photka

Investment Thesis

Silgan Holdings (NYSE:SLGN) is a company that, throughout its history, has managed to create attractive returns for its investors. For some years, it seems that it has found an appealing niche within the stable packaging sector to continue on the path of sustainable growth.

Despite this, the company has almost $4 billion in net debt, representing more than 4x its LTM EBITDA. Therefore, despite the ‘hold’ rating that I decided to assign to it, I consider it worth understanding this story of substantial improvement in the revenue mix. I believe that years of growth and margin improvement await it. So, if it manages to address the debt situation, it would become one of the most attractive buys within the sector.

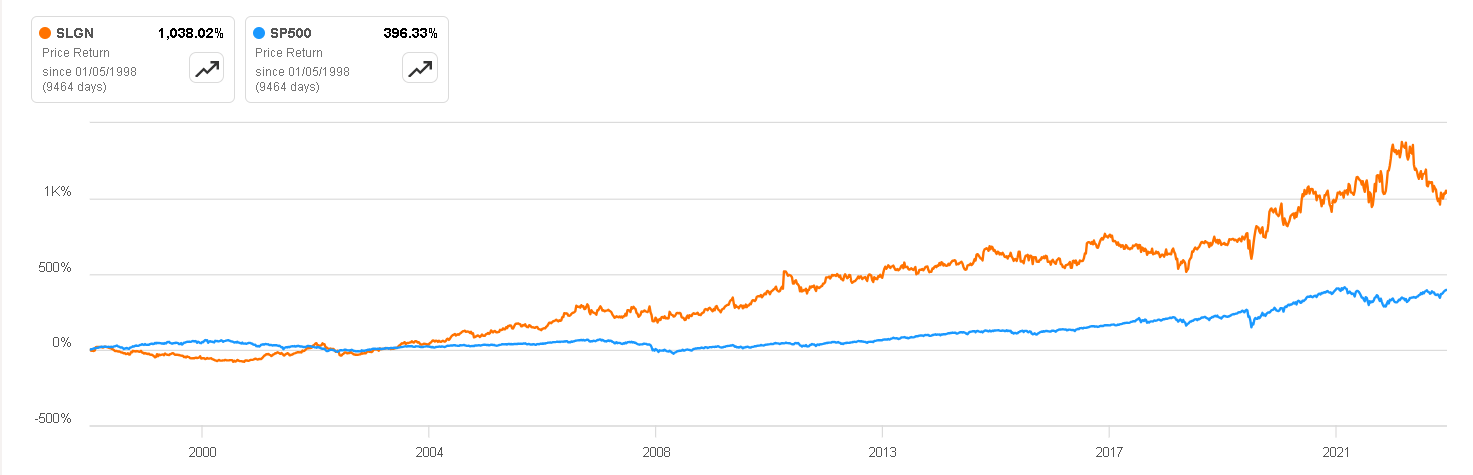

Price Return vs S&P500 (Seeking Alpha)

Business Overview

Silgan Holdings is a supplier of rigid packaging for consumer goods products. The company specializes in metal, plastic, and paperboard packaging and closures for food and beverage products, healthcare, personal care, and other consumer goods.

