Phynart Studio/E+ via Getty Images

Investment Thesis

In recent months, Quipt Home Medical (NASDAQ:QIPT) has continued its impressive journey of growth and strategic expansion. The company has remained focused on its mission of becoming a leading provider in the home medical equipment sector, leveraging both organic and inorganic growth strategies. This commitment is evident in its latest operational advancements and financial results, which suggest a strong trajectory moving into 2024. With the stock currently trading at a significant discount compared to its peers, we reiterate our BUY rating and see a substantial upside potential. Since our last update, QIPT’s share price has shown volatility, reflecting broader market trends and the company’s ongoing growth initiatives. Despite some fluctuations, the underlying strength of the company’s business model and its strategic acquisitions supply a solid foundation for future growth. We continue to see ~100% upside from today’s price levels.

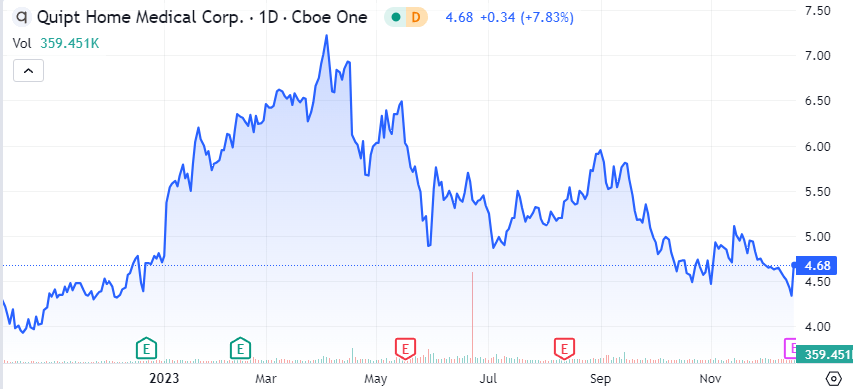

QIPT price action since previous article (Seeking Alpha)

Company Overview

QIPT continues to solidify its position in the home medical equipment (HME) market. Its product and service offerings, including sleep apnea treatment, oxygen concentrators, and mobility equipment, remain integral to its growth. The company’s expansion into new states and its growing patient base have advance established QIPT as a significant player in this sector. See our previous articles for more a more comprehensive overview of the company’s business.

Recent Performance and Developments

QIPT reported strong financial performance in 3QFY’23, with revenue growing by 64.3% year-over-year, and adjusted EBITDA increasing by 80.3%. This growth is attributed to a combination of organic initiatives and strategic acquisitions. The company announced its largest ever acquisition earlier in the year adding $60 million in revenue followed by more recent acquisitions in the states of Louisiana, Mississippi, and Texas has added significant density to its existing operations, contributing an estimated $9 million in annualized revenue. Given the overall these for this business is highly predicated on consolidating the very fragmented HME market, we see these developments as great progress.

Market Overview and Competitive Landscape

QIPT operates in the dynamic and expanding market of home medical equipment (HME) and services. This sector has seen significant growth due to various factors, including an aging population, technological advancements, and a shift towards in-home healthcare solutions. Understanding the market dynamics and QIPT’s position relative to its key competitors is crucial in assessing its potential and strategic direction.

Market Dynamics

-

Aging Population: The United States, appreciate many other developed countries, is experiencing a demographic shift towards an older population. This trend is increasing the demand for home-based healthcare services and equipment, as older adults generally have a higher need for medical care, particularly in managing chronic conditions.

-

Healthcare Cost Optimization: There is a growing emphasis on cost-effective healthcare delivery. Home healthcare is often less expensive, more convenient, and just as effective as care provided in a hospital or skilled nursing facility. This cost dynamic is pushing more healthcare providers and patients towards home medical solutions.

-

Technological Advancements: The HME market is benefiting from technological advancements, such as telemedicine, remote patient monitoring, and advanced medical devices, which improve the quality and effectiveness of home-based care.

-

Policy and Reimbursement Landscape: Regulatory policies and reimbursement rates for home medical equipment from Medicare, Medicaid, and private insurers significantly influence the market. Recent increases in CMS reimbursement rates have been favorable for the industry.

Key Competitors

QIPT faces competition from several key players in the HME market. Some of its notable competitors include:

-

AdaptHealth Corp. (AHCO): A major player in the HME market, AdaptHealth offers a range of medical products and services, specializing in sleep and respiratory therapies. It has a substantial footprint across the U.S. and has been actively growing through acquisitions.

-

Lincare Holdings: A subsidiary of Linde, Lincare is one of the largest providers of oxygen, respiratory, and other home healthcare equipment and services in the U.S. Its extensive network and broad range of services make it a formidable competitor in the market.

