valentinrussanov/E+ via Getty Images

Investment action

I recommended a hold rating for Clarivate Plc (NYSE:CLVT) when I wrote about it the last time, as I do not see any visible catalyst for the stock. The first thing that CLVT needs to do is show the market that organic growth can turn positive. Based on my current outlook and analysis of CLVT, I propose a buy rating. Now that CLVT has turned organic growth positive and has visible tailwinds ahead that could drive organic growth higher, I believe the stock is attractive at this valuation.

Review

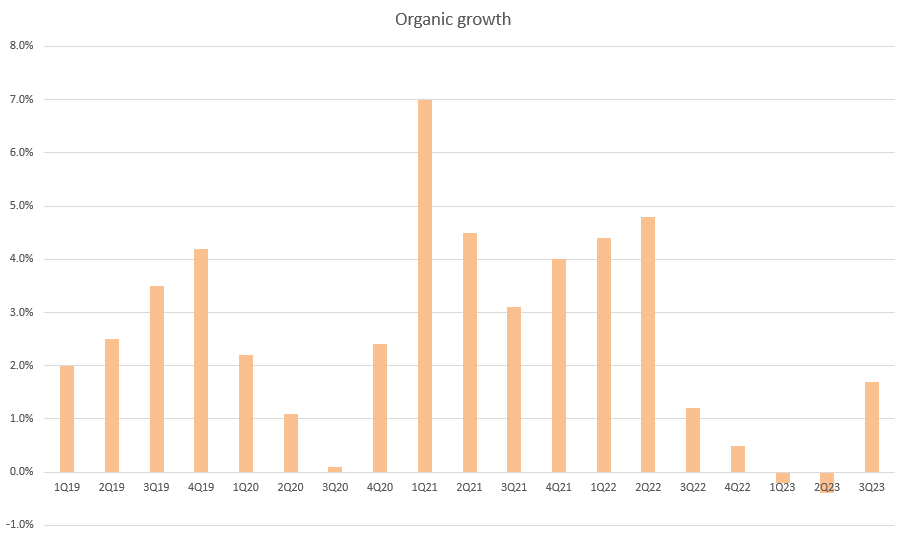

To give a brief recap, CLVT reported 3Q23 revenue of $647.2 million, a 1.8% y/y growth on a reported basis. On an organic basis, revenue growth improved by 210bps from -0.4% growth in 2Q23 to 1.7% in 3Q23. The organic growth was driven by subscription revenue growth of 1.3%, re-occurring revenue growth of 0.5%, and transactional revenue growth of 3.5%. By segment, Academia & Government [A&G] grew 3.4% organically, Life Sciences & Healthcare [LSH] grew 1.7%, but Intellectual Property [IP] grew only 0.9%. Not only did CLVT report positive organic growth, but they also demonstrated EBITDA margins by 80 bps y/y to 43.5%, beating consensus estimates of 41.9%. Consequently, CLVT reported EPS of $0.21, which beat the consensus assess of $0.18.

As I expected, the catalyst for the stock to work is organic growth turning positive, which CLVT did in 3Q23. The share price reacted immediately, jumping from the low of $6 to the current price of $8.80. Importantly, the organic revenue recovery was driven by improving underlying trends in A&G and LSH. On a consolidated basis, I believe the CLVT outlook is now a lot clearer given that A&G is 50% of total revenue and its growth is less correlated to macroeconomic cycles due to its dependence on government budgets. This can be seen from the past few quarters’ performance, where organic growth continued to speed up despite the macro weakness. In fact, 3Q23 had the strongest growth in five quarters. The content aggregation transactional sales and three large library workflow software wins with major universities in 3Q23 should keep A&G’s growth momentum going in the near future. From a stock sentiment perspective, the A&G segment should advance better sentiment as 4Q should see another quarter of organic growth acceleration given that 4Q is the largest transactional quarter of the year. Management has noted that early indications of how the business is trending, particularly within the US, are positive. Suppose A&G accelerates its organic growth to 4% in FY24, at 50% of total revenue. This effectively locks in ~2% of organic growth for FY24 on a consolidated basis.

