BMW Wirestock

Driven To A Tough Spot

While BMW’s (OTCPK:BMWYY) growth potential in China seems intact due to its large focus on selling premium automobiles, it faces an increasingly competitive environment in Europe as a result of an influx of Chinese mass-market EVs.

I wrote an article in Dec 2022 on the investment opportunity when the penetration of Chinese EVs in Europe was still nascent. My main investment theses were that (1) the market was underestimating its growth potential in China despite its electrification progress and (2) the market was overlooking BMW’s ability to capitalise on Internal Combustion Engine (ICE) vehicle demand.

However, the faster-than-expected penetration of Chinese EVs in Europe due to overcapacity in China poses a huge risk for BMW’s sales in Europe. The risk-reward doesn’t seem as attractive anymore, and I thus rate the stock as a hold.

Company Overview

BMW is a German premium automaker known for its automobile brands such as BMW, Mini, and Rolls-Royce. It also sells motorcycles and provides credit financing and leasing of vehicles through its Financial Services segment.

Underestimation of Growth Potential in China

About 30% of BMW’s revenue comes from sales in China. It is a fast-growing market for EVs due to both a rising, aspirational middle class and a government-led push for higher EV adoption.

One issue that the market seems to be concerned about is the competition from domestic EV brands in China. These tend to target the mass-market customer segment and are priced as such. BMW largely doesn’t compete with them because they target the premium segment. Furthermore, BMW has religiously tried to maintain its premium brand image – deciding not to cut prices in China unlike Mercedes (OTCPK:MBGYY) and Tesla (TSLA). BYD (OTCPK:BYDDY) is introducing a few premium models, but given that their brand is associated with the mass market, I doubt that they will be able to achieve the strong brand equity needed to cater well to the premium segment.

BMW CEO Oliver Zipse elaborated on the Chinese market in the Q2 2023 earnings call.

If you look below, yes, there is a lot of change coming on. In China, the electric cars are seen unlike in Europe, have seen something for the base segment. Cheaper cars have an electric drivetrain. This is how it operates in China. That is not the case in the upper, specifically in the premium market segment. There is a normal development like we see it in Europe or the United States, if you like at the complete market. So you have to really have to look with a magnifying glass in these 2 different market segments. And we — the majority of our cars are in the upper markets segment above RMB 350,000. On the lower end with MINI, we already have a joint venture, where with Great Wall, where we have a common platform for MINIs and for Great Wall. So to do a joint movement, joint development with Chinese manufacturers is not a new idea.

Of course, as I said before, we have to look with a magnifying glass in the lower base segment and the premium segment, there is a very solid brand-based premium market in China on the BEV side as well on the combustion engine side. And we will not slip down into the base segment. We have never done that, and there is no reason just because the biggest change in China is currently in the base segment that does not motivate us to slip down into the base segment.

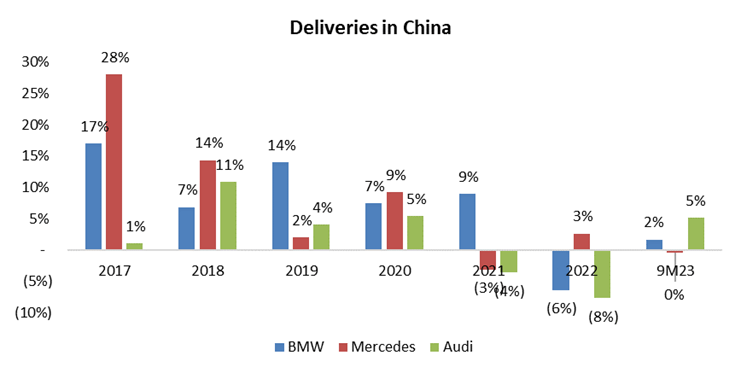

Despite not following through with price cuts, their deliveries in the first 9 months of 2023 have grown 2% year-on-year, which is an improvement from the 2022 slump.

