jpgfactory

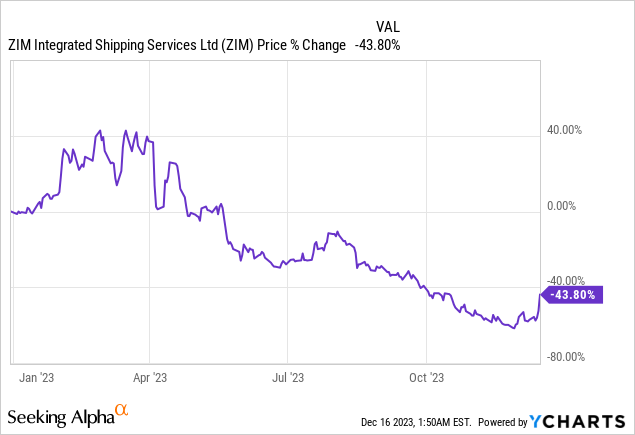

Although ZIM Integrated Shipping Services (NYSE:ZIM) lowered its EBITDA forecast in 2023 due to challenges in the container shipping industry, recent turmoil in the Red Sea has fundamentally changed the short to medium outlook for the shipping company, in my opinion. A number of shipping companies including Maersk and Hapag-Lloyd have said that they are going to pause container shipments in the Red Sea due to Houthi attacks on container ships.

The deteriorating security situation in the Red Sea could benefit container freight rates which already edged up 10% since the end of November. I do not expect the dividend to make a comeback in the short term, but I believe that at the current valuation level and given the firm’s high short interest ratio, ZIM has short squeeze potential!

Previous rating

I upgraded ZIM Integrated Shipping Services to hold in September due to the company maintaining a strong balance sheet and liquidity position. While the pricing situation in the container market threw up some challenges at the time, I believe freight rates may continue to enhance as some shipping companies paused their container traffic in response to attacks on container ship traffic in the Red Sea.

Increased risk for container shipping companies could result in higher freight rates

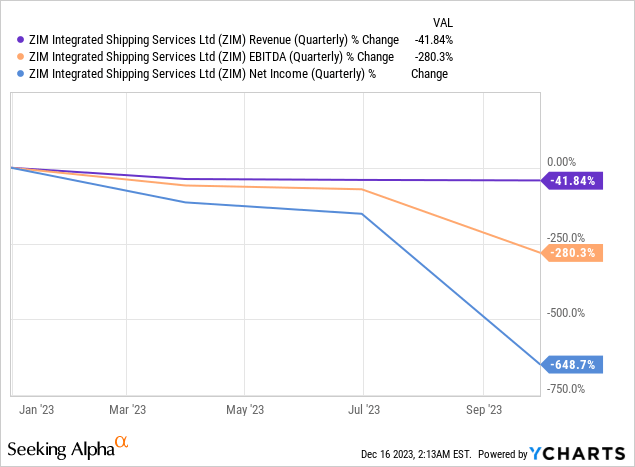

In the last year, the main obstacle to profitability for container shipping companies admire ZIM Integrated Shipping Services was rapidly dropping container freight rates which made the transport of goods from one port to the other an increasingly unattractive business. The sharp reject in freight rates in the last year caused a collapse in the company’s revenues, EBITDA, and net income.

The drop in freight rates was the single biggest reason for ZIM Integrated Shipping Services’ disappointing third-quarter results, the elimination of the dividend and it was behind the company’s downgrade in its EBITDA guidance for FY 2023. Given the deteriorating pricing environment in the container market, ZIM Integrated Shipping Services downgraded its full-year EBITDA forecast from $1.2-1.6B in Q2’23 to $900-1,100M in Q3’23.

However, the pricing environment may be just about to change as increasing risk for container shipping companies operating in the Arabian and Red Seas, and the announcements of some companies to pause shipments through the Bab al-Mandab Strait, could be catalysts for higher container freight prices. Following a series of attacks on container ships in the Red Sea, conducted by Houthi rebels from Yemen, Maersk announced that it would halt its voyages in this region. Germany-based Hapag-Lloyd also said that it would temporarily suspend its Red Sea route, also in light of recent attacks.

These developments are starting to have a positive impact on container prices as a whole since the voluntary suspension of container traffic in the Red Sea is reducing the availability of container ships and increasing transit time.

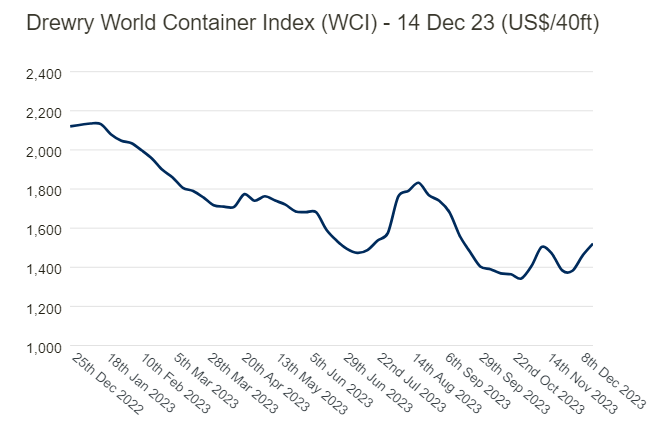

The market has already seen an uptick in container shipping prices, as measured by the Drewry World Container Index, which depicts the prices for the shipment of a 40-foot container. As of December 14, 2023, it costs companies $1,521 to ship one 40-foot container which shows a price enhance of approximately 4% in the last week. Since the end of November, which is when ZIM Integrated Shipping Services warned of increased threats related to container shipping in the Arabian and Red Seas, prices have gone up approximately 10%.

