Daniel Balakov

Recently, I wrote a bearish article on the ProShares UltraShort S&P 500 ETF (SDS), arguing that inverse levered ETFs should not be held for the long-term, as they inevitably decay towards zero due to the inherent positive bias in markets and volatility decay. Does that mean the corrollary, that levered long market ETFs like the ProShares UltraPro S&P500 ETF (NYSEARCA:UPRO), are good long-term bets?

While levered long market ETFs like the UPRO have delivered very high compounded returns when measured over long time horizons, they are not suitable for long-term investors unless one has extremely high tolerance for pain (i.e. drawdowns). A common 15-20% drawdown in the markets can lead to massive 50-60% loss due to returns being magnified. Finally, while market crashes are rare, I believe a 40-50% market decline, like the one experienced during the Great Financial Crisis, can cause a 90%+ loss in UPRO.

In my opinion, levered ETFs like UPRO are only suitable for short-term tactical trading. However, with markets currently the most overbought in over 5 years, I would not recommend investors buy the UPRO ETF at the moment.

Fund Overview

The ProShares UltraPro S&P500 ETF seeks daily returns that are 3x the return of the S&P 500 Index (“Index”). The goal of the UPRO ETF is to magnify gains (and losses) and help investors achieve targeted exposure with less capital.

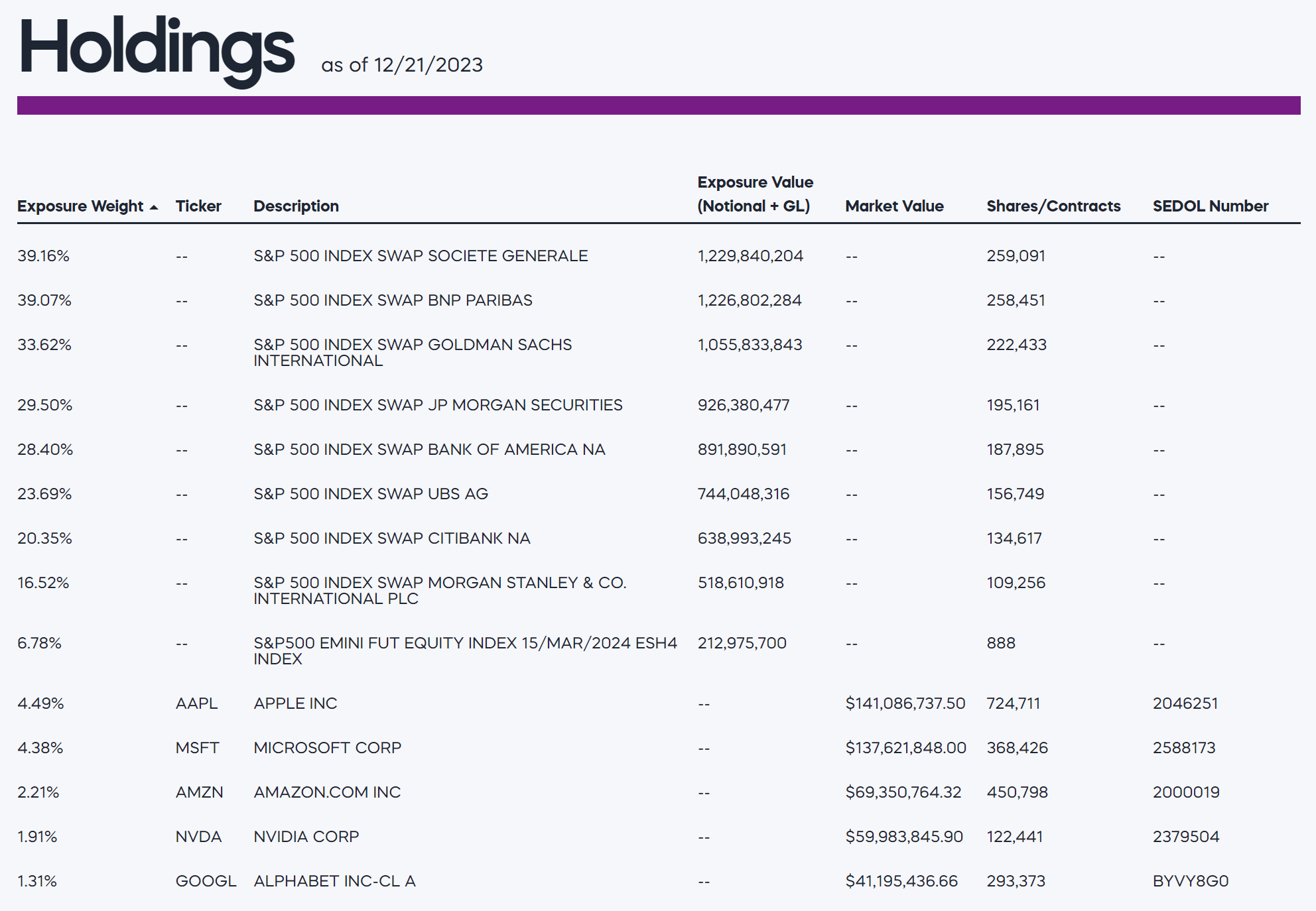

The UPRO ETF achieves its levered return by holding the stocks within the S&P 500 Index as well as entering into total return swaps with the large investment banks that are reset nightly (Figure 1).

Figure 1 – UPRO portfolio holdings (proshares.com)

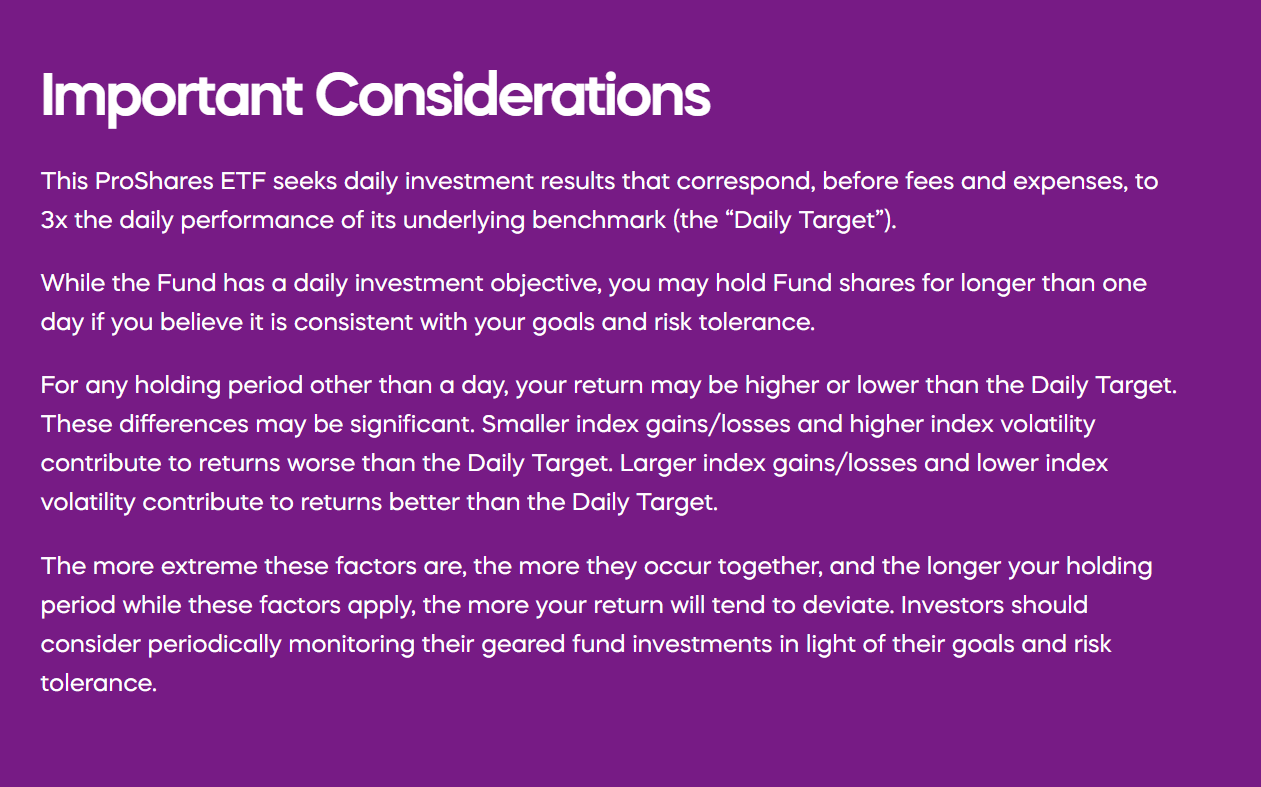

Similar to my warning on the SDS ETF, interested investors should read and understand this disclaimer from the ProShares website, as well as consult these warnings from FINRA and the SEC (Figure 2).