Annual reports and press releases

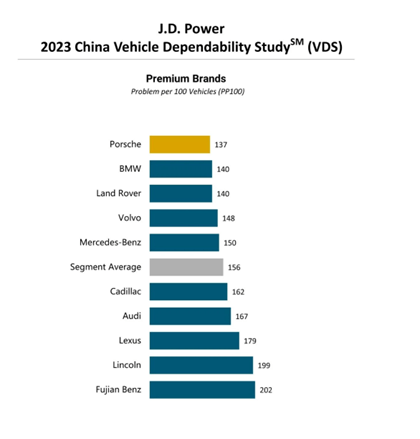

Moreover, a study by J.D. Power shows that BMW has retained its quality advantage over domestic brands (they have lower problems per 100 vehicles). It has improved from 147 in the 2022 study to 140 currently.

J.D. Power J.D. Power

Hence, I continue to believe that BMW will be able to grow its vehicle sales in China successfully due to its strong positioning in the premium segment and its quality advantage over domestic brands.

Overlooked Market Demand for ICE Segment

The market has been too focused on EV transitions, without considering continued ICE demand during the transition. In my previous article, I highlighted how BMW took a cautious approach to the ICE phase-out so that it will be able to capture both ICE and EV demand. Its competitors have pursued a more aggressive electrification strategy that will require a large upfront investment that’s irreversible. BMW, on the other hand, has developed mixed platforms so that it can easily pivot towards where the demand lies.

Indeed, governments have started to realise that their ICE bans may be premature. The EU has allowed for ICE vehicles to be sold beyond their 2035 phase-out if they are run exclusively on carbon-neutral fuels. The UK has also pushed back its deadline to 2035. Even Mercedes has had to push back their “50% of sales from electrified vehicles” target by a year. Moreover, dealers have faced some difficulties selling EVs. This could mean that the ability to sell ICE vehicles within the next decade could still be advantageous.

I believe BMW’s mixed platform approach will provide it with an advantage in ICE sales alongside its EV transition.

New Key Risk: Influx of Chinese Mass-Market EVs in Europe

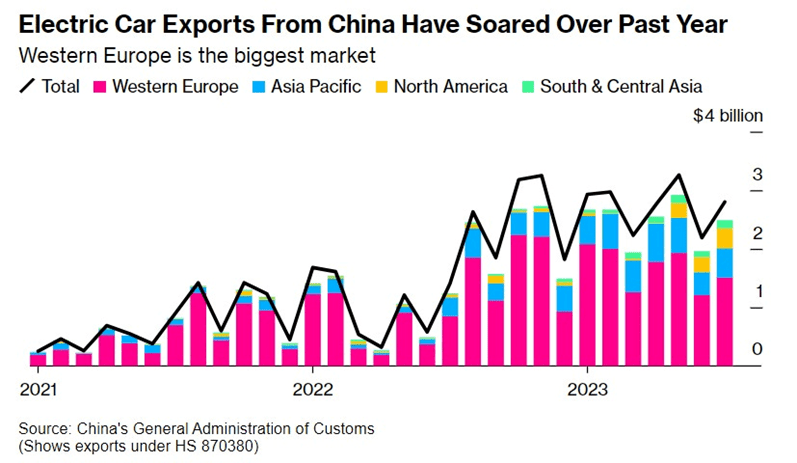

There has always been the possibility of Chinese EV brands taking market share in Europe, where BMW caters to both the mass-market and premium segments, unlike in China where the focus is mainly on premium. However, over-production of EVs in China in 2022 has led to a wave of cheap, mass-market EVs flowing into Europe quicker than expected.

