MadamLead

A little more than a year ago, I wrote an initiation article on the DNP Select Income Fund (NYSE:DNP). Although the DNP fund was paying an attractive $0.065/month distribution, I cautioned investors against investing in the fund as I felt Utility Sector valuations were at an extreme and the DNP fund was trading at an unjustified premium to its net asset value (“NAV”).

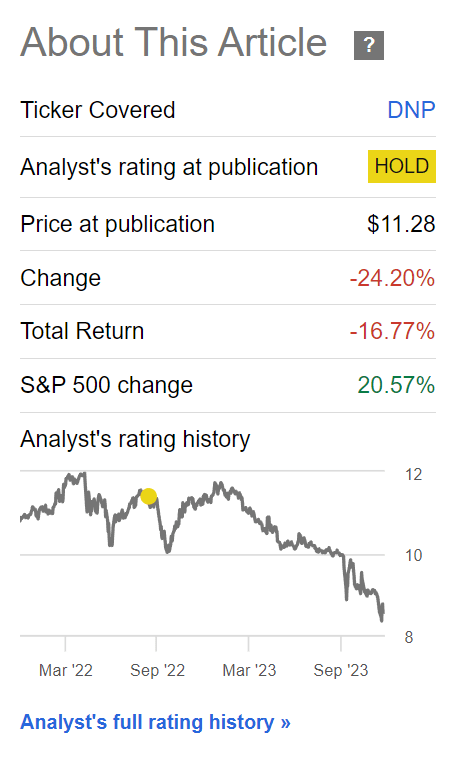

Since my article, the DNP fund has had a rough year, losing approximately 17% in total returns compared to 20% gains in the S&P 500 (Figure 1).

Figure 1 – DNP has massively underperformed in the past year (Seeking Alpha)

DNP’s poor performance can be attributed to a combination of normalization in sector valuations, as well as a contraction in the fund’s premium to NAV. With more than a year gone by, let’s revisit the DNP fund to see if it is attractively priced now.

Brief Fund Overview

The DNP Select Income Fund is one of the most popular closed-end fund (“CEF”) in the market with $2.7 billion in net assets (Figure 2).

Figure 2 – DNP funds under management (DNP annual report)

The DNP fund’s popularity stems from the fact that it has paid a consistent $0.065/month distribution for close to 3 decades.

