Joe Hendrickson/iStock via Getty Images

Shares of Whirlpool (NYSE:WHR) have been a poor performer even as they modestly bounced off their lows. Last year, I urged investors to buy shares of WHR, but they have returned a disappointing -13% since then. The company’s margin performance has been weak, which has made it more difficult to pay down debt. I do view the dividend as ensure, and a shift in policy from the Federal Reserve may be exactly what Whirlpool needs to get through this difficult time.

Seeking Alpha

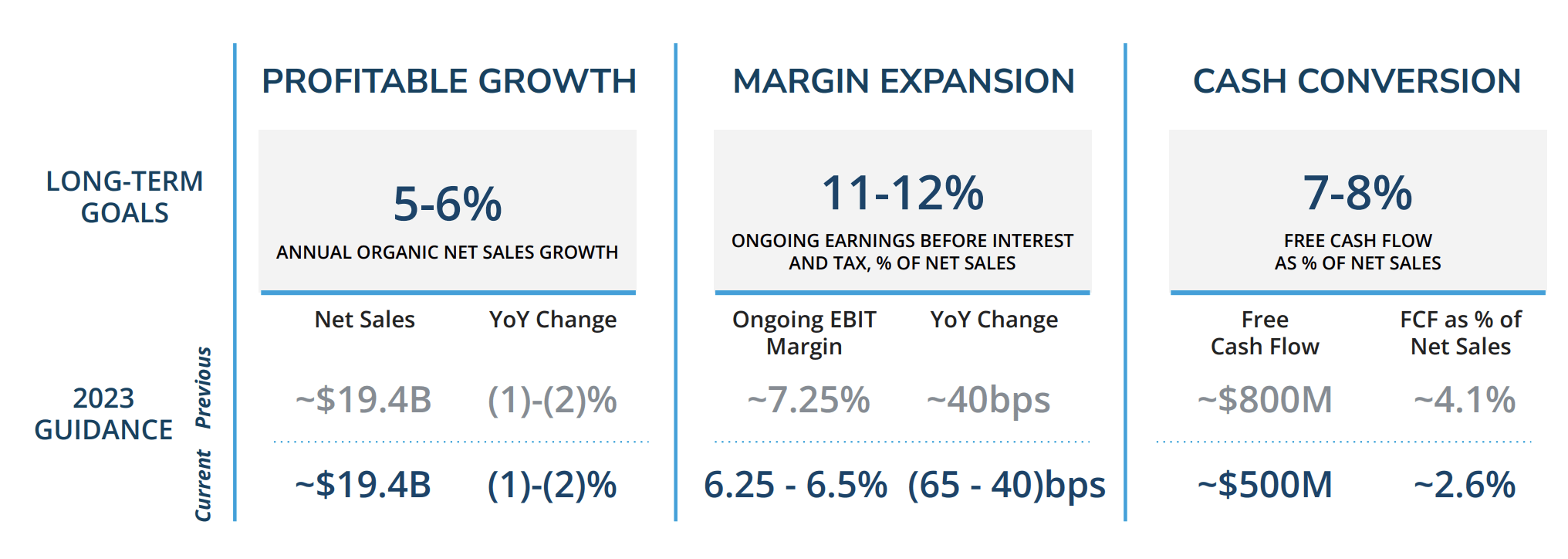

In the company’s third quarter, it earned $5.45 in adjusted EPS, which beat consensus. This was outweighed by reduced guidance with expectations for $16 in ongoing EPS and $500 million in free cash flow. As you can see below, the company kept its revenue calculate unchanged, but it meaningfully cut margins, which also led to lower free cash flow. About $100 million of the lower free cash flow is due to worsening working capital with inventory now set to build slightly whereas $200 million comes from weaker margins. With this guidance, Whirlpool needs significant ongoing improvement to confront its long-term targets.

Whirlpool

It should also be noted that the company is enjoying tax benefits from its European restructuring, which means it will likely have a negative tax rate this year. That helped it preserve its EPS guidance despite weaker EBIT margins. This is another reason the market has reacted so negatively to guidance and looked past the quarterly beat.

These pressures that drove the reduced guidance were evident in recent results. In the third quarter, revenue rose 3% to $4.9 billion, aided by M&A with a 1% reject in organic sales. EBIT margin of 6.5% was up from 5.5% last year. Over the past year, the company has seen over 6% relief on inflation, outweighing nearly 4% of pricing headwinds. The InSinkErator acquisition has driven increased revenue and earnings growth.

Unfortunately, while margins have improved from last year when supply chain bottlenecks caused significant problems for the company, Whirlpool has lost momentum here. Margins fell by 80bp sequentially with a 1.5% reject in pricing/mix. Falling prices have overwhelmed the benefits of lower input prices. Management has blamed this on normalization in the promotional environment as unclogged supply chains have helped bring more appliances to the market.