Bloomberg

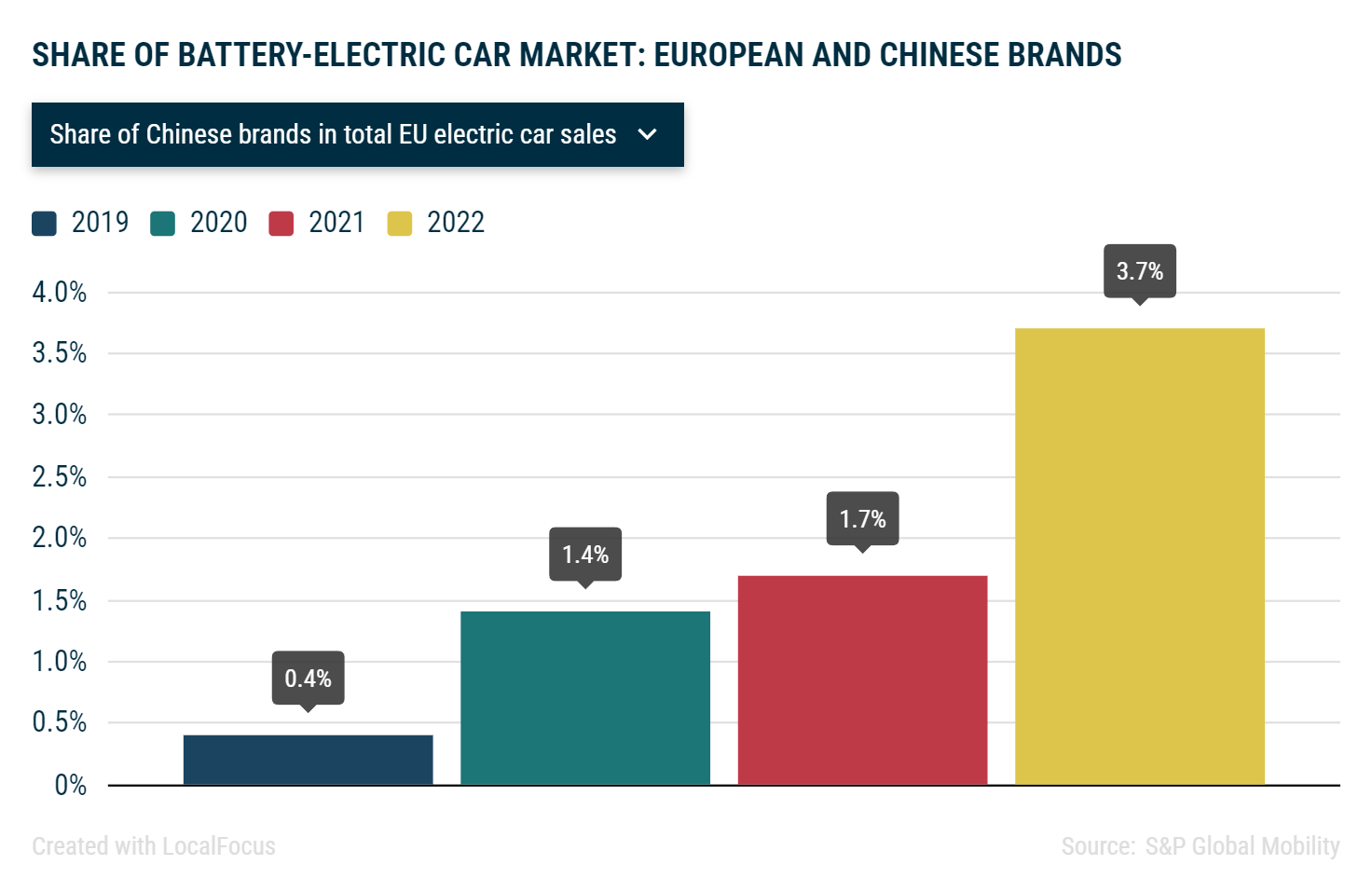

As shown below, the penetration of Chinese brands in the European EV market has increased substantially in 2022.

