CUHRIG

Elevator Pitch

I award a Buy investment rating to Yancoal Australia Ltd (OTCPK:YACAF) [YAL:AU] [3668:HK].

Yancoal Australia’s valuations are poised for a re-rating, which warrants a Buy rating. Its China market’s prospects are good, and the company can leverage on its robust financial position to boost shareholder value.

Readers should take note that Yancoal Australia’s shares are traded on the OTC (Over-The-Counter) market, the Australian Securities Exchange, and the Hong Kong Stock Exchange. The three-month average daily trading values for the company’s OTC, Australia-listed, and Hong Kong-listed shares were $0.04 million, $5 million, $4 million, respectively as per S&P Capital IQ data. Investors can trade in Yancoal Australia’s relatively more liquid Hong Kong and Australian shares using US brokers with access to overseas markets admire Interactive Brokers.

Company Overview

In its 1H 2023 interim report, Yancoal Australia describes itself as a company that “owns, operates or has joint-venture interests in nine (of which seven are owned and the other two are joint ventures) coal mine complexes in New South Wales, Queensland and Western Australia” with the “capacity to produce” approximately “55 million tonnes of saleable coal per annum.”

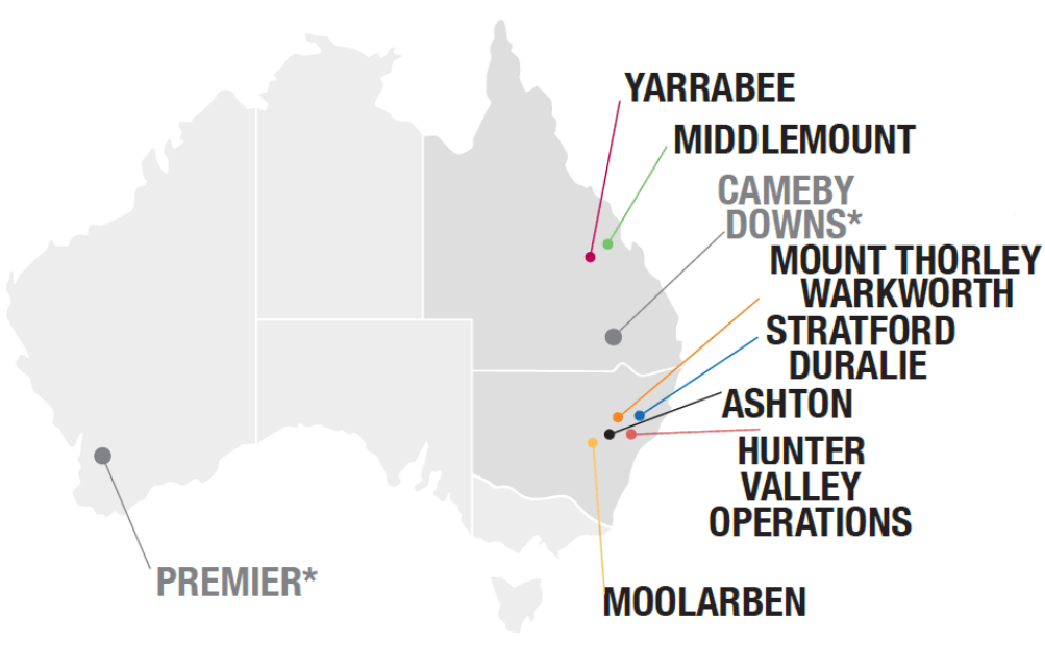

The Location Of YACAF’s Coal Mines

Yancoal Australia’s November 2023 Investor Presentation Slides

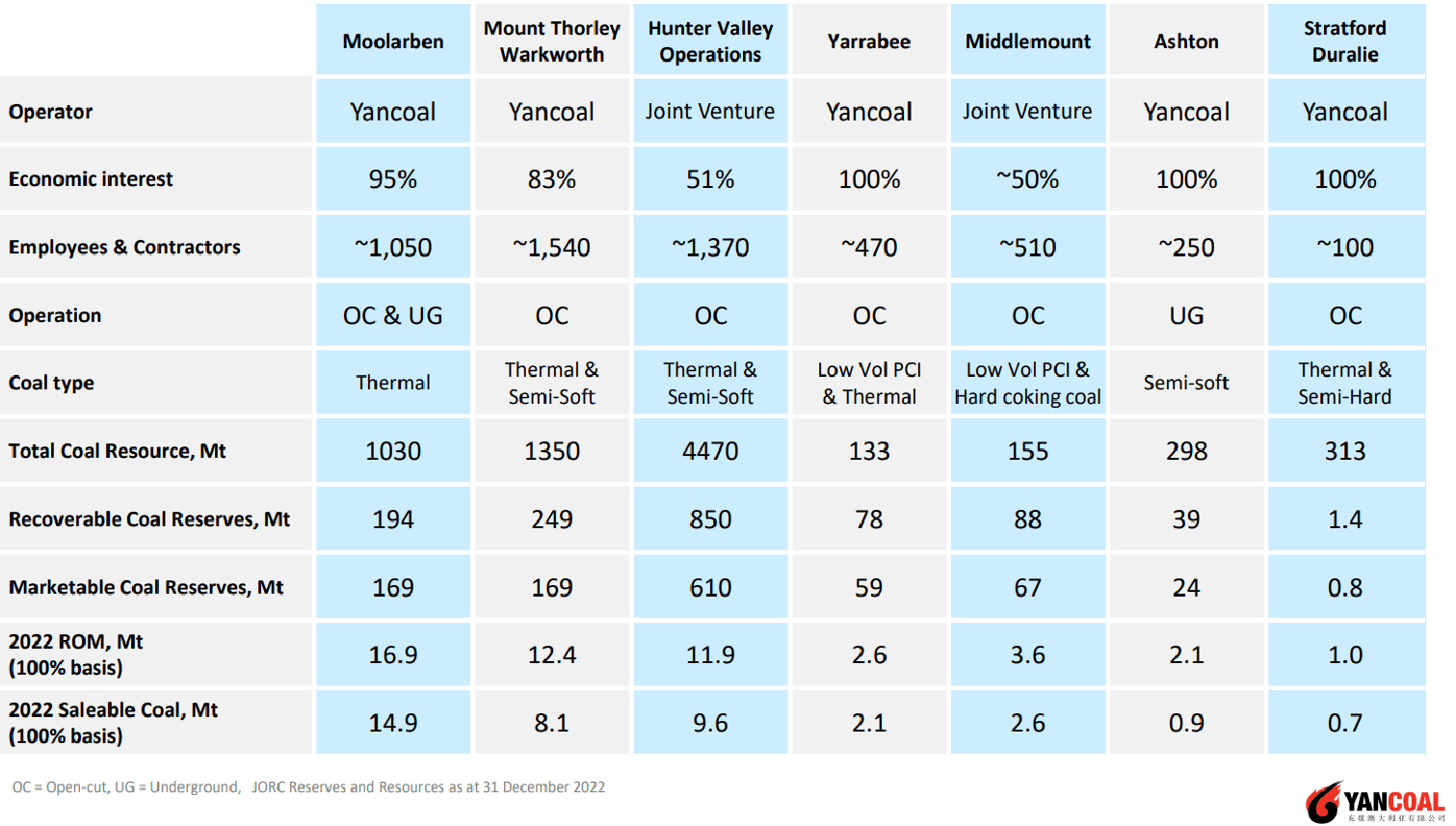

Details Of Yancoal Australia’s Seven Owned Mines

Yancoal Australia’s November 2023 Investor Presentation Slides

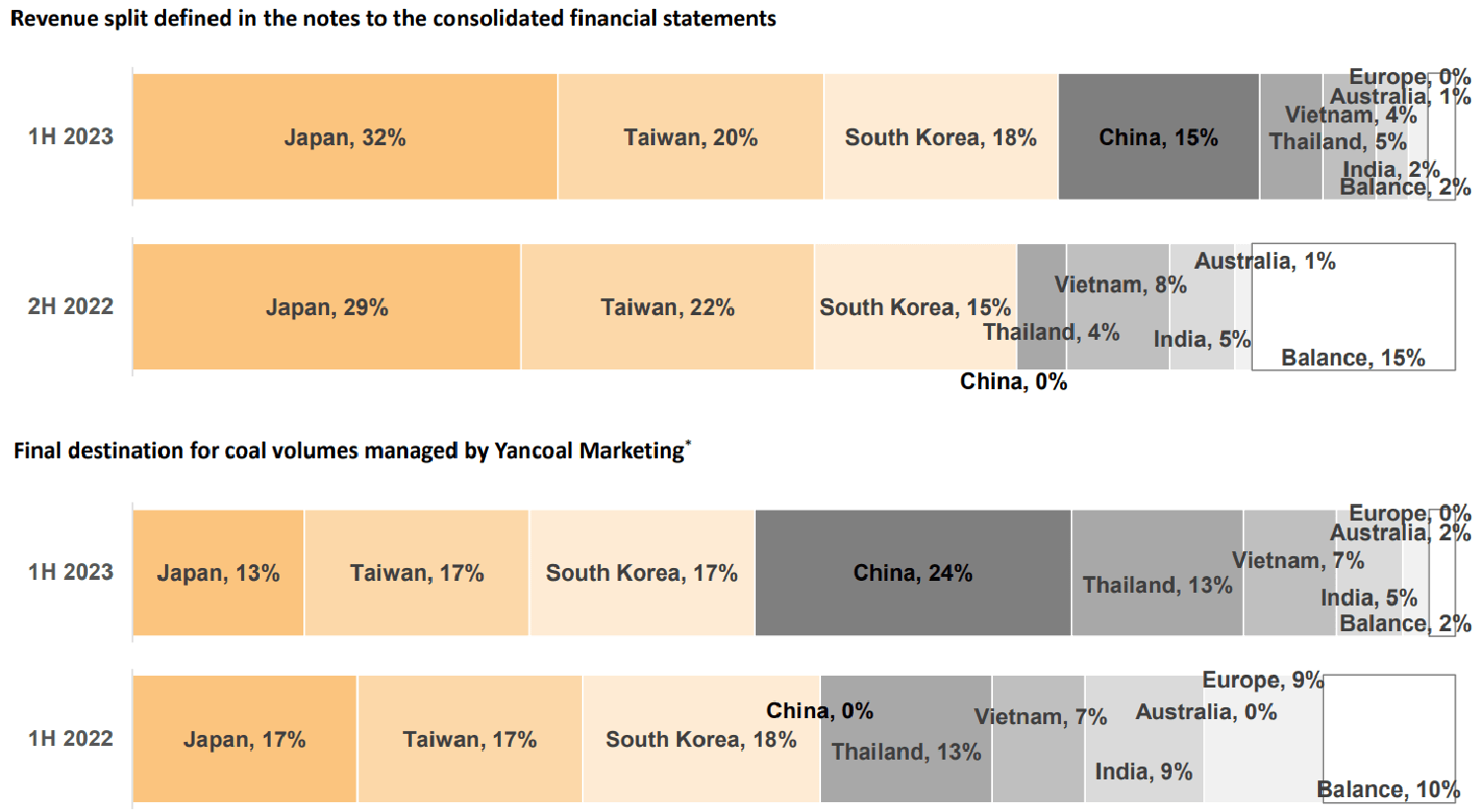

YACAF highlighted in the company’s November 2023 investor presentation slides that it is among the top three coal producers in Australia, alongside Glencore (OTCPK:GLCNF) (OTCPK:GLNCY) and BHP Group (BHP) (OTCPK:BHPLF). Separately, the company disclosed in its most recent interim report that roughly 85% of its top line for 1H 2023 was derived from the Asia Pacific geographic region.

Narrow Revenue And EBITDA reject Expected For 2024 With China In The Spotlight

The market is expecting a narrower top line and EBITDA contraction for Yancoal Australia in the following year, and this is likely attributable to the positive outlook for coal sales to the Chinese market.

Based on consensus financial data taken from S&P Capital IQ, the analysts calculate that Yancoal Australia will record a -4.9% decrease in revenue (in local currency or Australian dollar terms) for FY 2024, which will represent an improvement as compared to the company’s expected -22.6% drop in its sales in the current year. Similarly, the sell side sees YACAF’s EBITDA reject moderating from -40.3% (projected) for FY 2023 to -7.8% in FY 2024.

Yancoal Australia’s Geographical Mix

Yancoal Australia’s November 2023 Investor Presentation Slides

As indicated in the chart presented above, China is one of the key markets for Yancoal Australia, as evidenced by the company’s 1H 2023 geographical mix.

Bloomberg reported earlier in late-September this year that “Australia’s (monthly) exports of thermal coal for power plants and coking coal for steelmaking” to China set a new three-year high in August 2023.