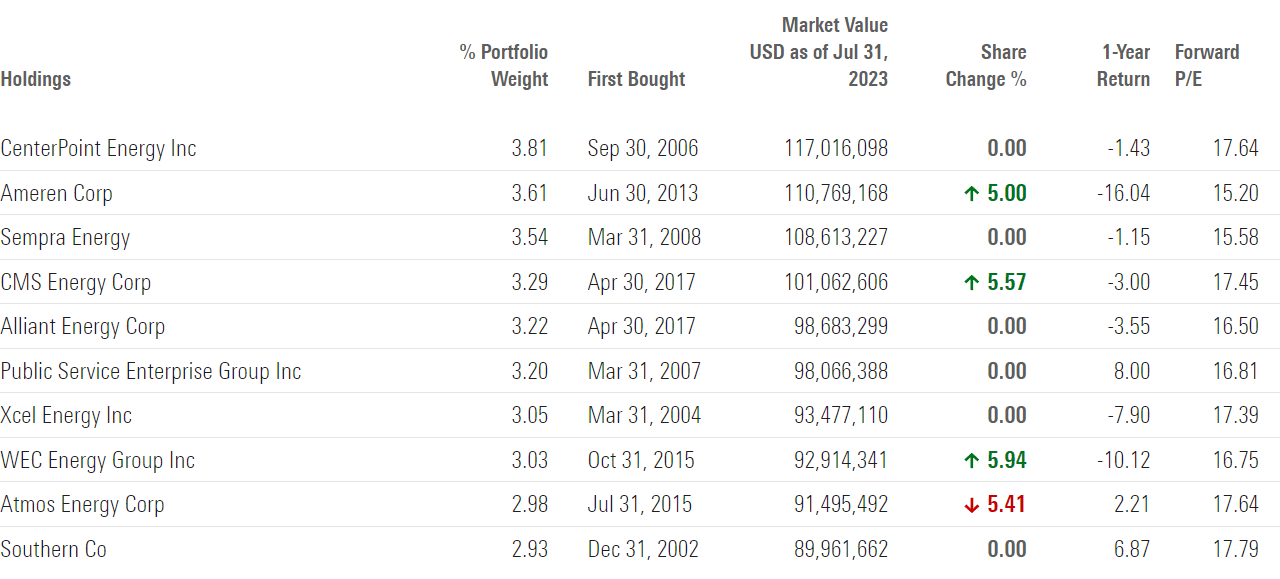

At a high level, DNP’s portfolio and strategy remain unchanged as it continues to focus on utility stocks, with a small allocation to corporate bonds. However, in the past year, there have been small changes in the fund’s top 10 holdings, with WEC Energy (WEC), Atmos Energy (ATO), and The Southern Company (SO) replacing American Electric Power (AEP), Eversource Energy (ES), and Dominion Energy (D) (Figure 3).

Figure 3 – DNP portfolio current top 10 positions (morningstar.com)