European Automobile Manufacturers’ Association

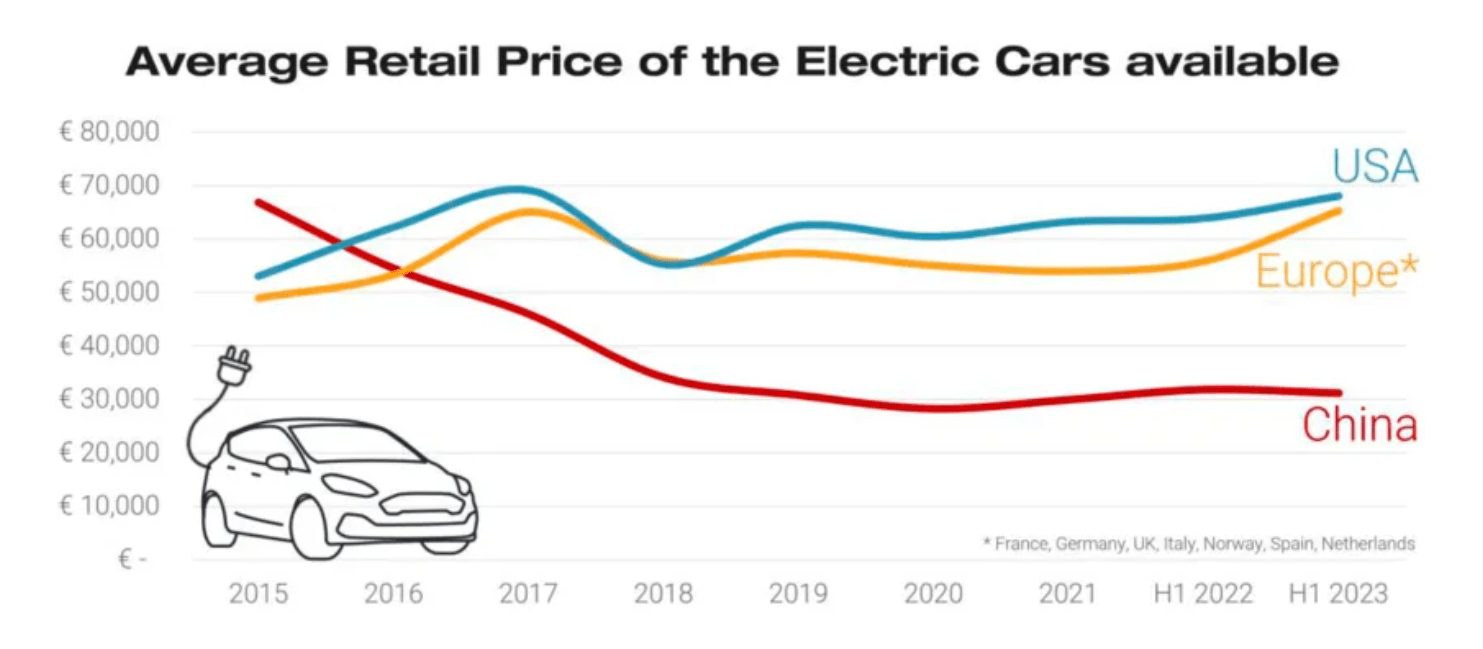

Chinese EVs Are Much Cheaper

These exported Chinese EVs are considerably cheaper than their European counterparts due to favourable government incentives in China, artificially lowering their costs.

According to research firm JATO Dynamics, EVs sold in China are roughly 40% cheaper than those sold in Europe. Even after import duties, these imported EVs from China are still considerably cheaper than European cars.