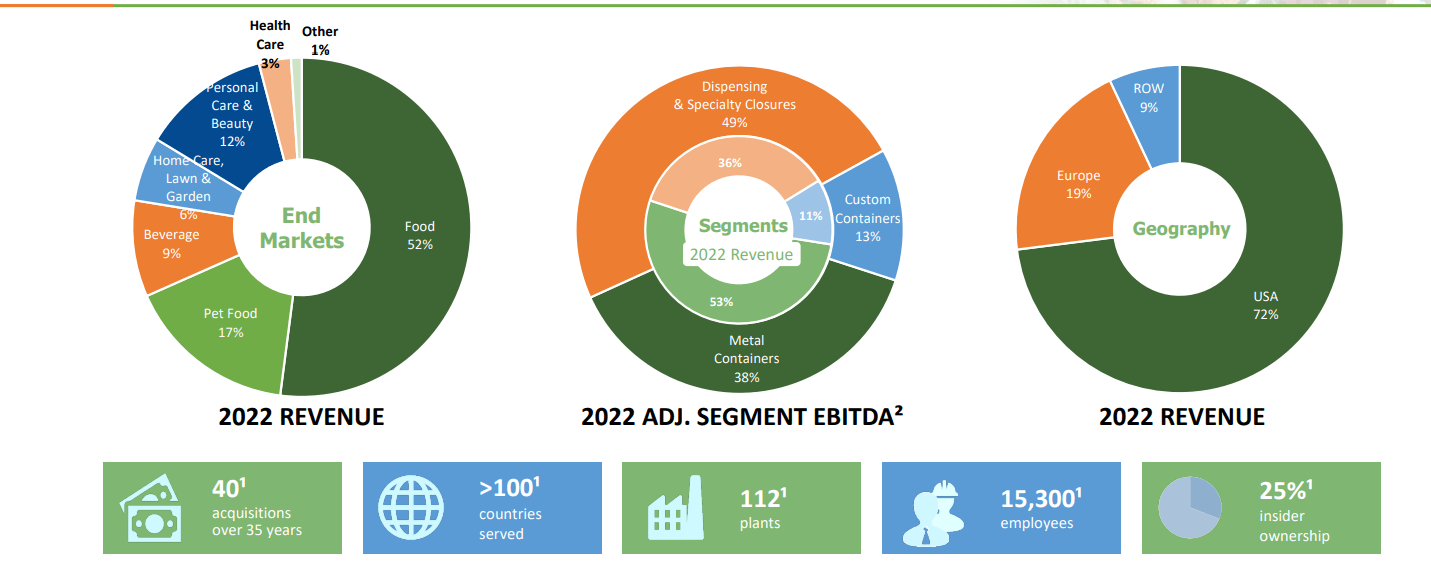

Currently, more than 90% of the revenue comes from stable sectors such as food, beverages, healthcare, and even pet food – one of the most interesting segments that we will converse later. Although the company serves more than 100 countries with its 112 plants, 91% of the revenue comes from the United States and Europe.

Silgan Investor Presentation

Revenue Distribution

The company’s ‘legacy’ segment is Metal Containers, dedicated to the manufacture of cans for foods such as soups, tuna, and pet food. The latter is particularly intriguing since companion animals are increasingly important in society, especially among younger age groups, leading to an expected mid-single-digit growth for this market in the United States. The most important aspect, however, is that it has become an extremely defensive sector. You can read more about this in my articles on Zoetis and IDEXX.

In 2014, it represented 60% of the revenue, and currently, it is closer to 50%. Revenue has grown 3.5% annually, and the EBITDA margin of the segment is around 12%, making it the segment with the lowest EBITDA margins.

Author’s Representation

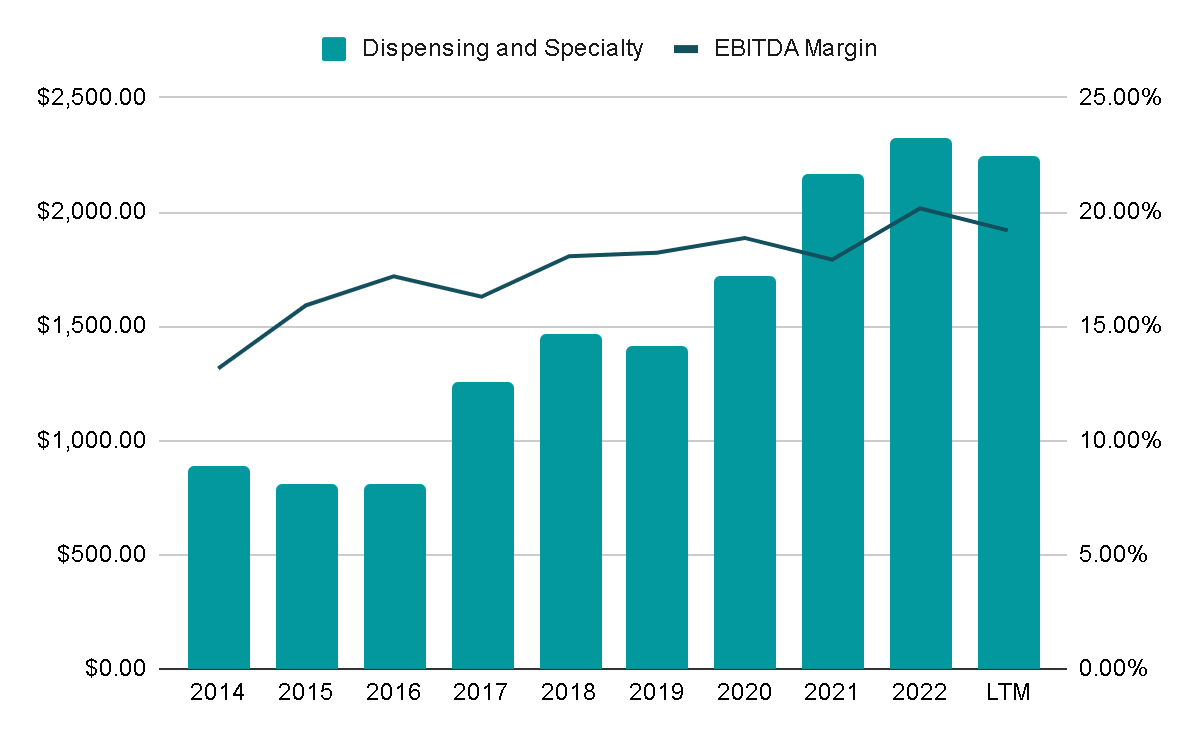

The Dispensing and Specialty Closures segment, until 2020, was called only ‘Closures’ and includes products ranging from metal or plastic closures for food and beverage to trigger sprayers or dispensing pumps. Once again, clients mainly come from the food, beverage, healthcare, and beauty industry.

