Joe Hendrickson

Summary

Following my coverage on The TJX Companies (NYSE:TJX), which I recommended a buy rating due to the business’s solid execution, continuous market share gains, and its ability to improve its margin profile, this post is to provide an update on my thoughts on the business and stock. I remain buy-rated for TJX as I see the business performing really well and being in a good position to continue growing. Near-term growth in 4Q24 should be a good one given its inventory position and the upcoming holiday season. There is also a viable path for the gross margin to expand.

Investment thesis

While the share price has not reflected my target price yet, I think the business performance is well on track. In 3Q24, TJX reported net sales growth of 9% Y/Y, better than consensus expectations of 7.6%. Margin performance was also better than expected, with gross margin coming in at 31.1%. On a net basis, the combination of the two drove a pre-tax profit margin of 12%, modestly beating the consensus estimate of 11.6%. In my opinion, 3Q24 performance sort of validated the growth momentum, and I expect this to continue through 4Q24, giving FY24 a good start. The reason for this belief is that top-line growth was mainly driven by traffic and not pricing. Increased traffic across banners drove TJX’s 6% comp sales growth in 3Q24. Marmaxx continued to perform well, and HomeGoods showed sequential improvement across income cohorts and regions. In particular, August and September were strong months, according to management. At the start of October, there was a little slowdown, but that was mostly because of the weather. As the month came to a close, the weather cooled, and traffic trends turned around. There is a key distinction between traffic-driven growth and price-driven growth, as the former is more sustainable, implying TJX product offerings are reasoned with consumers in this spending environment (i.e., the trade-down trend benefits TJX). This strong traffic trend led me to believe that TJX will see a strong 4Q as the holiday season will drive elevated traffic given TJX’s value offerings.

I also expect gross margins to continue expanding as management noted stronger merchandise margins driven by better freight expenses and leverage on higher-than-planned sales. These positive impacts more than offset the negative impacts from shrinking accruals and investments in the supply chain. As for cadence, in the near term, gross margin should see an acceleration as TJX continues to recapture the freight headwind that it has encountered in FY20. So far, TJX has already recaptured around 200 bps of the 300 bps freight headwind. That said, I think it is unlikely for TJX to recapture 100% of the remaining 100bps as the cost structure in the freight network is elevated due to the tight labor market (high wage). Until the labor market eases, it seems like a minor portion of the freight headwind will become a structural mid-term headwind. That said, there are other drivers of gross margin expansion that could outweigh this. For instance, improvements in logical efficiency (moving goods from DC to stores). TJX has a good track record of improving gross margins over the years, so I have faith that they will be able to find ways to improve efficiency. Also, I like the fact that management pulled their resources out of HomeGoods’ e-commerce business as there was no viable path to profitability. Because of this pullout, 3Q24 saw an acceleration in costs (costs related to ending the business), which should repeat in the coming quarters.

“Yeah. So the costs associated with that were mainly cost to shut the business down.” 3Q24 earnings results call

Finally, any concerns regarding TJX’s ability to meet the festive season demand should have been eased with the TJX 3Q24 balance sheet results. While TJX ended 3Q24 with an inventory decline of 0.5%, this is not a problem as inventories on a per-store basis are flat. Importantly, I note that management has specifically called out that they have a variety of products that can continuously update their store shelf multiple times a week to offer consistent newness during the holiday season. Additionally, remember that Christmas is on a Monday this year, unlike last year when it was on the weekend. As such, TJX should see an additional working day that is a public holiday, which means an additional day of better traffic vs. last year.

Valuation

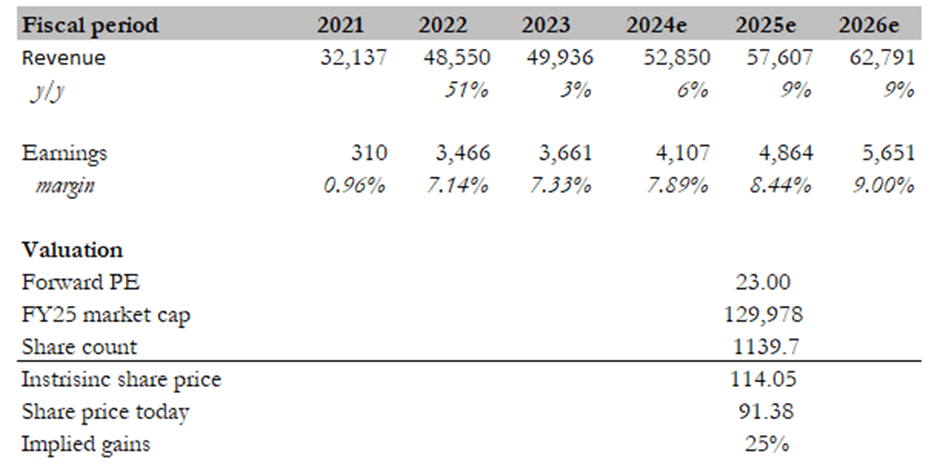

Own calculation

My target price for TJX has increased from $107.44 to $114.05. The increase was due to my more optimistic growth outlook of 9% for FY25 and FY26, as I believe TJX is in a much better position than I had originally expected. The macro situation today vs. back then is also much better, with inflation coming down and the labor market slightly improving. These all bode well for the consumer spending environment, which is positive for TJX. While I have a positive view of margins, I am not updating my margin expectations as the bottom line is conservative. Any upside at the margin line would be positive for stock upside. I have talked about the relative valuation for TJX against its peers (Ross Stores and Burlington Stores) previously, and I think TJX continues to trade at the right multiple at 23x. It deserves to trade at a discount to Burlington Stores (27.5x) because of its lower growth and margin, and it is similar to Ross Stores because they have similar growth and margin.

Risk

Though inflation rates have come down dramatically, the labor market remains very strong, and my worry is that this might cause the current freight and wage costs to become permanent or go even higher. This could be a structural impairment to the TJX margin profile relative to the past.

Conclusion

In summary, I like that TJX’s growth was driven by positive traffic trends. Despite the stock price not yet reflecting my target, note that performance remains robust. Gross margin also has room to further expand if TJX can find ways to improve efficiencies, overcoming the impact from elevated freight cost. All in all, I maintain my buy rating on TJX.

Q2 2024 Earnings Call Transcript")