Eoneren

The Company

DTE Energy (NYSE:DTE) is a $23-billion market cap diversified energy company based in Detroit, with operating units including Detroit Edison and MichCon, serving millions of customers in Southeastern Michigan. While utility revenues make up half of the company’s total revenue, DTE has expanded into non-utility energy businesses, such as power and industrial projects, fuel transportation, and marketing. The company’s fuel mix comprises approximately 40% coal, 20% nuclear, and 22% natural gas, with plans to enhance the use of renewable fuels.

DTE aims to phase out coal usage at specific plants by 2028 and 2040, with a broader goal of achieving net-zero carbon emissions by 2050, in alignment with previous commitments to reduce emissions by 50% by 2030 and 80% by 2040.

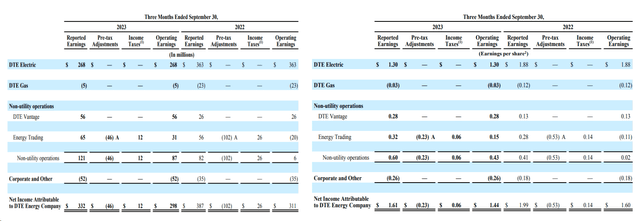

In Q3 FY2023, DTE reported operating earnings of $298 million or $1.44 per share, a decrease from $311 million or $1.60 per share in the same period of 2022.

DTE’s IR materials

This reject was attributed to cooler summer temperatures, impacting earnings by ~$0.15 per share, and an enhance in summer storms. The utility also faced higher one-time operating and maintenance (O&M) cost reductions for storm protection. Despite these challenges, DTE demonstrated effective cost management, as operating expenses fell by 50% to $2.3 billion in 3Q FY2023 compared to $4.7 billion last year. The nine-month operating expenses through September 30 saw a 42% reduction to $7.8 billion compared to the same period in 2022, with notable savings in non-utility fuel and purchased power costs.

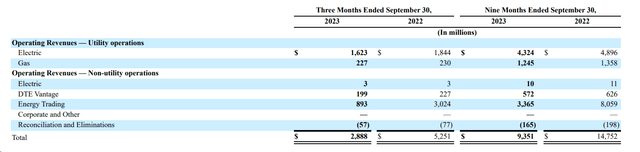

Total operating revenue for 3Q FY23 was $2.9 billion, down significantly from $5.3 billion in 3Q FY2022. Utility revenues, specifically, decreased by 11% to $1.8 billion.

DTE’s 10-Q

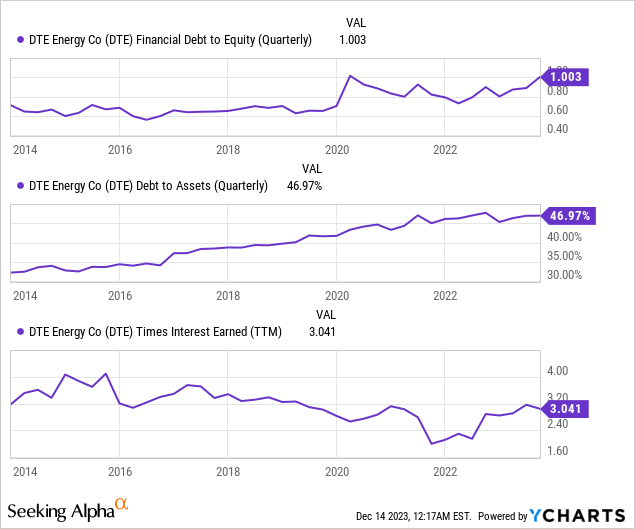

DTE’s interest expense in 3Q FY2023 rose to $200 million, compared to $171 million in 3Q FY2022. The company’s debt-to-equity ratio continued to rise in the last quarter, but it cannot be said that it has become much more difficult for the company to pay its debts, as its times-interest-earned ratio (TIE) remained above 3, which is generally not bad.

