RyanJLane

Investment Thesis

In this article, I’m sharing my thoughts on Atlantica Sustainable Infrastructure plc (NASDAQ:AY), a company that’s really making waves in renewable energy. We’re going to look at how they handle solar, wind, and hydropower, and what makes them stand out in places appreciate North and South America, and Europe. I’ll be talking about how they’re doing financially and why I think they’re a smart choice for investors. I address challenges, particularly in the EMEA region, while highlighting the company’s capacity to steer market volatility. Readers can expect a balanced view, blending meticulous financial scrutiny with an appreciation of Atlantica’s role in the sustainable energy transition.

Rating: Buy

Introduction

Atlantica Sustainable Infrastructure specializes in renewable energy and infrastructure globally, managing assets in solar, wind, natural gas, and hydroelectric power. They also handle electricity transmission and transportation across North America, South America, and parts of Europe. Focused on clean energy and environmental conservation, Atlantica pursues long-term projects and contracts for stable revenue and reduced market risks, aiming to balance sustainable energy transition with investor returns.

Current Financials

As I contemplate on Atlantica Sustainable Infrastructure plc’s financial performance in the third quarter of 2023, I see several reasons to uphold my buy thesis. First, their revenue and EBITDA have remained stable at $858.6 million and $627.3 million, respectively. This stability, in my view, signifies a resilient business model, particularly in the volatile energy sector. Moreover, the company has reported a 2.9% year-over-year growth in cash available for distribution, reaching $184.2 million in the first nine months of 2023. This growth, albeit modest, is a positive indicator of the company’s operational efficiency and financial health.

The geographical and sector-based breakdown of Atlantica’s financials advocate bolsters my confidence. In North America, revenue increased by 4.6% to $338.7 million, primarily due to higher production of solar assets. This boost, despite the lower production from wind assets, reflects the diversified nature of Atlantica’s portfolio, which I believe is key to mitigating risks associated with any single energy source. Similarly, in South America, there’s been a 14.5% boost in revenue, highlighting the company’s effective expansion strategy in emerging markets.

However, it’s important to admit some challenges. In Europe, the Middle East, and Africa (EMEA region), revenue and adjusted EBITDA decreased by 7.9% and 8.3%, respectively. This was primarily due to lower revenues at solar assets in Spain, influenced by market price fluctuations. Despite this, the predefined rate of return on these regulated assets provides a buffer against market volatility, an aspect that I find particularly reassuring.

Atlantica’s CEO, Santiago Seage, emphasized the company’s strategic positioning in the renewable energy market, highlighting the growing demand and uphold for renewable energy across various geographies. This, coupled with the company’s ability to blend higher costs of capital in new investments, suggests a strong market presence and adaptability. The signing of two tolling agreements for storage projects in California, offering higher returns than expected, advocate exemplifies Atlantica’s strategic prowess in capitalizing on market opportunities.

Their financing model, described by CFO Francisco Martinez-Davis, is simple and prudent, primarily consisting of plain vanilla project debt with fixed interests or hedges. The company’s approach to debt repayment and its emphasis on maintaining a balanced and sustainable capital structure is commendable. This strategic financial management, combined with their diversified, well-contracted portfolio of assets, reinforces my buy thesis.

In conclusion, while there are areas of concern, particularly in the EMEA region, the overall financial stability, strategic market positioning, and prudent financial management of Atlantica Sustainable Infrastructure plc present a compelling case for a buy rating. The company appears well-positioned to capitalize on the growing demand for renewable energy, making it an attractive investment opportunity in the sustainable energy sector.

Forward Outlook and Guidance

Reflecting on Atlantica Sustainable Infrastructure plc’s forward outlook, I’m bolstered in my buy thesis by several key points shared by the company’s leadership during their recent earnings call. CEO Santiago Seage’s commentary on the renewable energy market was particularly insightful. He noted the continued high growth in renewable energy in the US and other markets where Atlantica operates. Seage emphasized that “demand for renewable energy continues to be strong, both from utilities and corporates,” emphasizing the market demand Atlantica is going to capitalize on, which reinforces my belief in the company’s growth potential.

