At my age, I’m still 25 to 30 years away from retirement. Therefore, readers need to grasp that at this stage of life, I’m primarily concerned with growing the value of my portfolio. My decisions might not be as conservative as others. For those closer to retirement, preservation of capital might be a bigger concern than growth.

As of this writing, MercadoLibre (MELI 0.17%), Axon Enterprise (AXON 1.13%), United Rentals (URI 0.41%), Crocs (CROX -0.69%), and Tanger (SKT -1.26%) make up 40% of my portfolio’s value. Many advisors would probably tell me to reduce my exposure to these five stocks and to diversify more.

However, I don’t strategize to make any changes to my top five holdings. While the professionals have their reasons for suggesting greater diversification, I intend to apply principles from investing greats Peter Lynch and Warren Buffett and keep everything with my top holdings the same.

Here’s what Lynch and Buffett have to say

In his 1988 letter to Berkshire Hathaway shareholders, Buffett wrote: “We are just the opposite of those who hurry to sell and book profits when companies perform well but who tenaciously hang on to businesses that disappoint. Peter Lynch aptly likens such behavior to cutting the flowers and watering the weeds.”

In other words, Buffett agrees with Lynch on a specific investing approach. They hold on to shares when those companies perform well, and they sell shares when those businesses disappoint. Most portfolio-building approaches do the opposite; they book their gains by selling winners while doubling down on losers.

For perspective, the five stocks I’m highlighting in this article make up just 18% of my portfolio’s cost basis — a very mundane average allocation of about 3.5% each. I’ve invested more money into other stocks in my portfolio. The difference is that all five of these stocks have gone up significantly since I first purchased shares, whereas many others have dropped.

In short, my portfolio concentration at the top is a natural outcome of what’s worked and what hasn’t. This wasn’t a deliberate choice up front.

Why I keep holding

If these five businesses started underperforming at some point, then perhaps I would trim these positions. But as far as I’m concerned, all five are flowers that are currently still blooming, and I want to keep them firmly planted in my garden. Here’s a brief investment thesis for each of these five companies that explains why I’m still holding.

1. MercadoLibre

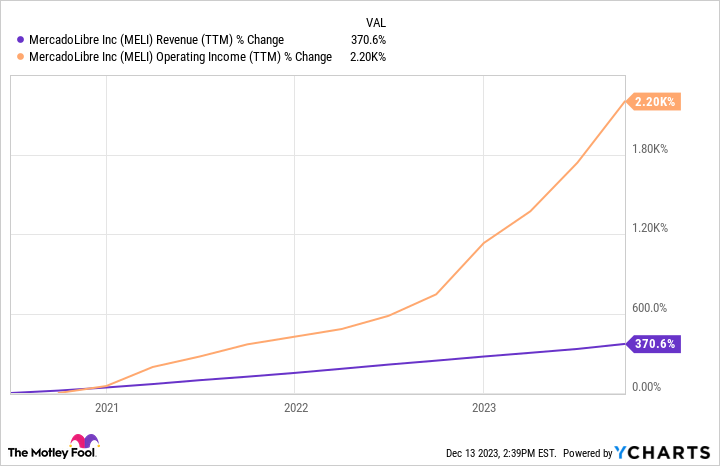

MercadoLibre operates in Latin American markets, such as Brazil, Argentina, and Colombia, and has generated $10.2 billion in net revenue through the first three quarters of 2023. That’s up 10 times from the same period five years ago, reflecting just how high-growth its opportunity is.

The company serves ongoing needs in Latin America, such as digital payments and e-commerce, and this should keep growth going in the future. As the chart shows, the company’s operating profit is skyrocketing, which is a good thing for long-term shareholders.

MELI Revenue (TTM) data by YCharts

2. Axon Enterprise

Axon Enterprise offers Tasers, body cameras, and time-saving software to law enforcement agencies around the country. As one might visualize, this isn’t an easy business to break into generally. Companies need reputable track records to safeguard contracts, and deals with law enforcement agencies tend to be long-lasting.