Upgraded Utility Sector On Relative Valuations

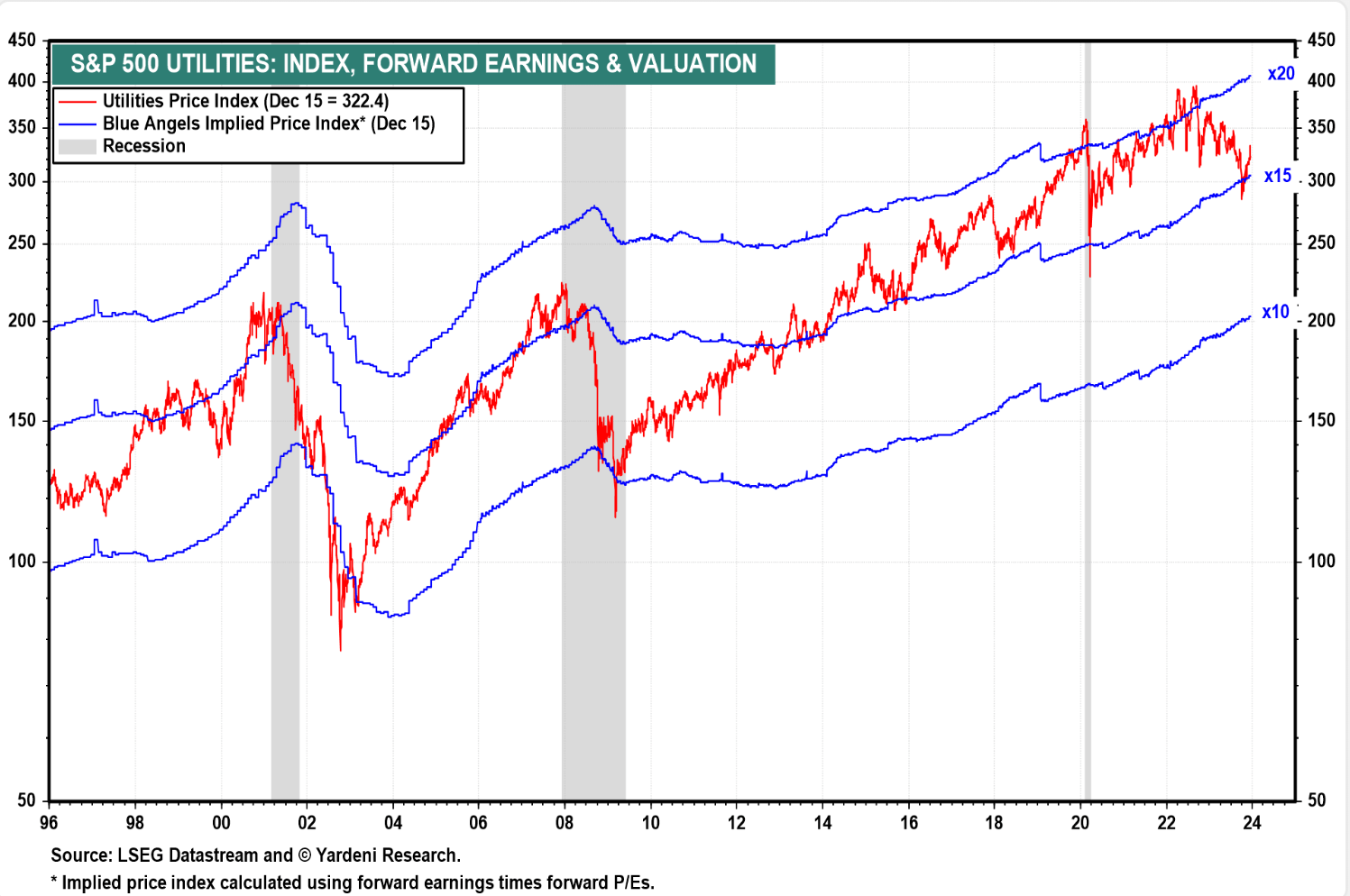

While Utility Sector valuations were trading at all-time highs > 20x Fwd P/E when I wrote about them in September 2022, valuations had fallen to < 16x Fwd P/E recently when I upgraded the sector in late September 2023 (Figure 4).

Figure 4 – Utility Sector valuations (yardeni.com)