DTE recently received regulatory approval for its Integrated Resource scheme, outlining investments in renewable energy assets to reach net-zero carbon emissions by 2050. DTE plans to add 1000 MW of renewable energy annually through 2025 and has filed for approval of a five-year $9 billion capital scheme for grid improvement. Looking ahead, DTE anticipates investing $45 billion in DTE Electric and MichCon over the next decade, focusing on distribution infrastructure and cleaner generation, with additional plans to exchange aging infrastructure and reduce greenhouse gas emissions at DTE Gas through a $3 billion investment scheme. Although the company received a lower-than-expected rate enhance in its 2022 electric rate case, management lowered its 2023 operating EPS forecast to $5.65-5.85 from $6.09-6.40, citing higher 4Q FY2023 storm expenses and lower electricity demand. However, DTE expects these challenges to be offset by O&M reductions and energy trading contract premiums, with management maintaining a projection of 7% growth in operating EPS through FY2027, Argus Research analysts noted in their recent investigate [proprietary source].

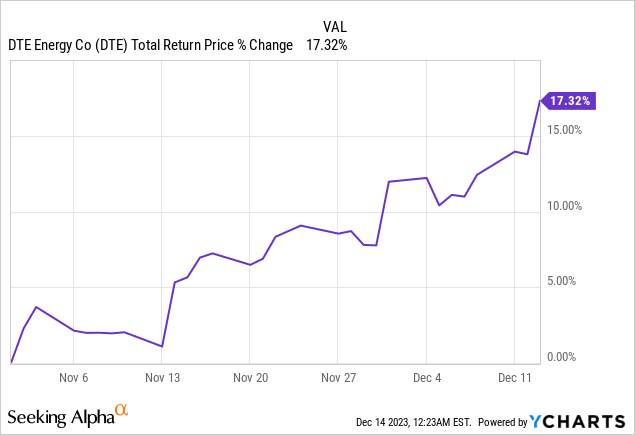

The positive outlook for FY2024 has contributed to the fact that the company’s shares have not sunk after the radical guidance cut for the current year; DTE has even gained an impressive 17.32% in the last few days since the publication of the Q3 report:

In addition to the enhance in guidance for FY2024, the 7.1% dividend enhance and the fact that the stock appeared in Wells Fargo‘s favorite names of the sector for FY2024.

From what I see, despite quite a sluggish 2023, I think DTE Energy is positioned well for FY2024 and beyond with the cost control it has, renewable energy investments, and potential benefits from the automobile industry recovery.

But what about the company’s valuation?

The Valuation

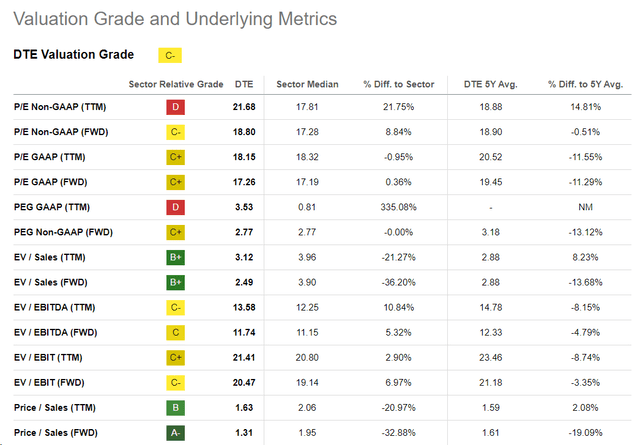

As far as I can see, DTE shares appear to be fairly valued at first glance. First off, Seeking Alpha’s Quant Valuation score is ‘C-‘, with several key metrics being in line with the sector medians (maybe only slightly higher in places).

Seeking Alpha, DTE’s Valuation

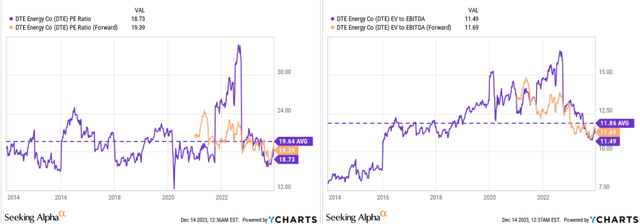

Secondly, we see that the EV/EBITDA and P/E ratios are roughly in the middle of their long-term ranges from a historical perspective, which also makes DTE appear fairly valued.

