MF3d

Written by Nick Ackerman, co-produced by Stanford Chemist.

First Trust Energy Infrastructure Fund (NYSE:FIF) has seen its discount narrow materially since our last update. This is driven by the fact that the fund is expected to merge into an exchange-traded fund structure, which would, along with its sister funds, create a larger fund. The real win here was that it would also mean no more material discounts going forward, and investors holding the fund could see an upside from here.

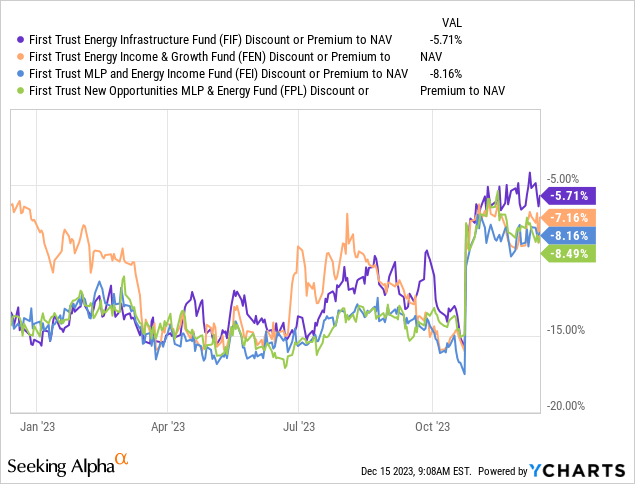

Given the discount closing materially since our last update, the fund’s performance has been strong. It has also helped that risk-free Treasury Rates have been receding more recently, causing an uptick in infrastructure funds with heavy weightings to utilities.

FIF Performance Since Prior Update (Seeking Alpha)

FIF Basics

- 1-Year Z-score: 2.27

- Discount: -5.71%

- Distribution Yield: 7.27%

- Expense Ratio: 1.48%

- Leverage: 20.41%

- Managed Assets: $344.5 million

- Structure: Perpetual

The objective of FIF is “to seek a high level of total return with an emphasis on current distributions paid to shareholders.” They intend to accomplish this through “investing primarily in securities of companies engaged in the energy infrastructure sector. These companies principally include publicly traded master limited partnerships and limited liability companies taxed as partnerships, MLP affiliates, YieldCos, pipeline companies, utilities, and other infrastructure-related companies that derive at least 50% of their revenues from operating, or providing services in maintain of, infrastructure assets such as pipelines, power generation industries.”

The Merger And Opportunity Potential

The merger isn’t FIF alone, but also its heavier energy peers, First Trust Energy Income and Growth Fund (FEN), First Trust MLP and Energy Income Fund Common (FEI), and First Trust New Opps MLP & Energy Fund (FPL). That merger into the new structure for a fund called First Trust Energy Income Partners boost Income ETF with the ticker (“EIPI”) is expected to happen in the second quarter of 2024.

Due to FIF still trading at a discount, there is still some opportunity here as the new structure means no discount will exist – at least not a meaningful one, as ETFs have a creation and redemption mechanism to keep the prices very near the NAV per share. Additionally, FIF is in a unique situation where it was already a regulated investment company rather than its energy-focused sister funds, which were structured as C-corps.

This is because the NAV of those funds could take a hit due to the tax situation when selling off MLPs in their portfolio and before they transition. However, it should be noted that they also mentioned that there could be a potential final one after the merger takes place.

In connection with the proposed mergers of FEN, FEI and FPL into EIPI, each of these Target Funds may be required to recognize a decrease to its NAV prior to its merger, with another potential final adjustment to be made to the NAV of EIPI following the mergers after the receipt of year-end tax information to be provided by the master limited partnerships (“MLPs”) that had been held by such Target Funds. The amount and timing of such adjustments, if any, will depend in part on the market prices and composition of each such Target Fund’s portfolio securities.

For this reason, it could make sense why FIF is trading at the shallowest discount relative to its other sister funds.

YCharts

The press release specifically stated that it isn’t contingent upon any of the other funds getting shareholder approval. Therefore, one or more of these funds may not end up going into this new structure.

Additionally, it could be possible that none of the funds get approval from shareholders. That seems admire an unlikely scenario, but it is possible. Saba Capital Management has just over a 6% stake in FIF, around 7.5% in FEI, then in FPL around an 8.4% holding, and they have no position in FEN. It seems admire there is little doubt that those shares will be voted for approval into the new structure.