Seage also highlighted a critical skill needed in today’s fluctuating economic environment, where he shared:

Based on what we are seeing at this point in time, we are being able, we believe, to blend the higher cost of capital in our new investments” – Q3 Earnings Transcript

This adaptability in financial planning and project execution is a solid strength, particularly as smaller developers struggle in the current market.

Moreover, Atlantica’s recent successes, appreciate the signing of two tolling agreements for storage projects in California, imply the company’s competitive edge and ability to ensure higher-than-expected returns. Seage’s remark that “we see a constructive market in front of us” aligns with my optimistic view of Atlantica’s positioning in the renewable energy sector.

CFO Francisco Martinez-Davis advocate reinforced this positive outlook by detailing Atlantica’s prudent financing model. The majority of their financing is non-recourse, self-amortizing project debt in ring-fenced subsidiaries, which provides a stable foundation for growth. Martinez-Davis explained “our assets repay their project debt progressively” which ensures that cash available for distribution is clearly after project debt repayment. To explain advocate, Atlantica Sustainable’s project debt, currently at $4.4 billion, is projected to decrease to $2.5 billion by the end of 2028. This significant reduction would very likely reinforce the company’s financial health, which would guide to better credit ratings and lower interest costs. The boost of investor confidence is also likely which allows for greater flexibility in future investments and strategic initiatives. Additionally, the main emphasis would be on the reduction of financial risks, and therefore opening up possibilities for increased shareholder dividends, which is vital to income-focused readers.

In summary, I think that Atlantica’s management team has an optimistic perspective on the market and their strategic approach to growth and financing continually supports my buy thesis. Atlantica is positioned well due to its ability to steer the challenges of a dynamic market, combined with a solid track record of securing profitable projects and maintaining a stable financial structure. These initiatives from the company give me confidence in its potential for sustained success in the renewable energy sector.

An Attractive Dividend As Short Interest Lowers

Atlantica Sustainable Infrastructure’s reaffirmed quarterly dividend of $0.445 per share, showcasing a substantial forward yield of 8.38%, supporting my buy rating. This yield is considerably higher by 118% compared to its sector median, which speaks volumes about the company’s ability to produce and distribute wealth to its shareholders. It reflects confidence in the company’s steady cash flow and financial prudence. For me, this is a clear signal of Atlantica’s commitment to delivering shareholder value and its stability within the volatile renewable energy sector. Such a reliable dividend profile not only attracts income-seeking investors but also underlines the company’s solid financial health.

Following, Atlantica Sustainable’s decrease in short interest since October, to me, signals a decrease of skepticism amongst investors, which is a pinpoint in my buy thesis. The rate has dropped from 6.2% in October to 2.45% as of December 15th. As short interest drops, it often suggests that the market is shifting towards a more positive outlook on the company’s future performance. My overall thesis appears cautiously optimistic as institutional investors decrease their short stakes, thereby solidifying my confidence in Atlantica as a sound investment with a forward-moving trajectory.

Why the Focus on North American Renewables is Key

The strategic focus of Atlantica Sustainable Infrastructure plc on North American renewable energy and storage projects is a well-calculated advance that aligns with the region’s burgeoning renewable energy market and the favorable policy environment created by the Inflation Reduction Act (IRA). This legislation is a game-changer for the renewable energy sector in North America, particularly in the United States, as it catalyzes substantial public and private investment in renewable energy technologies. The IRA, along with the Infrastructure Investment and Jobs Act (IIJA), has led to the announcement of $227 billion in investments, signifying a monumental commitment to the transition towards cleaner energy and decarbonization.

The increasing demand for electricity, coupled with the declining costs of solar power modules and the government’s initiatives to boost renewable shares in the total energy mix, are driving the growth of the solar power market in the United States. The installed solar capacity in North America had reached 104.4 GW as of 2021, with a considerable growth rate compared to previous years. This trend is expected to continue, fueled by the IRA’s emphasis on renewable energy and storage, making Atlantica’s strategic focus on North America particularly opportune.

Moreover, the IRA’s significant tax credits and incentives for renewable energy investments improve the financial viability of renewable energy projects, making them more attractive for investment. Atlantica’s focus on energy storage aligns with the IRA’s emphasis on this technology, which is crucial for managing the intermittency of renewable energy sources appreciate solar and wind. The increased financial and regulatory uphold for storage technologies under the IRA makes investments in this area more appealing.

