BrianAJackson

Introduction

Today, I’d like to talk to you about a small-cap company that goes by the name of Nelnet (NYSE:NNI). It’s a company often recognized for its role in student loans, but it’s been increasingly successful in diversifying its business into new business segments.

Despite a general trend away from the conglomerate structure in the US, apart from a few outliers such as Berkshire Hathaway (BRK.B), Nelnet has decided to buck that trend by utilizing stable student loan-related revenues to fund new business ventures.

Beyond its core student loan business, Nelnet successfully diversified into financial services, education technology, and communications. While there were some challenges this past quarter linked to its stake in Allo Communications, Nelnet’s conglomerate structure provides stability and the potential for long-term growth.

For investors open to a conglomerate corporate structure, I believe you would do well to get accustomed to Nelnet, as I believe there is massive potential in this investment.

Let’s dive in.

Company Overview

Nelnet is often recognized as a student loan processor, but there’s a whole other side to this company that many might not be aware of. Beyond the familiar realm of student loans, Nelnet diversifies into several other industries.

In its Financial Services division, Nelnet manages a substantial $559 billion in loan volume. This division is not just limited to student loans but also delves into government and consumer loan servicing. The 2020 launch of Nelnet Bank, which now oversees $14 billion in net loan assets, marked a significant expansion in their financial services.

Apart from its well-known role in student loans, Nelnet also operates a Business Services sector. This arm of the company is dedicated to supporting educational institutions through payment processing and technology services, extending its reach to thousands of schools and universities.

Additionally, Nelnet is making strides in the Communications Services sector through its partly-owned subsidiary, Allo Communications. This division represents a move beyond their traditional scope, offering fiber optic network services that include broadband and television, particularly focusing on areas that are typically underserved.

Industry Overview

Nelnet’s diverse operations not only shape but are also shaped by the student loan processing, vertical market software, and fiber optic network industries. Let’s examine these industry dynamics in the context of Nelnet’s activities.

Student Loan Processing Industry

First, the student loan processing industry, vital for managing and collecting loan payments, is significantly influenced by companies like Nelnet. They play a crucial role in the collection of student loan payments and earn fees from the government for their services. This industry is essential for the financial management of higher education funding.

One risk that has been looming over Nelnet is the prospect of widespread student loan forgiveness. However, I believe that such action is politically improbable, given the deep divisions within Congress and the American public on this issue. While the idea of student loan forgiveness has garnered attention, the complex and divisive nature of the topic makes it unlikely to see a sweeping, nationwide solution in the near future.

That said, the threat of widespread cancellation cannot be fully dismissed. The goal of widespread debt cancellation remains a top priority for main democrats, and while it was blocked by the Supreme Court this around, if the democrats were able to consolidate power in the legislature and white house, I believe they would be likely to push this goal again.

If this were to happen, it could rapidly upend the largest part of Nelnet’s business, making it critical for investors to monitor.

Vertical Market Software Industry

In the vertical market software industry, companies develop specialized software for specific sectors. Nelnet’s entry into providing technology solutions for K-12 and university markets is a strategic move, offering a steady source of recurring revenue. Given the niche nature of these solutions, companies like Nelnet face less competition, allowing for deeper market penetration and stability.

One risk facing Nelnet’s endeavors in the VMS industry is the advancement of AI and low-code software solutions. As these tools develop, a risk exists that organizations may choose to develop, build, and own their IT solutions instead of outsourcing them to companies like Nelnet due to a future lower development cost.

Author’s Note:

For those interested in delving deeper into the world of Vertical Market Software (VMS) businesses, a prior article I wrote offers a comprehensive exploration. It sheds light on the unique strategies, financial dynamics, and market impacts of VMS companies, illustrating how they’re reshaping industry landscapes through strategic acquisitions and niche market dominance.

Fiber Optic Network Industry

The fiber optic network industry focuses on delivering high-speed internet and communication services. Companies in this sector, including Nelnet, often target underdeveloped areas where competition is minimal. This strategy allows them to exert greater pricing power and achieve potentially higher profit margins, capitalizing on the demand for advanced digital connectivity. Nelnet’s communication business is operated by its partly-owned subsidiary, Allo.

One risk facing Nelnet’s Fiber Optic endeavors is the fact Allo is no longer majority-controlled by Nelnet. While selling a large stake in the business freed up a ton of capital, it ultimately means that the future of the business is out of Nelnet’s hands.

Quarterly Earnings Update

Turning to its recent earnings report, in Q3 2023, the company reported a GAAP net income of $45.3 million, a significant drop from the previous year’s $104.8 million. EPS came in at $1.15, falling short of expectations by $0.25, and revenue declined by 16.62% year-over-year to $329.52 million.

This quarter, Nelnet’s earnings per share were adversely affected by a loss from its 45% stake in Allo. The company reported a loss of $17.3 million ($13.1 million after-tax), a setback that contributed to an earnings dip compared to a similar loss in the same period last year.