JATO Dynamics, Auto Express

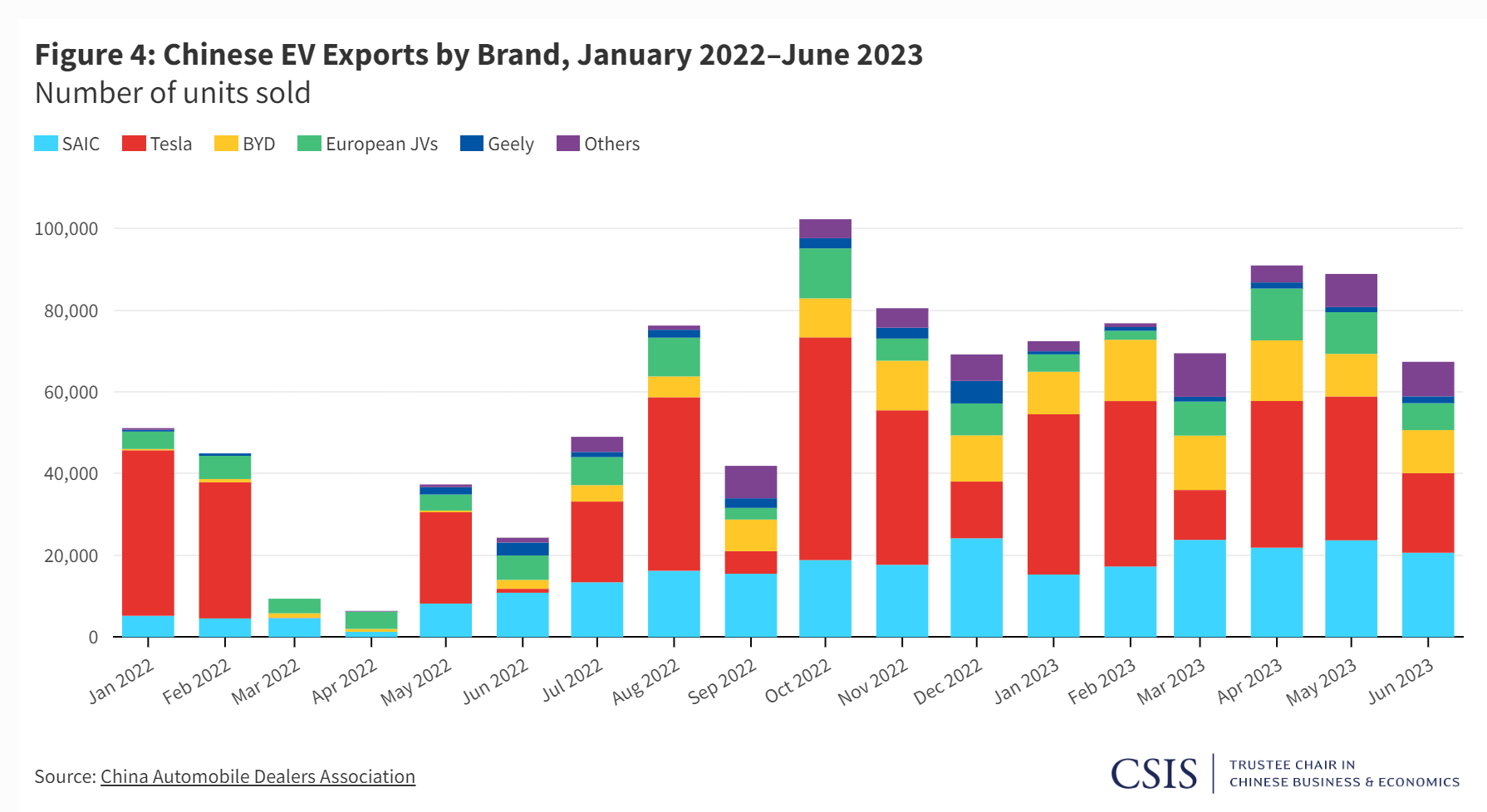

Increased Penetration, Led By Chinese-owned European Brands

Centre for Strategic and International Studies, China Automobile Dealers Association

Most of the Chinese EV penetration in Europe is likely to be driven by Chinese-owned European brands like MG and Polestar, which are owned by SAIC and Geely, respectively. These brands have a marketing foothold in Europe, while other Chinese brands may suffer from lack of brand recognition and poor customer perception. MG benefits from having a rich British heritage, so it is relatively insulated from the poor customer perception of domestic Chinese brands. Indeed, MG has been gaining traction and is now the second best-selling EV in the UK.

Given their cheaper prices and relatively similar technology, brands like MG and Polestar could continue to take market share. It may take some time for customer perception to change for domestic Chinese brands.

Annual reports and press releases

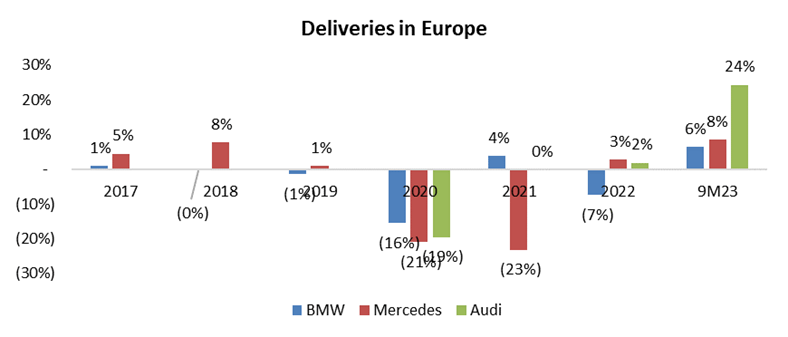

Although BMW managed to grow deliveries by 6% in Europe in the first 9 months of 2023, I don’t have conviction in BMW’s competitive advantage against these Chinese-owned European brands in the hyper-competitive mass-market EV space.