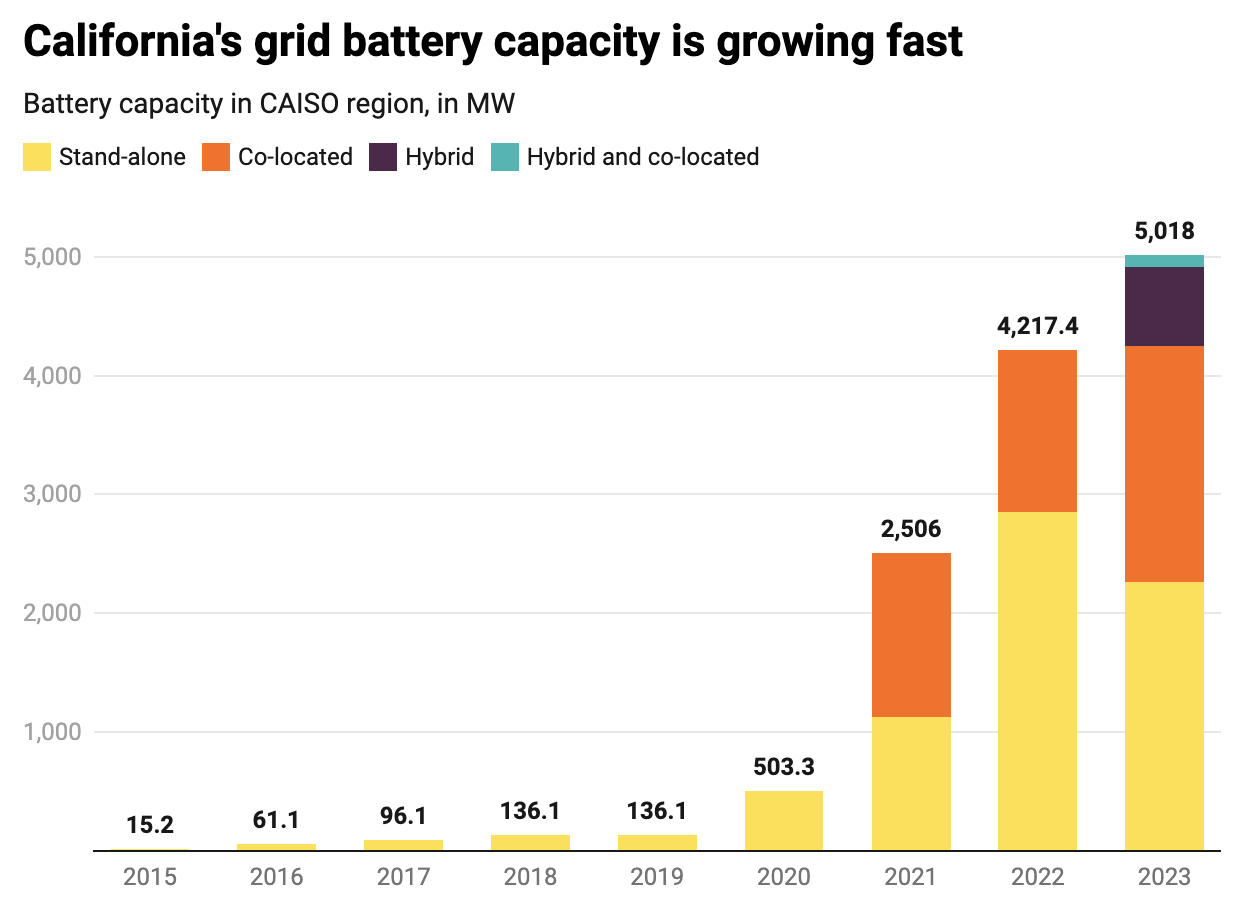

Additionally, the growing market for energy storage, crucial for grid stability in regions with high renewable penetration appreciate California, reinforces the strategic relevance of Atlantica’s focus in North America. Below is a graph that I thought illustrated this perfectly, from Canary Media.