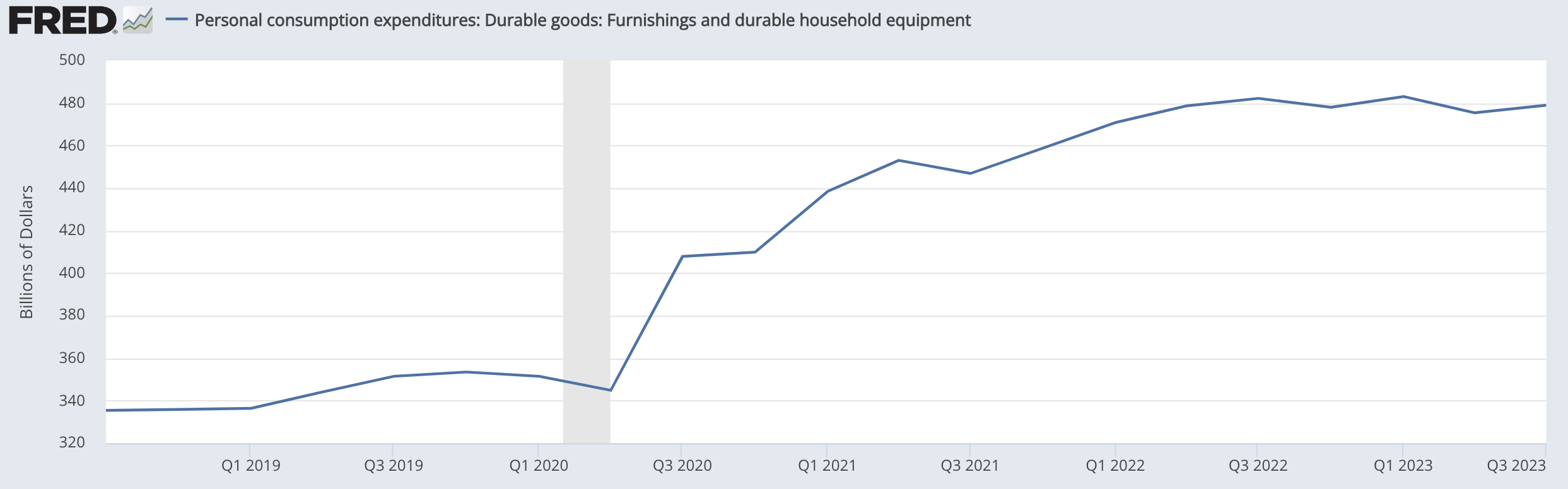

Frankly, there is more than normalization occurring. According to the latest CPI report, household appliance prices are down 3.5% from last year. Laundry equipment, obviously a major driver of Whirlpool’s business, is down 12%. That is a significant loss of pricing power, which is why margins have been squeezed. Fortunately, the company has been winning share, gaining about 1% in North America, but this is at the cost of margins. As you can, spending on household goods and appliances has stagnated for essentially eighteen months.

St. Louis Federal Reserve

This stagnation is apparent in Whirlpool’s North American business, which accounts for over 60% of revenue and over 80% of profits, where its InSinkErator acquisition was the driver of growth.

Overseas, it is also a mixed bag. Latin America is the bright spot with sales rising 10% to $0.9 billion on a constant currency basis as Brazil and Mexico rebound. Operating margins expanded 100bp, driving 35% growth in pre-tax earnings to $54 million. Conversely, Asia is the weak point with sales down 8% on a constant currency basis with pre-tax earnings of just $5 million as construction markets there have been soft, weakening consumer sentiment. Subsequent to quarter end, Whirlpool announced it is selling a 24% stake in its India unit to help pay down debt.

Finally, in Europe, sales were down 2% excluding Russia to $0.9 billion, and the business ran at breakeven. Europe has been a problematic market for Whirlpool for years with difficulty building scale and maintaining margins, which is why it has chosen to divest the unit, making current results less relevant for investors. The merging of its European business with Acrelik remains on track for an April close. As part of this agreement, it maintains a 25% stake in the entity, which it can monetize, should there be buyers. With its 40-year licensing of the Whirlpool brand to the entity, it expects about $750 million of present value in future cash payments. That is below the $1.6+ billion I hoped the business could fetch. Still, removing these operations and receiving the licensing payments should supply a $250 million boost to free cash flow starting next year.