-

Apria: Known for its comprehensive range of home respiratory therapy, sleep apnea treatment, and negative pressure wound therapy, Apria is another significant competitor that has established a strong presence in the U.S. market.

-

Rotech Healthcare (ROTK): Rotech offers a full range of home medical equipment and related services, with a focus on respiratory care. It has a nationwide presence and is known for its patient-centric approach.

-

Other Regional and Local Providers: The market also includes numerous regional and local players, contributing to a fragmented and competitive landscape. These smaller companies often contend on the basis of localized service and specialized offerings.

QIPT’s Competitive Position

In this competitive environment, the company distinguishes itself through a focused acquisition strategy, expanding its geographic footprint, and diversifying its product offerings. The company’s recent acquisitions and organic growth strategies have strengthened its market position, enabling it to contend effectively with larger players. QIPT’s commitment to technological integration, such as e-prescribing and automated resupply, also positions it well to capitalize on market trends and improve its competitive edge.

Potential Growth Catalysts

QIPT’s journey through 2023 has unveiled several potential catalysts that could propel its growth in the upcoming years. These catalysts highlight the company’s strategic approach to expanding its market share and enhancing shareholder value.

-

Strategic Acquisitions: QIPT’s aggressive acquisition strategy, particularly the transformative purchase of Great Elm Healthcare and the recent expansion into Louisiana, Mississippi, and Texas, has significantly increased its operational footprint. These acquisitions not only add to the company’s revenue but also supply opportunities for cross-selling and upselling in new markets. The integration of these new assets is expected to contribute substantially to the company’s top-line growth and operational efficiencies.

-

Organic Growth and Operational Efficiencies: The company has demonstrated a strong capacity for organic growth, underpinned by its expanded sales force and investments in technology. The adoption of e-prescribing platforms, as highlighted by the DMEscripts investment, is set to streamline patient setup and resupply processes, enhancing patient satisfaction and adherence. QIPT’s focus on operational efficiencies, as evidenced by improved bad debt expense management and payroll optimization, also positions it for sustainable growth.

-

Robust M&A Pipeline: QIPT’s management has indicated a robust pipeline for future acquisitions, focusing on geographic expansion and density in existing markets. With its strengthened balance sheet and improved free cash flow guidance, the company is well-equipped to seek these opportunities. The acquisitions are not just about expanding the company’s footprint; they are strategic moves to enter markets with high potential and to leverage existing operational strengths.

-

Improved Free Cash Flow Guidance: The upward revision of free cash flow guidance to 6-8% of revenue reflects QIPT’s improving operational efficiency and financial health. This increased free cash flow is crucial for fueling the company’s growth initiatives, including advance M&A activities and organic expansion efforts.

-

Market Positioning and Partnerships: QIPT’s strategic partnerships, such as the national insurance contract with United Health, position it favorably in the market. These partnerships are not only a testament to the company’s credibility but also pave the way for accelerated patient onboarding and expanded market achieve.

-

Industry Tailwinds: The growing demand for in-home healthcare solutions, driven by an aging population and the need for cost-effective healthcare delivery, continues to serve as a fundamental growth driver for QIPT. The company’s diverse product portfolio and expanded service areas align well with these market trends.

-

Technological Advancements: Investment in technology, such as e-prescribing systems, positions QIPT at the forefront of innovation in the home medical equipment sector. These technological advancements are expected to improve operational efficiency, better customer experience, and maintain revenue growth through better service delivery and patient management.

-

Strong Management Team: The leadership of CEO Greg Crawford and his team has been pivotal in steering the company through its growth phases. Their expertise and strategic vision are crucial in realizing the potential of these growth catalysts.

Valuation

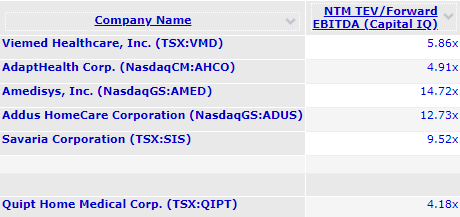

QIPT continues to be undervalued compared to peers. While peers such as Viemed (VMD) and AdaptHealth have seen their multiples reject over the past year, QIPT has actually sustained its valuation which is a testament to its resilience in this tough market. Having said that, we believe QIPT should be valued (conservatively) at 6-7x given its recent track record. we maintain a target share price of $8

QIPT Comps (Capital IQ)

Risks

Risks include integration challenges with recent acquisitions, competition in the HME market, and potential changes in CMS reimbursement rates. However, QIPT’s management has demonstrated adeptness in navigating these challenges.

Conclusion

QIPT is well-positioned for sustained growth, backed by a solid strategy, a robust balance sheet, and an effective management team. With the stock currently undervalued, we see significant potential for upside and propose investors consider a long position. We see ~100% upside from today’s price levels

Q2 2024 Earnings Call Transcript")