Due to the interests that Nelnet has in partly owned entities, earnings at the company are subject to volatile swings, as with similar companies like Berkshire Hathaway. While this can make it a challenge to analyze the business performance, I would suggest investors take that challenge rather than avoid it due to the perceived complexity.

I’ll provide a more nuanced view later on in this article.

Over the last reported quarter, the Loan Servicing and Systems segment saw a decrease in revenue to $127.9 million, down from $134.2 million in the previous year. However, this segment’s net income after tax improved to $18.6 million, compared to $16.7 million in the same period last year.

In contrast, the Education Technology, Services, and Payment Processing segment experienced growth. Revenue increased to $113.8 million from $106.9 million year-over-year, and net income after tax rose to $16.8 million, bolstered by higher interest rates in 2023. This shows the strength of the company’s technology endeavors.

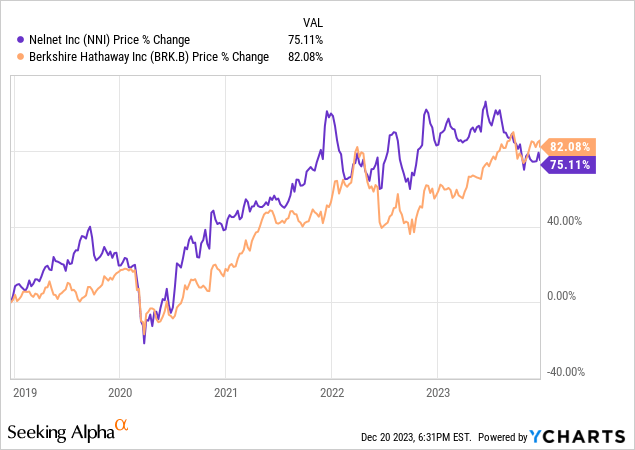

Nelnet vs Berkshire Hathaway

Nelnet’s earnings results highlight the benefits of its conglomerate structure in a way that I feel is similar to Berkshire Hathaway’s model, perhaps the most well-known conglomerate in the US. This diversity across various sectors allows for a balanced business approach, offsetting fluctuations in individual segments and stabilizing overall performance.

This strategy contributes to Nelnet’s resilience and steady growth, even in challenging market conditions.

Expanding on Nelnet’s strategic approach, while the company may not match the scale of a conglomerate like Berkshire Hathaway, its initial foray into corporate diversification has been promising. Nelnet has astutely ventured into other business lines, carefully selecting sectors where it can establish strong competitive advantages.

This strategy mirrors the early stages of Berkshire Hathaway’s growth, where diversification played a key role in building a resilient and successful business model.

For Nelnet, this approach has already shown early signs of success, indicating potential for long-term stability and growth. By branching out into various industries with distinct competitive edges, Nelnet is positioning itself to withstand market fluctuations and capitalize on diverse revenue streams, much like the other conglomerates.

Valuation

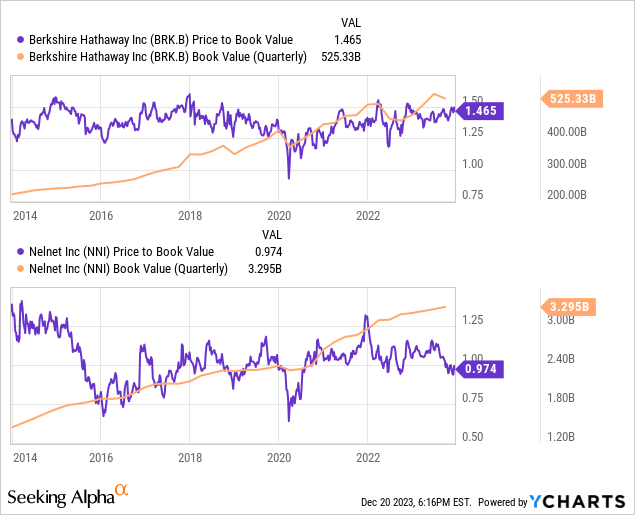

With a price-to-book value of less than 1x and price-to-operating cash flow per share of just 8.45X, I consider Nelnet to be a deep-value stock. I believe that evaluating the company on a strict price-to-earnings basis obscures the true opportunity that exists due to the impact its investments will have on GAAP earnings.

While the company has more work to do in order to show sustained growth in operating cash flow, I believe the initial signs are positive, and the business model as a whole is sound.

Conclusion

Nelnet’s diversified operations, spanning beyond student loans into financial services, education technology, and communications, offer a compelling investment opportunity. While Q3 2023 earnings faced challenges, the conglomerate structure provides greater financial stability.

With a price-to-book value below 1x and a price-to-operating cash flow per share of 8.45X, Nelnet is a deep-value stock, and its strategic investments signal long-term growth potential.

I rate Nelnet a “Strong Buy.”

Q2 2024 Earnings Call Transcript")