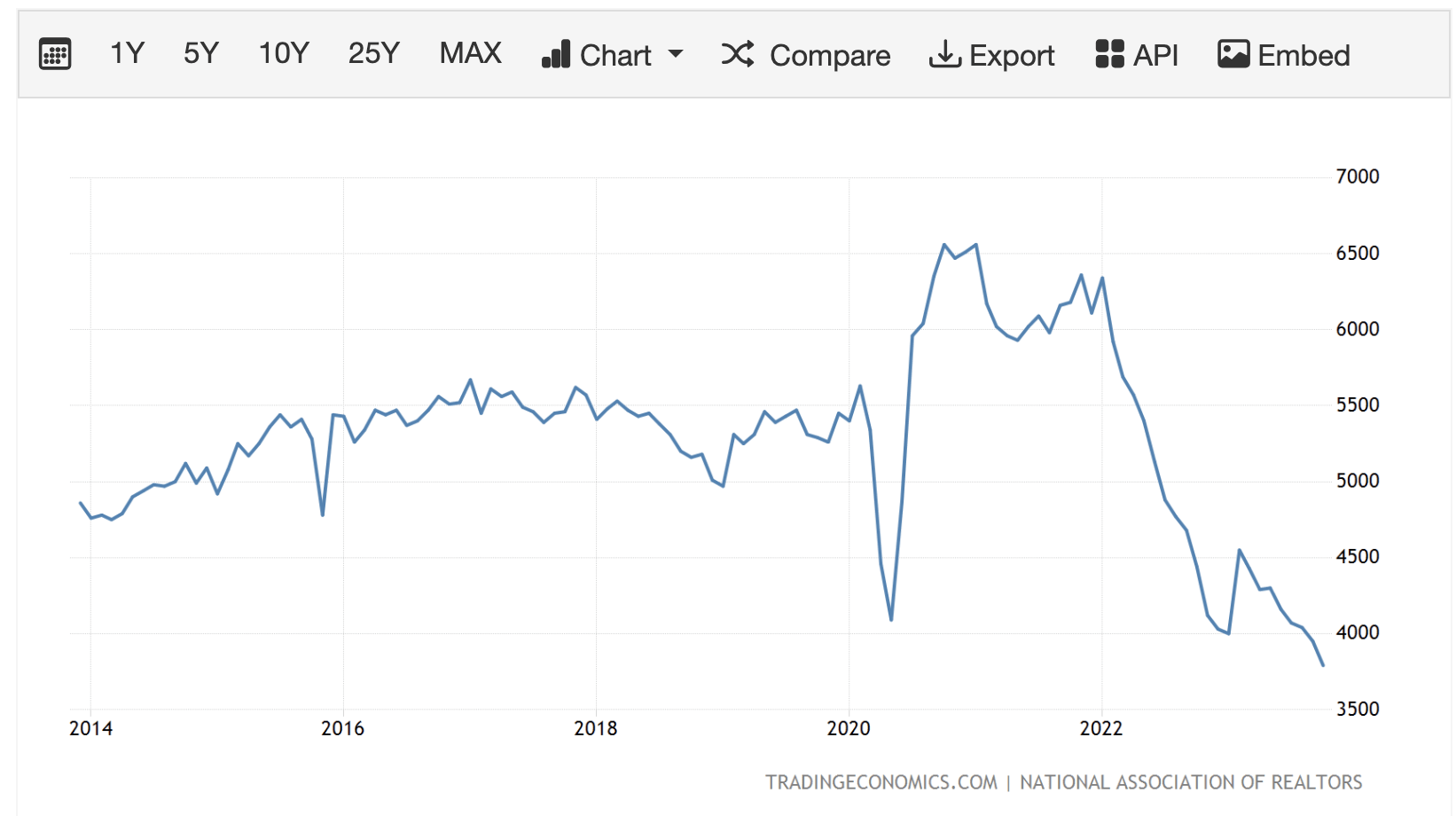

The simplification of its business and exit from a long-term underperforming business should enable management to focus more on its core US franchise. Here, I am increasingly optimistic about a turn in the business this year. 60% of appliance demand right now is replacement relative to the long-run 53-54%. I am not sure if it is that replacement is so strong or that new purchases are particularly soft. Purchasing or upgrading appliances is an activity correlated to moving or buying a new house. While I expected a reject in housing sales this year, the magnitude has been jarring with existing home sales at 10+ year low.