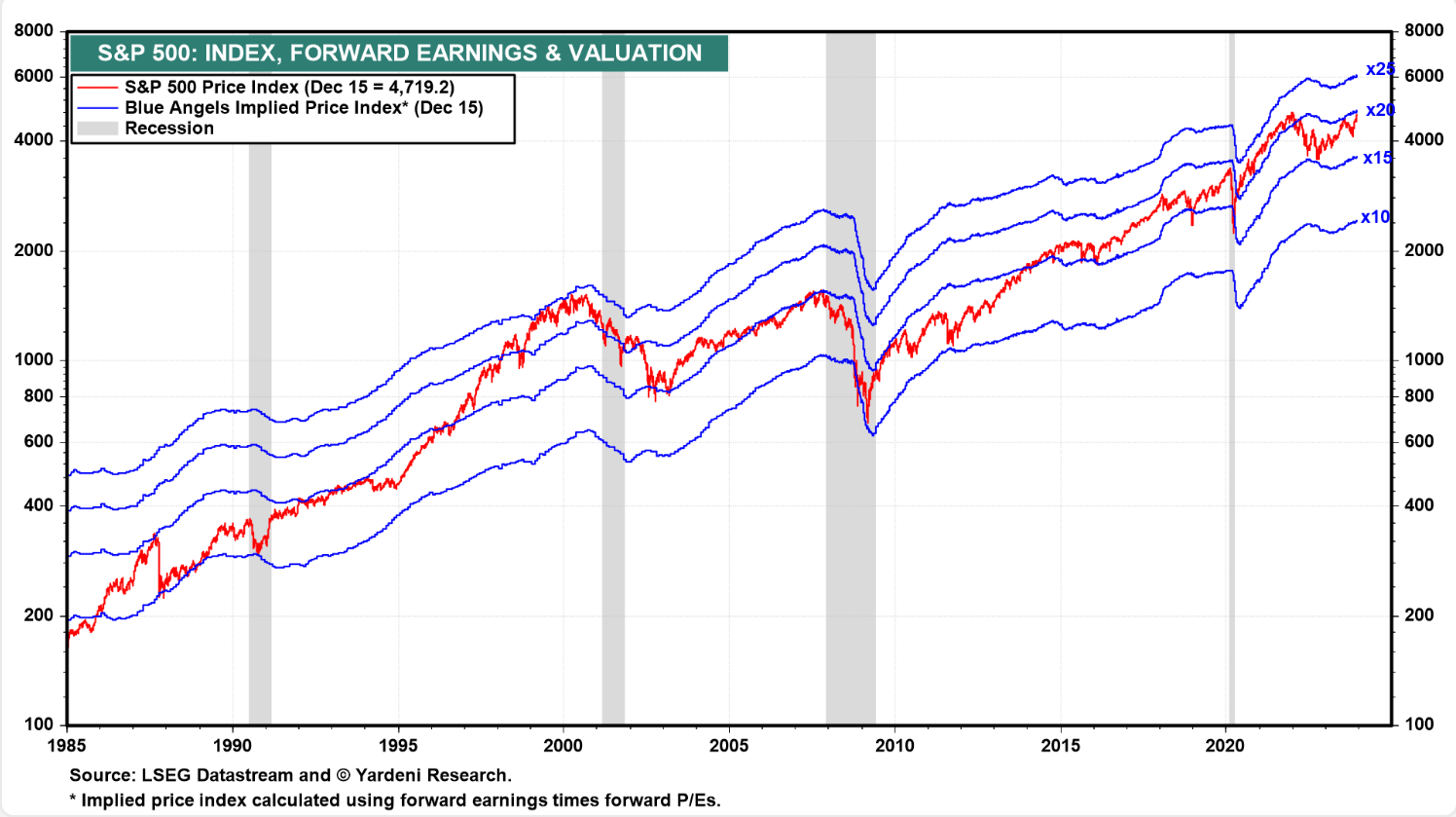

Furthermore, in September 2022, Utilities were trading at a 1x premium to the market’s valuation multiple at ~17x (Figure 5). However, by September 2023, Utilities’ relative valuation had fallen to a 2x discount, as the market’s valuation rebounded while the Utility Sector’s valuation contracted.

Figure 5 – S&P 500 Index Fwd P/E (yardeni.com)

With normalizing absolute and relative valuations, the Utility Sector looks like an attractive place to allocate capital, so I raised my rating on the Utilities Select Sector SPDR ETF (XLU) to a buy. While I did not capture the absolute low, my bullish rating on the XLU ETF has been correct, as the XLU ETF has delivered 8.5% total returns since.

Looking forward, I continue to believe Utilities are an attractive place to allocate capital as the sector continues to trade at a valuation discount to the market.

However, DNP Was Not A Buy Due To Valuations

While I was bullish on the Utility sector in late September, I did not raise the DNP fund to a buy. My main concern with the DNP fund has to do with the valuation of its shares relative to its portfolio of assets.