Drewry

Short squeeze potential

For a short squeeze to happen, two conditions must be met: 1) Shares of the company for which a short squeeze may be expected must be heavily shorted, and 2) There must be an unforeseen catalyst event that wasn’t previously considered by analysts and investors.

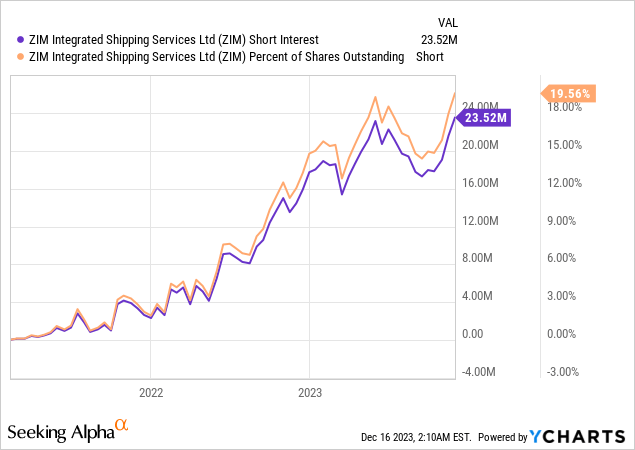

As to the first point, ZIM Integrated Shipping Services had a short interest ratio of almost 20% as 23.5M of the firm’s shares are currently shorted. The short interest trend also points upwards, indicating that investors’ attitudes towards the shipping company have consistently eroded in the last two years.

Second, the escalating number of container ship attacks in the Red Sea has the potential to limit the availability of container shipping capacity and also enhance the risk for Red Sea voyages, implying that prices for container shipments could rise drastically in the short term, especially if the international community fails to put an end to such attacks. Since investors have previously not considered a potential upsurge in container prices, I believe ZIM Integrated Shipping Services has considerable short squeeze potential.

ZIM Integrated Shipping Services’ valuation

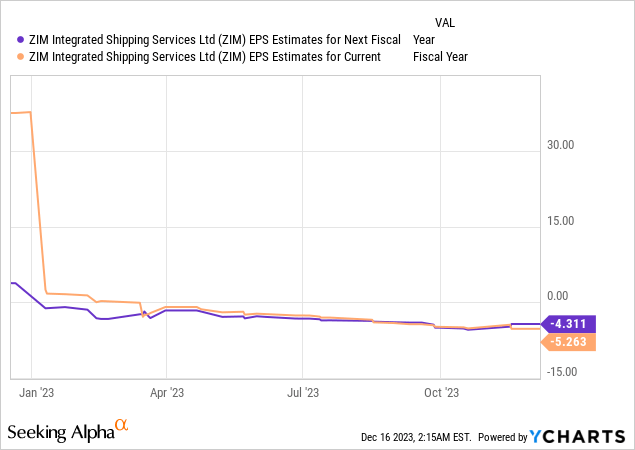

Previously, ZIM Integrated Shipping Services’ valuation was impacted by expectations of a recession. Now, the short- and medium-term outlook for ZIM Integrated Shipping Services may change considerably as freight rates have already reacted to the increased risk of Red Sea voyages. Analysts still expect negative earnings in FY 2023 and FY 2024, but estimates may proceed to the upside if the short-term pricing situation advocate improves.

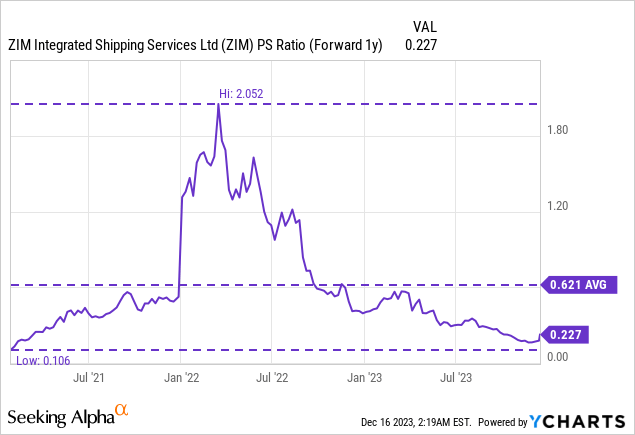

With no profits expected for this year and next year, a P/E ratio cannot be applied to value ZIM Integrated Shipping Services. However, based off of revenues, the shipping company appears to be an anti-cyclical bargain: shares are priced at just 0.23X revenues and are therefore 63% cheaper than the 3-year average P/S ratio indicates.

Risks with ZIM Integrated Shipping Services

ZIM Integrated Shipping Services as an Israel-based company is especially at risk from targeted attacks on container ships. Terror attacks and longer transit times are therefore very real risks to the shipping firm. However, in my opinion, these risk factors will be reflected in a higher fear premium (higher container freight rates) which may actually better ZIM Integrated Shipping Services’ short-term earnings picture. A deteriorating risk situation in the Arabian and Red Seas would therefore both a risk and an opportunity (to capture higher shipping rates) for ZIM Integrated Shipping Services.

Final thoughts

Freight prices have seen positive momentum in the last two weeks, which is when Houthi-led attacks on container ships in the Red Sea escalated. Considering that freight prices have moved upwards by 10% since the end of November and that ZIM Integrated Shipping Services remains a heavily shorted company (every fifth share has been shorted), I believe the shipping company has considerable short squeeze potential. Additionally, I expect the short-term earnings picture to better and EPS estimates reset to the upside, reflecting improved container freight pricing. Given the circumstances surrounding Red Sea-borne container traffic, I believe ZIM Integrated Shipping Services is a promising, yet speculative buy heading into 2024!

Q2 2024 Earnings Call Transcript")