EIPI will still be actively managed, and it’ll “seek to supply a high level of total return with an emphasis on current distributions paid to shareholders.” The investment policy provided seems fairly broad in that they are “investing in energy companies.” Additionally, the fund will use a partial covered call strategy. The funds already do this as well, so that won’t be that big of a change.

Though it isn’t specified in the material I’ve seen yet, which is just the press release announcing the Board’s approval, I would make the assumption that the fund isn’t going to be employing leverage. That would mean the fund, if it was created today with all four funds approved, total assets would come to around $1.188 billion.

I’d also make the assumption that the ETF will be structured as an RIC and not a C-corp, which is the most common. That means that investors in FEN, FPL, and FEI are going to see less exposure to master limited partnerships than they currently do. FIF will as well, but to a slightly lesser degree.

FEN carries 67.3% of its net assets in MLPs as of their last semi-annual report. FPL was at 59.7%, and FEI was at 58.6%. FIF was at a 47.4% allocation, but these figures are all relatively higher because they break it down to net assets while they are leveraged funds.

FIF % of Net Assets Allocation (First Trust)

Going forward, the exposure is going to be limited with the assumption that they’ll be in an unleveraged ETF RIC structure. RICs are limited to holding 25% of their portfolio in MLPs.

Risk

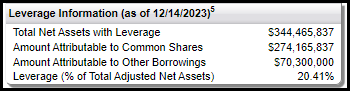

While there is an opportunity to capitalize on the discount contraction that remains over the coming 6 months or so, there are always risks. Being that the fund is still leveraged, the risk to the downside is relatively higher. It’s unclear when they would take down the leverage – or even if they scheme to run a non-leveraged ETF.

FIF Leverage Stats (First Trust)

However, the discount of around ~6% could easily be wiped away during a market downturn. For now, with the Fed looking set to cut rates rather than boost, it would suggest there is some upside potential to go if the risk-free rate falls encourage. It’s worth considering, though, that the economy slows down significantly during this period, and that would turn into a negative, especially for the fund’s energy exposure, which often relies more heavily on a strong economy.

That being said, you’d still be invested in a portfolio that is carrying most of the same exposure and could ride the rebound in the new structure or simply sell and advance the capital elsewhere to take part. It would just be that if they sell assets to deleverage before conversion, the rebound might not be as significant as the downside advance.

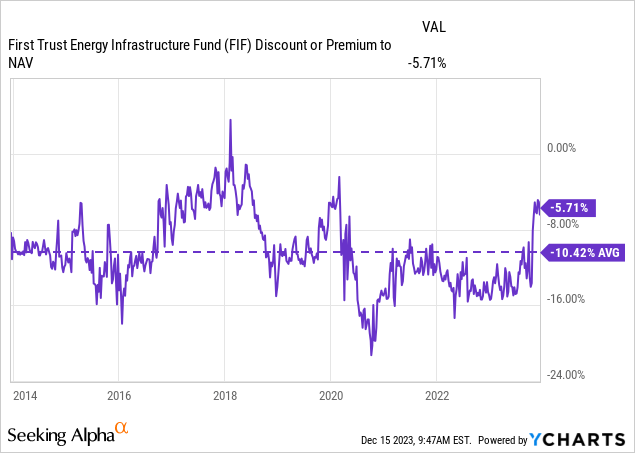

An additional consideration is if the fund’s shareholders don’t approve the conversion. That would likely see the fund’s discount widen back out to the longer-term average level. Over the last decade, that was much closer to 10% and would mean downside potential from here.

YCharts

Conclusion

The reasoning for this conversion could be speculated that First Trust is moving out of the closed-end fund business. They had announced that they were merging several of their other CEFs into abrdn funds. Stanford Chemist discussed that when he discussed FEI and the opportunity on that fund. Saba building a position in several of their funds could also have been part of the reasoning.

Overall, the fund’s discount was narrowed significantly after this announcement, but there is still some small opportunity there to attain the rest of the discount upon conversion. That being said, the merger is subject to approval and how the market cooperates in determining the actual end result going forward. Those are the main risks.

Q2 2024 Earnings Call Transcript")