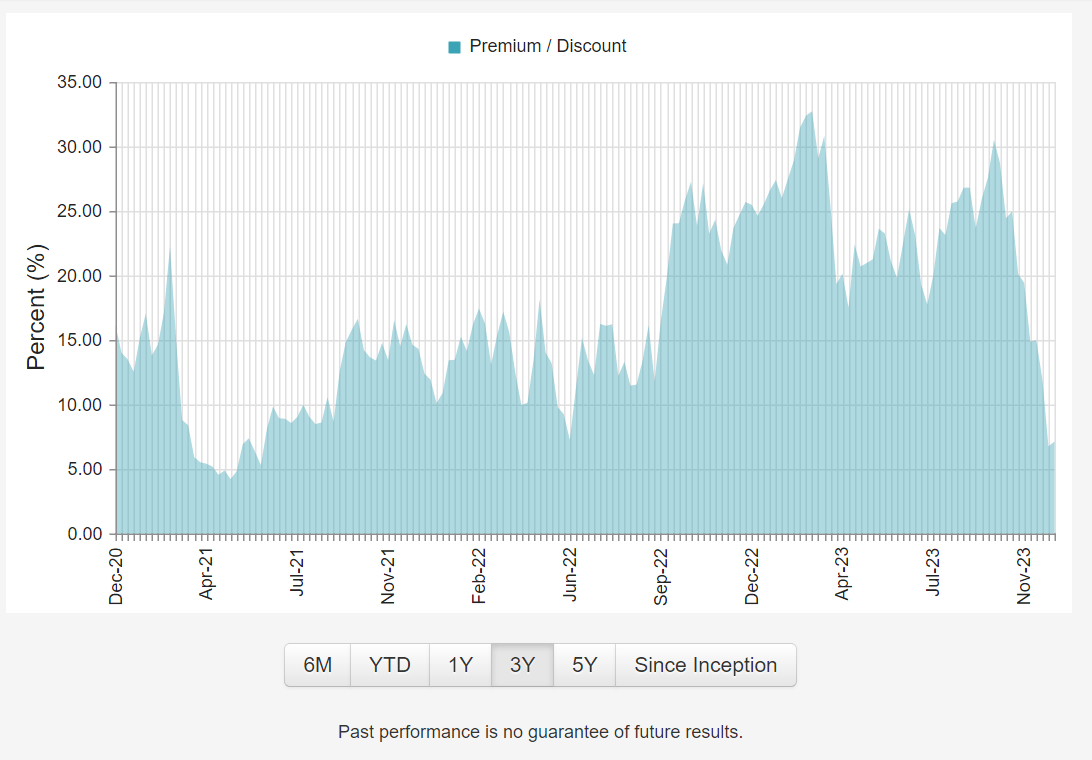

Recall from my article last year, the DNP fund was an income investor favourite and investors had pushed the DNP’s valuation to a rich 17% premium to NAV. As the DNP fund continued to pay more than it earned (approximately 30% of DNP’s fiscal 2023 distribution was funded from return of capital) and utility stocks declined, DNP’s premium valuation actually expanded in the past year to a high of 30% (Figure 6).

Figure 6 – DNP trades at a rich premium to NAV (cefconnect.com)

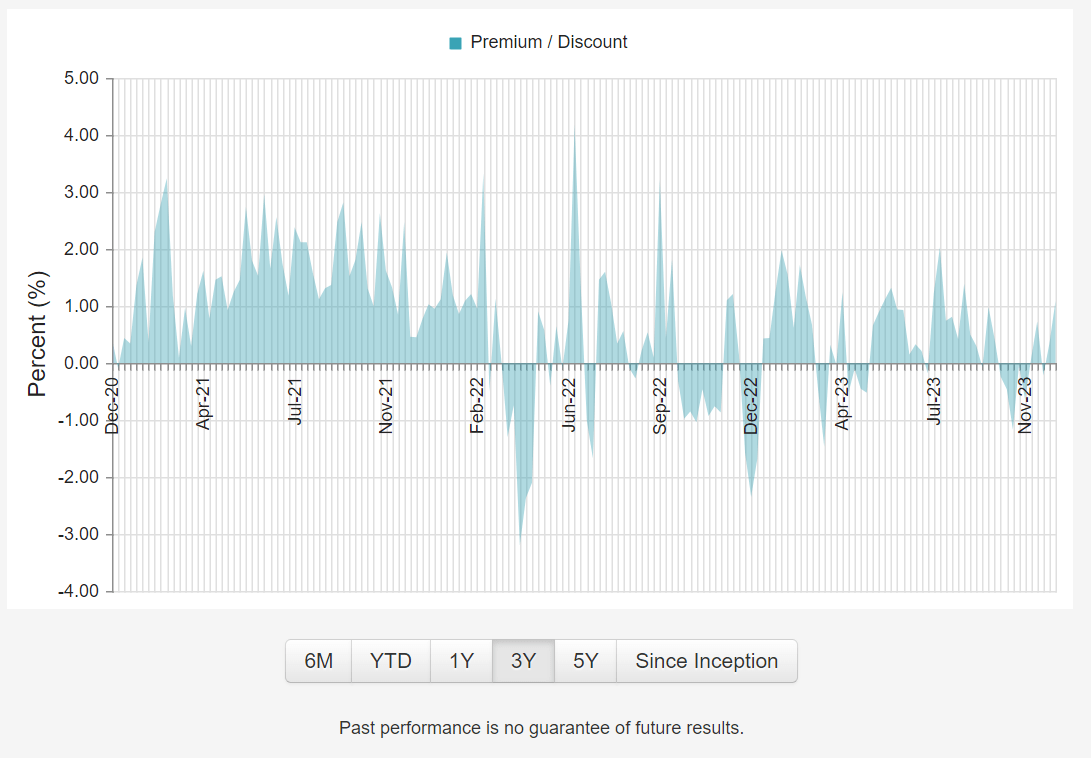

Since the DNP fund simply owned a basket of publicly traded utility and infrastructure stocks and bonds, there was no reason why its portfolio should be trading at such a rich valuation premium when peer utility CEFs like the Reaves Utility Income Fund (UTG) can be bought near its NAV (Figure 7).