With its track record, Axon has built a large, recurring revenue stream with agencies around the country, and its backlog of orders continues to grow. Moreover, the company’s track record is allowing it to break into new opportunities, such as with federal agencies and in international markets, which can continue to drive long-term shareholder returns.

3. United Rentals

United Rentals is one of the best-performing stocks over the past decade, with shares up more than 650% in value. And yet the largest equipment-rental company in the U.S. is still relatively unknown to investors. This highlights how boring the market finds this space.

In this case, boring is good. United Rentals is a very profitable company with a long record of strong free cash flow generation. And because investors tend to ignore the space, the company can often buy out competitors at cheap valuations. This allows it to quietly grow while gobbling up market share, leading to higher profits down the road.

It’s a simple yet effective path to creating shareholder value and it’s why I keep holding my shares of United Rentals.

4. Crocs

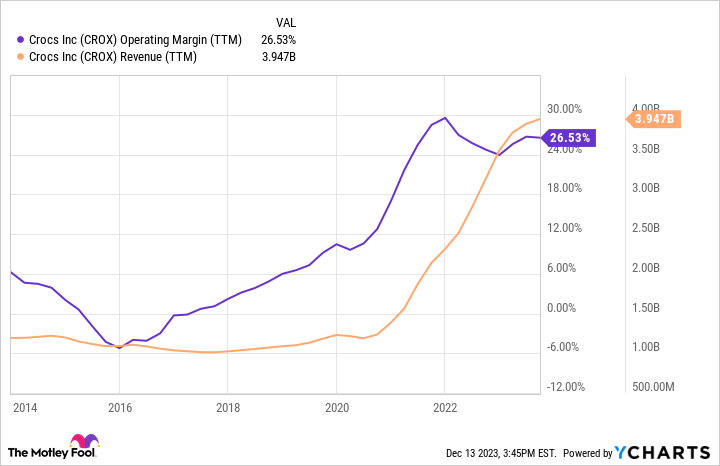

Crocs expects to produce nearly $4 billion in revenue this year, which is pretty huge for a shoe stock. Due to its already large size, I don’t necessarily expect the company to take the world by storm in coming years. That said, Crocs has a fantastic operating margin of around 26%, as the chart shows, which makes it attractive to me as an investment.

With strong profitability, Crocs can do simple things that boost shareholder value, such as repurchasing shares and reducing its long-term debt. And trading at less than 10 times its trailing earnings, the stock is cheap enough to be a winner with even modest growth — I wouldn’t expect its valuation to fall much from here.

CROX Operating Margin (TTM) data by YCharts

5. Tanger

Tanger is a real estate investment trust (REIT) that owns 39 outlet malls and open-air shopping centers. Many of its tenants are in the discretionary sector, which admittedly is a little risky. That said, the company has long enjoyed occupancy rates at around 98%, which also happened to be its occupancy rate as of the third quarter of 2023.

This company has a chance to meaningfully boost cash flow in coming years. Almost 60% of its current annual base rate rents are due for renewal between now and the end of 2026. Raising rents would boost cash flow and potentially boost the money available for dividends.

As a REIT, Tanger is obligated to pay a percentage of its profits out as dividends. It already provides a high yield at about 4%, but that could boost in a big way. The company would have to raise its dividend by almost 50% to fully recover to where it was before the pandemic — business is back, so this seems doable. Moreover, if it can steadily boost rents in coming years, then that adds extra cash flow to boost dividends even advance.

Holding on for the ride

Over time, my bad investments have dropped in value, whereas the five stocks mentioned here have jumped. By leaving things alone, this has caused my portfolio to naturally concentrate around my winners. And since I still see good things ahead for my top five, I don’t strategize to trim or sell any of these positions in the coming year.

This might make my returns a tad more volatile in 2024 — fewer stocks can have larger impacts on overall returns. However, I believe the bigger risk would be to sell shares of winning companies when they still have so much ahead of them.

Q2 2024 Earnings Call Transcript")