Figure 2 – UPRO disclaimer (proshares.com)

Levered ETFs Have Positive Convexity And Volatility Decay

Two main features of all levered ETFs are ‘positive convexity’ and ‘volatility decay’. Positive convexity refers to the fact that an investment in a levered ETF grows exponentially as price moves in favour of the bet. For example, assume we invested $100 into UPRO. If the S&P 500 Index rallied 5% on day 1, our position will grow to $115 (3 times 5% return). If the index rallied again by 5% on day 2, the position will grow to $132.25, more than three times the theoretical 2-day compounded return of 10.25% or $130.75. This difference between the ending exposure and the theoretical exposure is called positive convexity and is caused by the daily rebalancing of the ETF’s exposure to 300% of the index.

Positive convexity can also shrink one’s exposure. For example, if the index returns were consecutive -5%, then the initial investment will end up at $72.25, versus three times the 2-day compounded loss of 9.75% or $70.75.

On the other hand, if the return profile is 5% followed by -5% on the S&P 500 Index, investors end up with $97.75, significantly less than three times the 2-day compounded loss of 0.25% or $99.25. This loss in value is due to ‘volatility decay’.

While on a day-to-day basis, the positive convexity and volatility decay effects are small, when compounded over long periods of time, they can cause levered ETFs to deviate significantly from their underlying indices.

Also, the greater the volatility, the greater the value erosion. In fact, the ‘volatility decay’ can cause so much value erosion that many levered long ETFs had to change their leverage during the COVID pandemic as the daily rebalancing and extreme volatility caused many 3x levered ETFs to lose 90%+ of their value.