Figure 7 – While UTG trades in line with NAV (cefconnect.com)

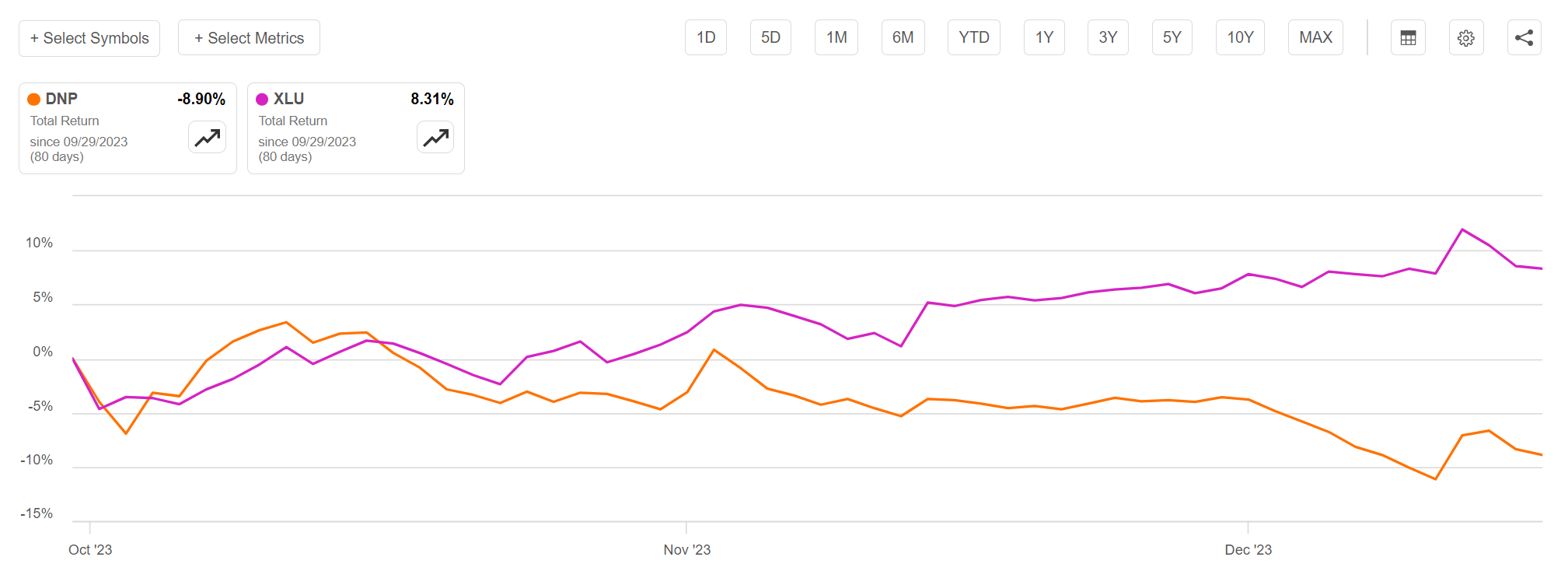

Therefore, I chose not to upgrade the DNP fund when I upgraded the Utility Sector as a whole. Evidently, that was the correct decision, as the XLU ETF has returned 8% since my upgrade while the DNP fund has lost 9% (Figure 8).

Figure 8 – DNP has lost 9% while XLU has rallied 8% since September (Seeking Alpha)

Looking forward, although DNP’s premium to NAV has collapsed in the past few weeks to just 7%, it continues to trade at a premium against its underlying assets. Therefore, I believe caution is still warranted.

DNP Vulnerable To Market Corrections

Furthermore, if we look at Figures 4 and 5, although Utility Sector valuations remain attractive relative to the market, market valuations at 20x Fwd P/E are at the high end of the historical range. If the equity markets are correct, utility stocks that are part of DNP’s portfolio are unlikely to escape unscathed.

Conclusion

Valuations do matter. Although I am bullish on Utility stocks based on normalized absolute and relative valuations, I believe caution is still warranted with the DNP fund as it continues to trade at a modest premium to its NAV. I maintain my hold rating on DNP.

Q2 2024 Earnings Call Transcript")