Trading Economics

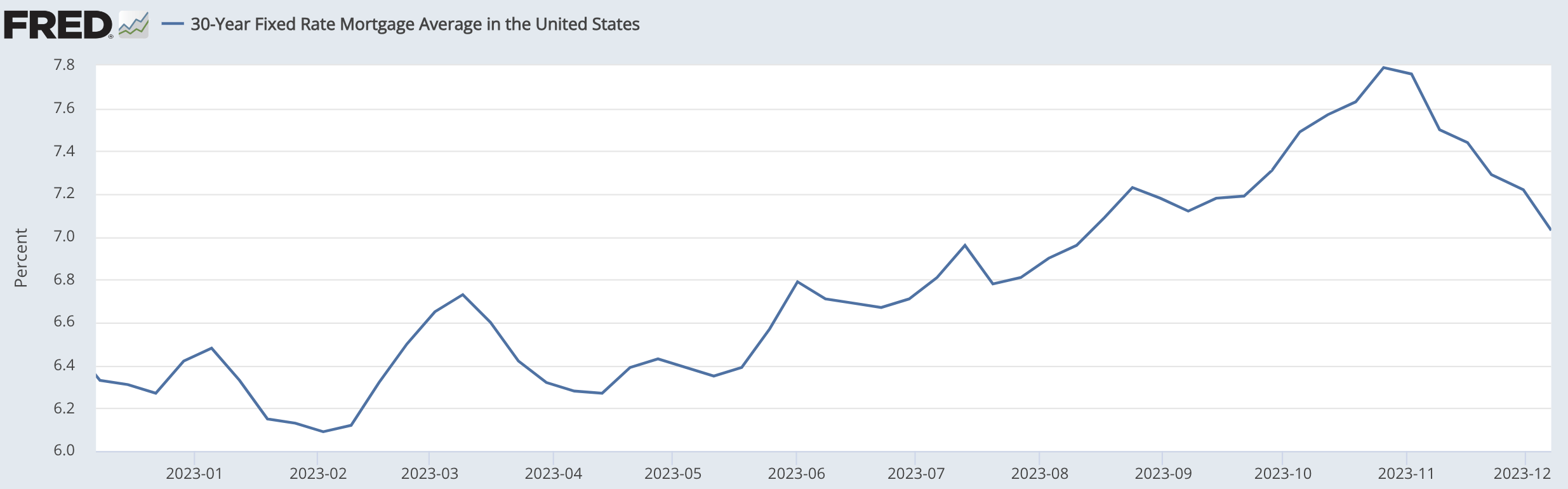

Of course, higher rates have made it more difficult for buyers to purchase a home. They also have locked existing owners with low-rate mortgages into their houses as the cost of moving would be so high. While I do not expect to see housing transactions recover even to pre-COVID levels, given this factor, with rates coming down, we should see improvement in 2024. Indeed, the Fed is now projecting three rate cuts next year. Mortgages have fallen 100bp from their highs, and if these cuts materialize, we should see rates fall encourage, making it easier for more housing transactions to occur.

St. Louis Federal Reserve

A rebound in housing activity should preserve recovery in demand for appliances, allowing the manufacturers to become less promotional and recapture their lost margins while also working inventories back down. With shares so beaten down, the company does not even need a full recovery in activity to put a floor under the stock.

This timing of lower rates will also benefit its balance sheet. After its InSinkErator acquisition, Whirlpool is carrying more debt, $7.6 billion in fact, and $1.3 billion matures over the next year The company needs to reduce net debt by about $1.7 billion to confront its targets. I originally hoped the proceeds from the European sale could cover this, but given the structure of the deal, which will not happen quickly.

Because of its higher debt load and elevated rates, interest expense has more than doubled from $40 million a year ago to $95 million last quarter. Now, management will pay down $500 million in debt in Q4, but this is coming largely from its $1.1 billion of cash rather than true de-levering. The challenge is that the company’s dividend costs $400 million. With $500 million in free cash flow, its debt reduction capacity is just $100 million this year.

Now with Europe being sold, we should see an acceleration in its free cash flow. The company’s $1 billion term loan matures in April, and another $1.5 billion is due in October 2025. WHR is unlikely to produce sufficient cash flow after its dividend to pay these off entirely, but as rates come down, it now has an opportunity to extend its maturities at lower rates than previously thought, which can give it more time to pay down debt.

I do expect the dividend to remain ensure as it is covered by cash flow, but buybacks are multiple years year. Investors are being paid to foresee, and with just a $6 billion market capitalization, shares have an 8% free cash flow yield.

In 2024, with US housing market activity rebounding, I expect low-single digit sales growth (~3%) and some margin recovery, getting back toward 7%, aided by continued softness in commodity prices. Combined with its $250 million in cash flow benefits from its European transaction, free cash flow can run about $800 million in this environment, providing 2x dividend coverage and enabling a more meaningful pace of debt reduction. Given its disappointing track record, I expect its multiple to be constrained, but even at a 10% free cash flow yield, shares could rally back to $145-150, providing a 30+% total return opportunity. The Fed easing rates and helping the housing market may be just what is needed to make Whirlpool a 2024 recovery stock after a weak 2023.

Q2 2024 Earnings Call Transcript")