California’s Grid Battery Capacity (Canary Media)

The IRA’s uphold for a stronger domestic clean energy industry and more robust supply chains for solar, wind, storage, and green hydrogen advocate enhances the attractiveness of this market for Atlantica. Ultimately, all compelling attributes for a long position in Atlantica.

Risks

While I preserve a positive stance on Atlantica Sustainable, it’s vital to admit the possible risks in their business model. First, the renewable energy market, despite its growth, is susceptible to regulatory and political changes. Fluctuations in government policies or subsidies could impact Atlantica’s operations and profitability. Additionally, their reliance on long-term contracts, though providing stability, could limit flexibility in rapidly changing markets.

Another risk involves the execution of new projects. As Atlantica expands, particularly in diverse geographies, it faces challenges in maintaining project efficiency and managing increased operational complexity. Also, while their financing strategy is prudent, the reliance on project debt brings its own risks, including interest rate fluctuations and refinancing challenges.

Despite these concerns, Atlantica’s diversified asset base and focus on stable, regulated revenue streams offer some mitigation. Their careful approach to project selection and financing, coupled with a strategic emphasis on low-cost, clean energy solutions, positions them well to steer these risks. I see these challenges not as deterrents but as aspects requiring vigilant management as Atlantica continues to grow in the dynamic renewable energy market.

Valuation

In my investment analysis of Atlantica Sustainable Infrastructure, the Seeking Alpha Valuation Metrics furnish compelling evidence to uphold my buy thesis. The standout figure is the dividend yield of 8.38%, soaring higher than the sector median of 3.85%. This substantial yield, graded A+ by Seeking Alpha, indicates a robust potential for income generation, which is particularly attractive in the current low-interest-rate environment. Now some investors worry that dividend is not sustainable. But, as I look into the cash dividend payout ratio calculated by Seeking Alpha, we see that Atlantica is at 56.71%, which is slightly under the sector median of 58.33%. Therefore, I am optimistic that the yield will hold at its current level; a much-needed statistic for the income-focused investors reading.

Conversely, the P/E Non-GAAP (FWD) at 104.45, receiving an F, suggests a premium valuation compared to the sector median of 17.46. While this could raise concerns about overvaluation, in my view, it also reflects market confidence in Atlantica’s future earnings potential, warranting a deeper look into its growth strategies and market positioning.

The Price/Sales (FWD) ratio stands at 2.25 with a sector median of 2.04, graded a C by Seeking Alpha. This close alignment with the sector median reassures me that Atlantica’s stock is not excessively priced relative to sales, maintaining its competitiveness within the sector.

Also, the Price/Book (FWD) ratio is a modest 1.74 against a slightly higher sector median of 1.72, earning a C+ grade. This indicates that the company’s stock is trading at a fair value relative to its book value, which is reassuring when considering asset-based valuation.