Valuation

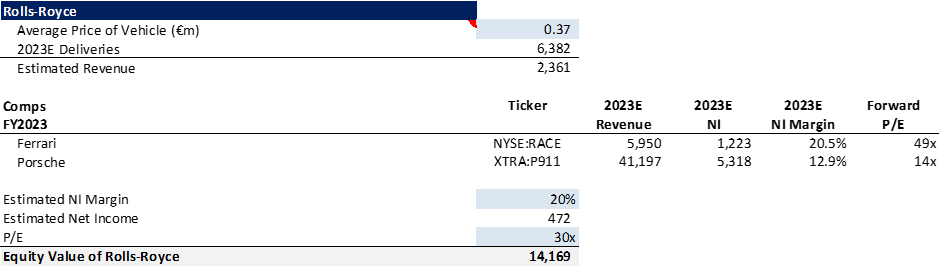

I use SOTP approach for valuation. For Rolls-Royce, I assume an average price of €370,000 per model (from collating prices on supercars.net). I get an estimated ~€2bn of revenue in 2023. I then assume 20% net income margin, similar to Ferrari, and use a 30x P/E multiple to achieve an equity value of ~€14bn.

My estimates, Capital IQ

For the Financial Services segment, it has grown its book value of equity at 9% CAGR from 2013-22. I use value this at 1x P/B to be conservative.

For the Automotive and Motorcycles segment, I estimate that net income is around €5.5bn for 2023.

Capital IQ

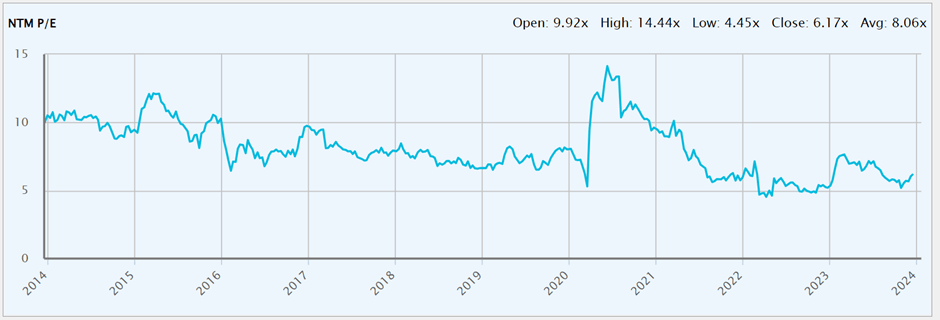

The chart above shows the NTM P/E multiple that BMW has historically traded at – the average is about 8x. I use 7x P/E to value the Automotive and Motorcycles segment, giving me a ~€39bn equity value for this part of the business.

My estimates

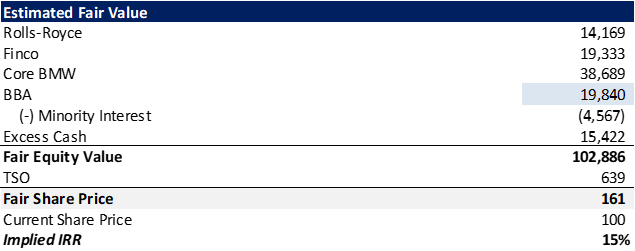

Putting it all together, we get a target share price of €161, leading to an upside of 62% and an implied 4-year IRR of 15%. If you’re purchasing the ADR, the target share price would be $59. I, therefore, rate this stock as a hold because of its mid-teens IRR and key risk of increasing penetration of Chinese mass-market EVs, which reduces the risk-reward skew.

Conclusion

While BMW’s growth potential in China is underestimated and its ability to meet demand for ICE vehicles is underappreciated, it faces increasing competition in Europe as Chinese EVs penetrate the market. At 15% IRR, there’s an insufficient margin of safety given the risk-reward skew. I thus rate the stock as a hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")