Levered ETFs May Be Useful For Swing Trading

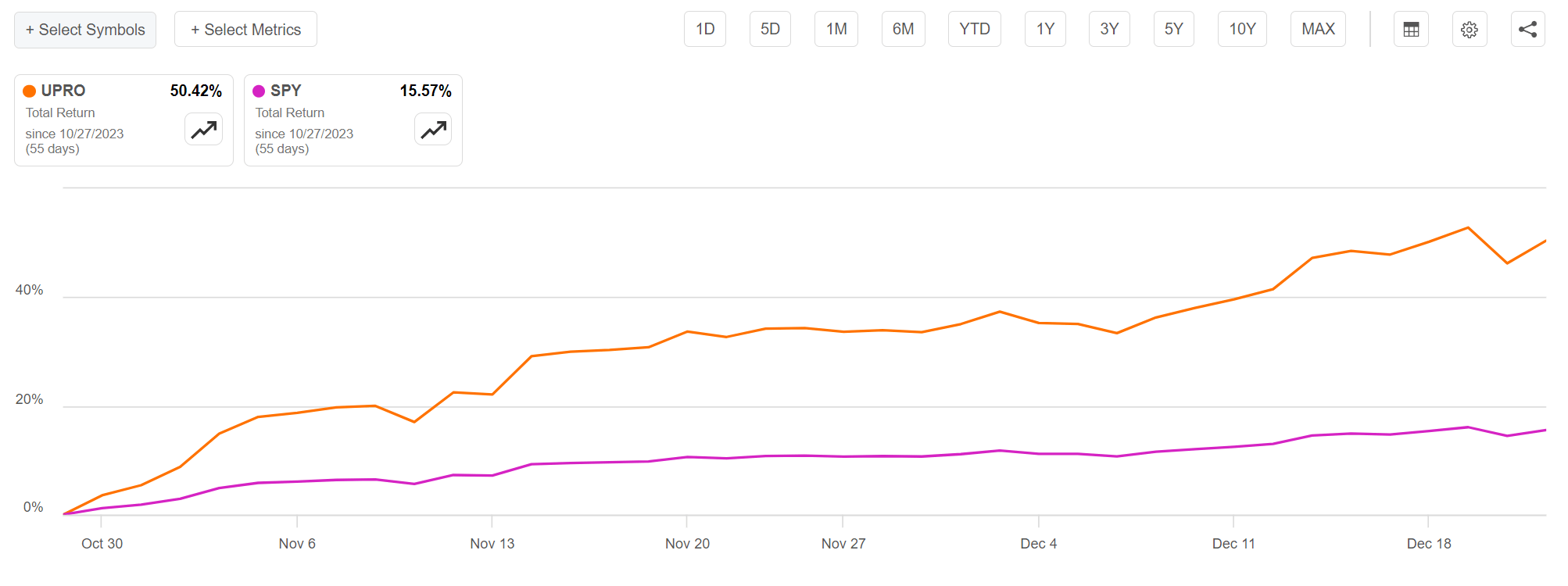

However, some nimble traders love to use levered ETFs for swing trading precisely because of their positive convexity. For example, measured from its recent swing lows on October 27th, the UPRO ETF has returned over 50%, more than 3 times the return of the SPDR S&P 500 ETF Trust (SPY), which has only returned 15.6% (Figure 3).

Figure 3 – UPRO vs. SPY, since late October (Seeking Alpha)

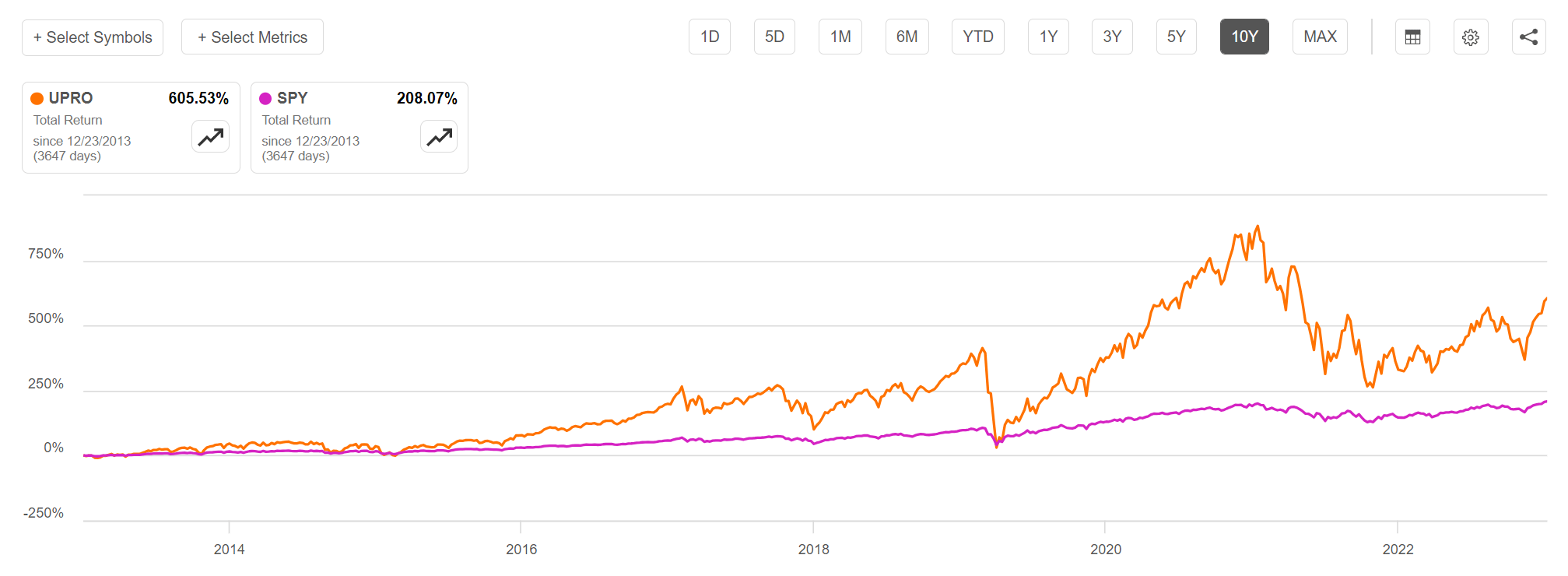

If we stretch out this comparison over even longer time horizons, the outperformance of UPRO can be even more striking. For example, when measured on a trailing 10 year basis, the UPRO ETF has returned over 600% compared to 200% for the SPY ETF, or roughly 3x the total returns (Figure 4).

