) that the company generated $1.1 billion of free cash flow over the past four quarters. This means the company’s trailing free cash flow multiple comes in at a very keen 8.8. The multiple informs us how much each dollar of free cash flow costs SNX at present. Such a low multiple demonstrates how much ‘extra’ revenue SNX is essentially generating at present. Value investors will also be looking at the attractive debt-to-equity ratio (0.49) & the fact that the recently announced secondary offering appears to be non-dilutive as stock is merely changing hands from major shareholders to the public. Furthermore, management continues to double down on its ongoing share repurchase program as well as reward shareholders through a growing dividend.

Capital Needs To Be Turned Over Faster

All of the above add to TD Synnex’s investment case but what will benefit the share price more over the next couple of years is how successful management will be in allocating capital effectively. There is no doubt (given the company’s strong free cash flow profile) that SNX will grow going forward. The question however is will the company will be able to grow consistently above its cost of capital (7% to 8%+). One would surmise that it will need to in order to produce real gains for its shareholders.

Therefore, although SNX deals with some large numbers (as illustrated through its ultra-low sales multiple), the net profit margin only comes in at 1.11%. Therefore to boost ROC, SNX has to turn over its capital faster than it has been doing. Nevertheless, top-line growth has not been helping in this endeavor. Net revenue fell by close to $1.4 billion in Q3 (over a rolling quarter basis) with Europe posting a decline for the quarter. We acknowledge that the company (in a negative top-line environment) still managed to grow its gross margin in Q3 as the product shift continues to tilt towards high-growth technologies but how long can this continue in a negative revenue environment is the key question here?

Suffice it to say, given the company’s inventory position ($7.5 billion at the end of Q3), receivables ($8.9 billion), interest-bearing debt ($3.3 billion) as well as goodwill & intangibles ($8.2 billion), capital must get turned over faster to ensure free cash-flow can remain elevated.

Technicals

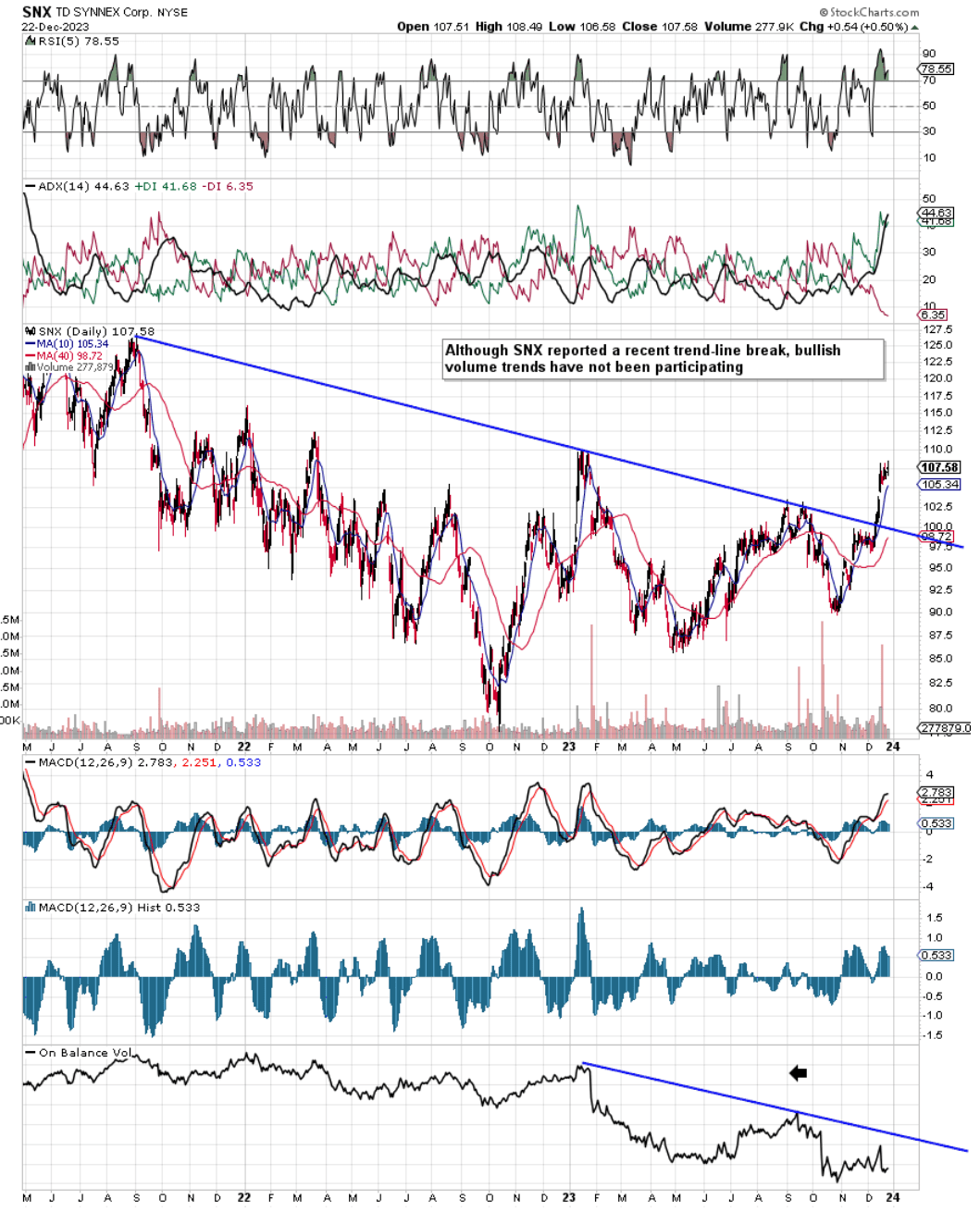

When we go to the technicals, we see that although shares recently broke out above long-term resistance, bullish volume trends have not been participating in the up-move. This is confirmed by observing that selling volume in recent months has been more aggressive on down moves as opposed to buying volume on corresponding up moves. Therefore, considering SNX’s negative top-line growth trend with the fact that bottom-line earnings (notwithstanding growing margins) have failed to gain traction since the merger in 2021, we are downgrading SNX to a ‘Hold’ until further developments.

Synnex Technical Chart (Stockcharts.com)

Conclusion

To sum up, although shares of SNX have seen 18%+ gains over the past 2 months, strong buying volume has not been participating in the rally. Although margins are on the rise, the company reported negative top & bottom-line growth in its recent third quarter. A sustained rally looks improbable here due to ongoing market challenges in Europe. Let’s see what the fourth quarter brings. We look forward to continued coverage.

Q2 2024 Earnings Call Transcript")