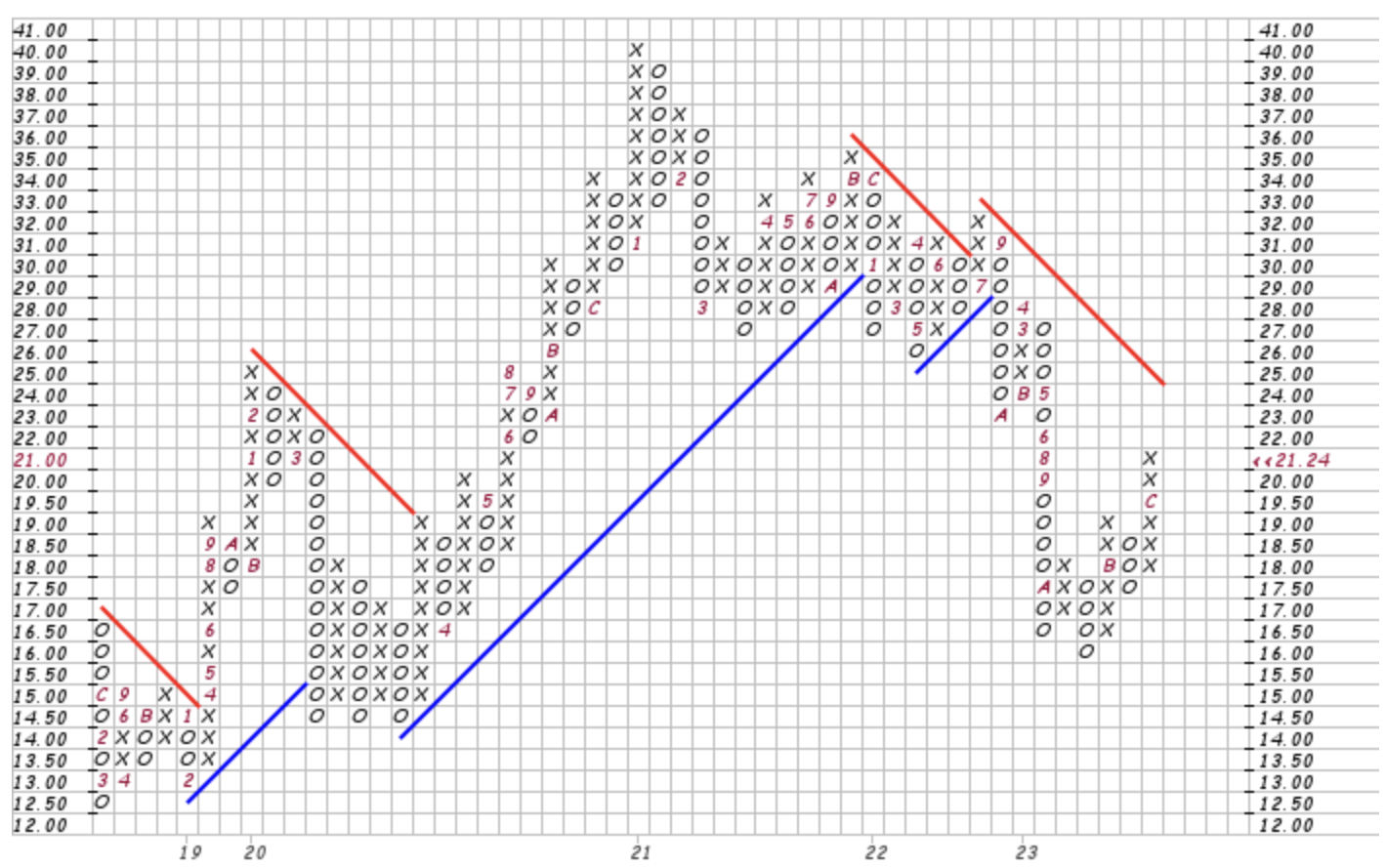

Lastly, let’s view my favorite technical chart, the point and figure with a traditional three box reversal. If we direct our attention to the middle right side of the graph, we notice the large boost in the stock recently. Just appreciate Newton’s law, an object in motion will stay in motion unless an external force is acted upon it, which applies to investing, too. We call this momentum and right now this is in our favor. In a technical view, I am subject to believe that with such momentum we could see the stock return to the median range it was once fluctuating at. I anticipate that the stock price will surge somewhere in the range of 27.00 to 32.00 (where we could see some profit-taking as well). All in all, with this technical chart, I think Atlantica is poised for potential upside and a solid return for investors.

AY Point & Figure (Stock Charts)

Taking these metrics into account, Atlantica’s stock presents an intriguing proposition. The high dividend yield suggests a strong return on investment potential, and although the P/E ratio is high, it may be justified by Atlantica’s strategic investments in the growing renewable sector. The P/S and P/B ratios advocate affirm that the stock is reasonably valued. These grades and numbers aren’t just abstract figures; they contemplate a company solidly positioned for those looking for income and principal gains in the sustainable energy space.

Conclusion

I believe overall, Atlantica Sustainable carves out a strong case for investment. I’ve researched the company’s strategic mastery over a diversified portfolio, its financial resilience in a tumultuous sector, and its future-facing growth prospects. The key takeaway is that this is a company not merely riding the wave of renewable energy but shaping it. Atlantica stands out with its ability to steer risk while championing sustainable practices and shareholder returns. My rating is quite clear: Atlantica represents a thoughtful investment for those looking to align with the future of energy without sacrificing the financial soundness of today.

Q2 2024 Earnings Call Transcript")