LSH, accounting for approximately 17% of total revenue, is expected to encounter ongoing organic growth in the upcoming quarters as well. Considering the difficult biotech landscape and the lack of hard real-world data in the quarter, the 1.7% organic growth in 3Q23 is quite remarkable. Now that CLVT has signed more contracts, I foresee significantly stronger normalized growth. In 3Q23, CLVT inked a strategic partnership with a prominent US biotech firm and inked another deal with a top 20 pharmaceutical company in the world.

Our Consulting business delivered 7% growth in the quarter and we secured a large engagement with a global top 20 pharma to extend our partnership in epidemiology analytics supporting market access and clinical trials. We also signed a strategic agreement with a leading US biotech to speed up commercial and market strategies for their direct drug candidate. 3Q23 earning call

In terms of growth cadence, growth in the near term (4Q23) is likely to remain depressed given the strong 4Q22 performance and the change in business strategy. Unlike in the past, CLVT is now aiming to sell its data directly to clients instead of going through third parties. Revenues from transactions and subscriptions linked to those transactions are expected to refuse in the near future as a result of this change. There are no arguments that this will impact near-term growth, but I see this as a transitional phase that will better the long-term organic growth profile of the segment. With this shift, CLVT will be able to create a subscription-based portfolio that is both more sustainable and more visible (revenue and cash flow). Also, I believe that LSH’s organic revenue growth in 2024 will be supported by the FDA’s improved drug approval rate this year, which bodes well for pharma commercialization.

Finally, for IP, which is ~33% of the total revenue, this segment has more correlation to the macroeconomic cycle. Much of the headwind that the segment is facing is due to weak macro putting pressure on budgets. This cyclical factor is likely to recover only when the macrocycle turns. Thankfully, it appears that the bottom is near, as the US Fed is signaling to cut rates next year. Another headwind in the segment, which I believe is non-structural, is the US Actors strike that has continued to impact Trademark and Patent transactional explore business lines. This strike not only delayed the release of new films; it also delayed the start of a contract.

We also saw a delay in the start date of a new contract with the United States Patent & Trade Office, which was awarded to Clarivate earlier this year. This enhanced contract was delayed by the client, and we recently received word the contract will start in early first quarter next year. 3Q23 earnings call

Now that the strike is over, the segment should start to recover gradually as the contract starts and new films that were previously delayed are now released into the world. In terms of growth cadence, 4Q23 is likely to remain weak as the strike only ended in November, but FY24 should see organic growth.

Valuation

Author’s work

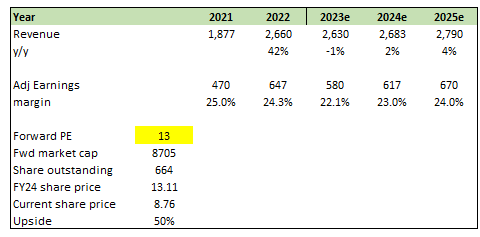

As CLVT showed that it can turn organic growth positive, I now expect CLVT to continue improving its organic growth outlook due to the reasons I mentioned above. For modeling assumptions, I expect CLVT to gradually better its consolidated organic growth to a previous high of 4% over the next 2 years, and FY23 to follow management’s guidance. For adj earnings, I annualized 9M23 adj earnings to derive $580 million. Post-FY23, with organic growth accelerating, margins should better accordingly to the historical level of mid-20s. A main upside drive is that I expect CLVT to trade at 13x forward PE, a ~3x enhance from the current 10x forward PE. I believe this assumption is not aggressive, as 13x forward PE is -1 standard deviation from the CLVT historical average of 24x. With organic growth turning positive, this should dismiss the worry that investors (appreciate myself) had previously. The acceleration in organic growth justifies CLVT trading at a higher multiple than today.

Author’s work

Risk and final thoughts

For the A&G segment, while it is not entirely correlated to the macrocycle, it is heavily exposed to the government budget, which makes it hard to forecast the future trajectory. The government could cut the budget at any point in the cycle, which is an inherent risk that could throw my organic growth forecast off track.

Overall, I am upgrading my rating to a buy as CLVT showed that it can produce positive organic growth. Notably, the 3Q23 results showcased encouraging organic growth across segments, especially in A&G and LSH. Looking ahead, I expect organic growth to recover back to historical levels given the new contracts signed, change in sales strategy, and potential easing of macro headwinds.

Q2 2024 Earnings Call Transcript")