YCharts, DTE stock, author’s notes

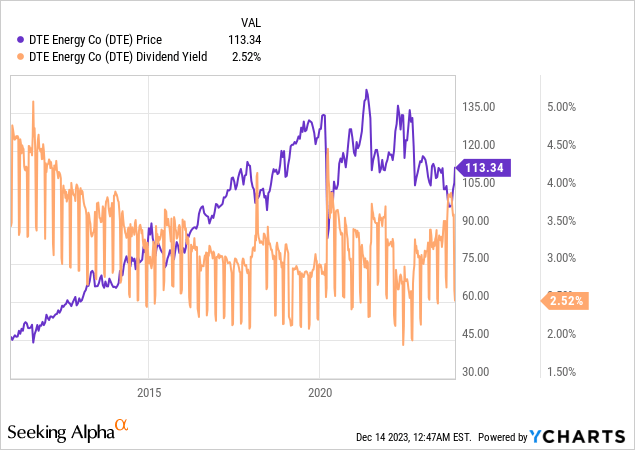

Third, DTE cannot be said to pay an outstanding dividend. Its TTM yield is 47 basis points lower than the sector median and also below its long-term average.

In the longer term, however, DTE clearly has an upside potential to its current valuation levels if the implementation of its strategic plans continues to drive gross profit and EBITDA margins higher, as another Seeking Alpha analyst, Francesco Infusino, wrote recently.

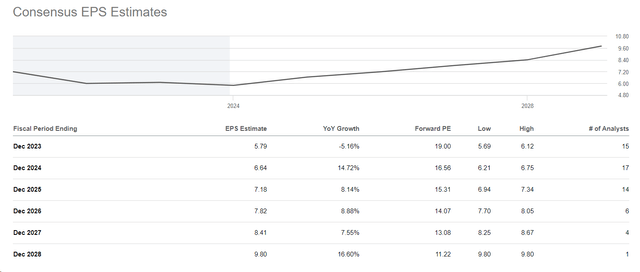

Furthermore, FY2024 and the next few years should furnish a good boost to DTE’s earnings, as Wall Street currently expects. The company is projected to grow out of its current valuation very quickly, leading to upside potential in the size of its next-year EPS growth if the current ‘fair’ multiples are maintained.

Seeking Alpha, DTE’s EPS Estimates

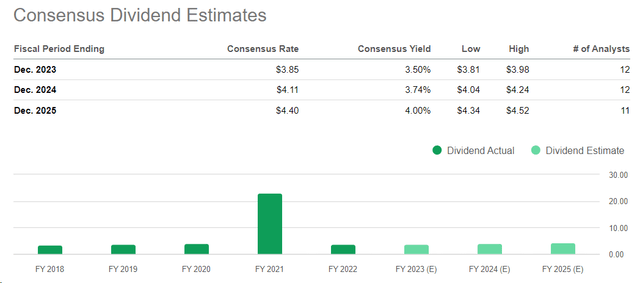

If we add next year’s dividend yield of 3.74% to this nominal growth, we acquire potential growth of around 18.5% by the end of FY2024 under the above conditions.

Seeking Alpha, DTE’s Dividend Estimates

The Bottom Line

While DTE presents potential opportunities, it’s crucial to consider associated risks before investing. One significant risk is the company’s sensitivity to natural gas prices due to its reliance on energy trading. Fluctuations in natural gas prices can impact DTE’s financial performance. Additionally, regulatory challenges in the utility sector pose a risk, as changes in regulations can influence the company’s operations, rates, and profitability. The energy industry is subject to broader economic conditions and geopolitical events, introducing volatility and uncertainty. I also have some concerns about the growing debt-to-equity and the actual reject in financial ratios in 2023, which could continue next year despite positive management forecasts.

However, in my view, the company’s recent operating performance and strategic initiatives signal long-term growth potential, with a positive trajectory for earnings and dividends. Despite a temporary dip in 3Q FY2023 operating earnings, management’s updated FY2024 EPS forecast suggests robust future performance, possibly reaching low double-digit EPS growth in FY2024. By combining the forward dividend yield of ~3.74% with the nominal growth in EPS (amid a maintained P/E ratio), I reckon the potential upside by the end of FY2024 at ~18.5%, indicating that DTE stock is currently undervalued.

Therefore, I rate DTE stock as a ‘Buy’ today.

Thanks for reading!

Q2 2024 Earnings Call Transcript")