At the company’s Q3 2023 production update investor call (event transcript taken from S&P Capital IQ) on October 20, Yancoal Australia stressed that “China is still a very good market for Yancoal’s products.” Yancoal Australia also shared at the Morgan Stanley (MS) Asia Summit in the middle of last month that it “continues to re-establish sales volumes into China” as outlined in its November 2023 investor presentation.

Recently, Chinese state media Global Times cited an industry expert’s view that “trade in coal, another key Australian export to China” is “likely to set a new record by the end of this year” as “bilateral ties better” in its recent December 7, 2023 news article.

The management commentary, industry statistics, and news flow highlighted above suggest that the recovery of the China market will be a key driver for the improvement in Yancoal Australia’s business and financial performance in FY 2024.

Cash Pile Limits Downside Risks And Offers Upside Optionality

As of September 30, 2023, Yancoal Australia had a net cash position of A$920 million on the company’s books, as disclosed in the company’s Q3 2023 business update press release. The company doesn’t have any debt as of end-Q3 2023, and its net cash is equivalent to about 14% of its current market capitalization.

With respect to downside risks, YACAF won’t be negatively impacted by higher interest expenses, assuming that interest rates remain elevated. More importantly, Yancoal Australia has a very low probability of becoming insolvent with its strong cash position and the absence of debt, even if coal demand weakens and coal prices fall.

In terms of potential upside, Yancoal Australia has the financial flexibility to take on low-cost debt if interest rates reject, or acquire assets at a bargain when opportunities present themselves. YACAF had noted at its Q3 2023 production update investor call that “when there is a great opportunity that shows up, and Yancoal will be confident to take up some sort of (financial) leverage.”

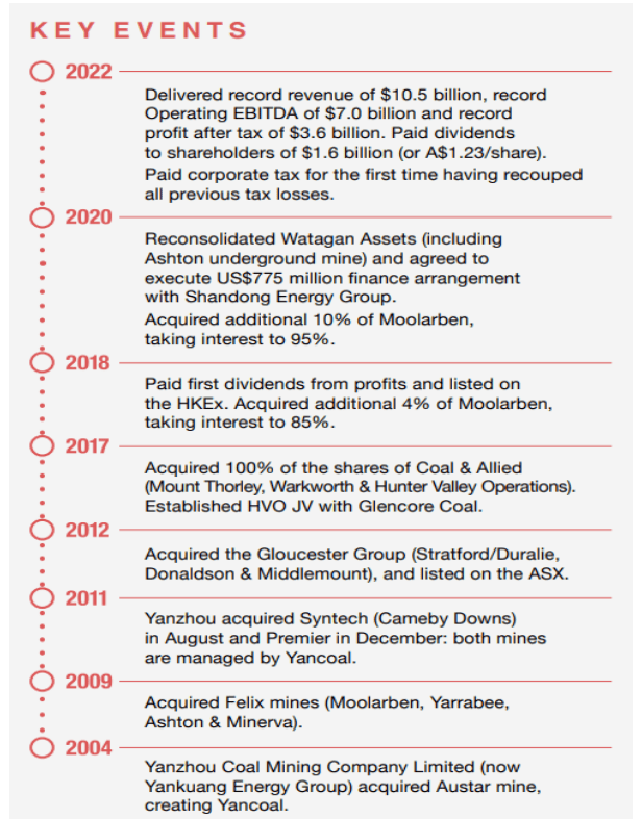

Also, Yancoal Australia has a track record of acquisition deals as indicated in its corporate history presented below. With its cash pile, YACAF has the financial capacity to execute on accretive M&A transactions.

Yancoal Australia’s Corporate History

Yancoal Australia’s November 2023 Investor Presentation Slides

In summary, Yancoal Australia’s robust cash position translates into limited credit risks, and a potential for value-accretive financial management (e.g. leveraging up when rate cuts occur) and capital allocation (e.g. M&A) activities.

Final Thoughts

Yancoal Australia is now valued by the market at attractive consensus forward next twelve months’ Enterprise Value-to-Sales and EV/EBITDA multiples of 0.68 times and 1.36 times (source: S&P Capital IQ), respectively. My opinion is that Yancoal Australia’s shares are likely to trade higher in the future, considering the positive outlook for the China market and the value creation potential associated with its strong cash position.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")