Figure 4 – UPRO vs. SPY, 10 years (Seeking Alpha)

Why Don’t Investors Use Levered ETFs More Often?

However, there is a downside to levered ETFs, namely their magnified drawdowns. While the UPRO ETF can deliver 600%+ returns over 10 years, along the way, it has also experienced some nasty drawdowns, including a 60% drawdown during the 2022 bear market, a 77% drawdown during the COVID pandemic, and a 49% drawdown during the 2018 China trade war. I doubt there are any investors who can hold an investment through those levels of drawdowns and not flinch.

Furthermore, from simple math, we know that the bigger the drawdown, the harder it is to get back to even: a 20% drawdown will need a subsequent 25% return, a 40% drawdown will need a 67% return, and a 60% drawdown will need a 150% return. In a truly bad bear market like the 2008 Great Financial Crisis, it is conceivable the UPRO ETF could experience a 95%+ drawdown, since the S&P 500 Index fell almost 50% from peak to trough. A 95% drawdown will require a 2000% return to get back to even.

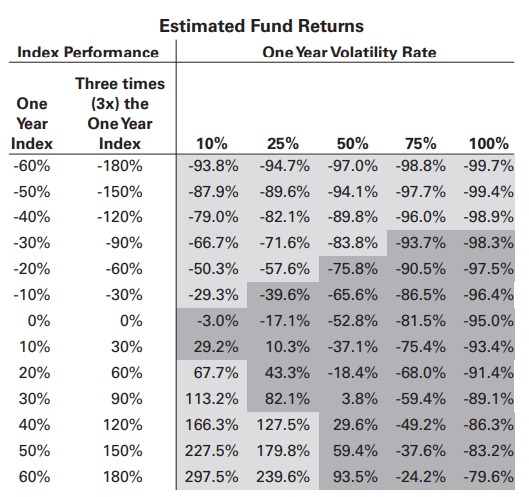

Based on ProShares’ estimates, if the underlying index fell 50% over 1 year (similar to the Great Financial Crisis), depending on the realized volatility, the drawdown on the UPRO could range from 88% to 99.4% (Figure 5).

Figure 5 – Estimated fund returns for UPRO depending on index returns and volatility (UPRO prospectus)

Therefore, in my opinion, levered long ETFs should only be used for short-term tactical trading by sophisticated investors.

Markets Extremely Overbought In The Short-Term

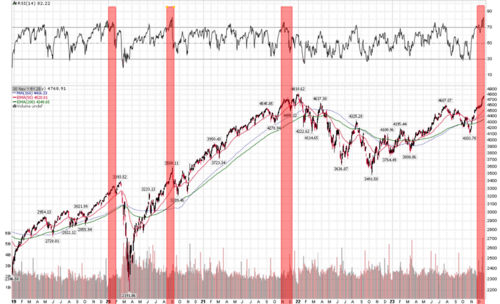

In the short-term, risk assets have gone virtually straight up since the beginning of November as investors anticipate the Federal Reserve cutting interest rates in 2024. On technical measures like RSI, the S&P 500 Index is the most overbought in the past few years and are prone to steep 1-day drawdowns like that experienced on December 20 (Figure 6).

Figure 6 – S&P 500 Index is extremely overbought in the short-term (Author created with price chart from stockcharts.com)

Historically, short-term market returns have been poor when they are this overbought so I would not recommend investors buy the UPRO ETF at the moment.

Conclusion

Levered long market ETFs like the ProShares UltraPro S&P500 ETF can deliver spectacular returns for sophisticated investors if timed correctly. However, the risk with levered ETFs is that they magnify returns, both positive and negative. If timed incorrectly, an investment in UPRO can lead to some eye-watering drawdowns.

In the near-term, I would advise against buying the UPRO ETF, as the S&P 500 Index is extremely overbought and historical short-term forward returns when markets are this overbought are poor.

I rate the UPRO ETF a hold.

Q2 2024 Earnings Call Transcript")