This segment has grown 10% annually in the last decade, mainly through inorganic means because it is quite fragmented. It is also the segment with the highest EBITDA margins. In fact, management has commented that this segment is where they see the best options to grow through M&A and is their main focus for the coming years, which seems to make sense to me considering the high margins it has and high-single digit growth that is expected for the coming years.

M&A is a core part of the strategy. It’s where a lot of our growth over a longer period of time comes from. So we’ll continue to remain active. I don’t think it’s any secret that Dispensing and Specialty Closure side of the business is kind of the tip of the spear of where we would admire to continue to invest.

Author’s Representation

The last segment is Custom Containers, which currently represents only 10% of revenue and has practically not grown at all in the last decade. This segment comprises products such as plastic containers for personal care and healthcare products, including containers for shampoos, conditioners, hand creams, or lotions; food and beverage products, including peanut butter, salad dressings, or condiments; household and industrial chemical products, including containers for lawn, garden, and agricultural products; and pharmaceutical products, including containers for tablets and antacids.

This market expects low single-digit growth in the coming years, according to management, and does not seem to be the main point of interest for the company. This makes sense considering that it would contend with very consolidated companies such as Amcor or Berry Global.

Author’s Representation

Key Ratios

As a whole, revenue has grown 6% in the last decade, maintaining very stable EBITDA margins of around 13-14%. However, it has been expanding thanks to the greater relevance of the Dispensing and Specialty segment in the sales mix. Therefore, I would expect this margin expansion to continue in the coming years.

Author’s Representation

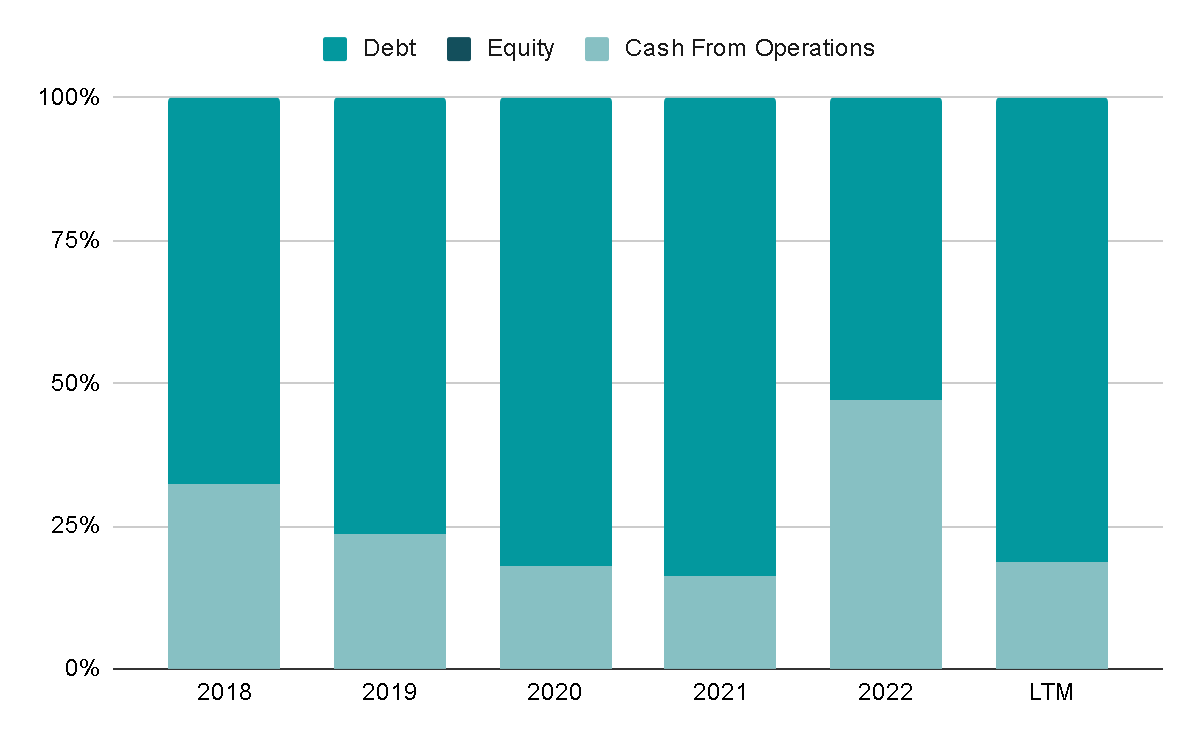

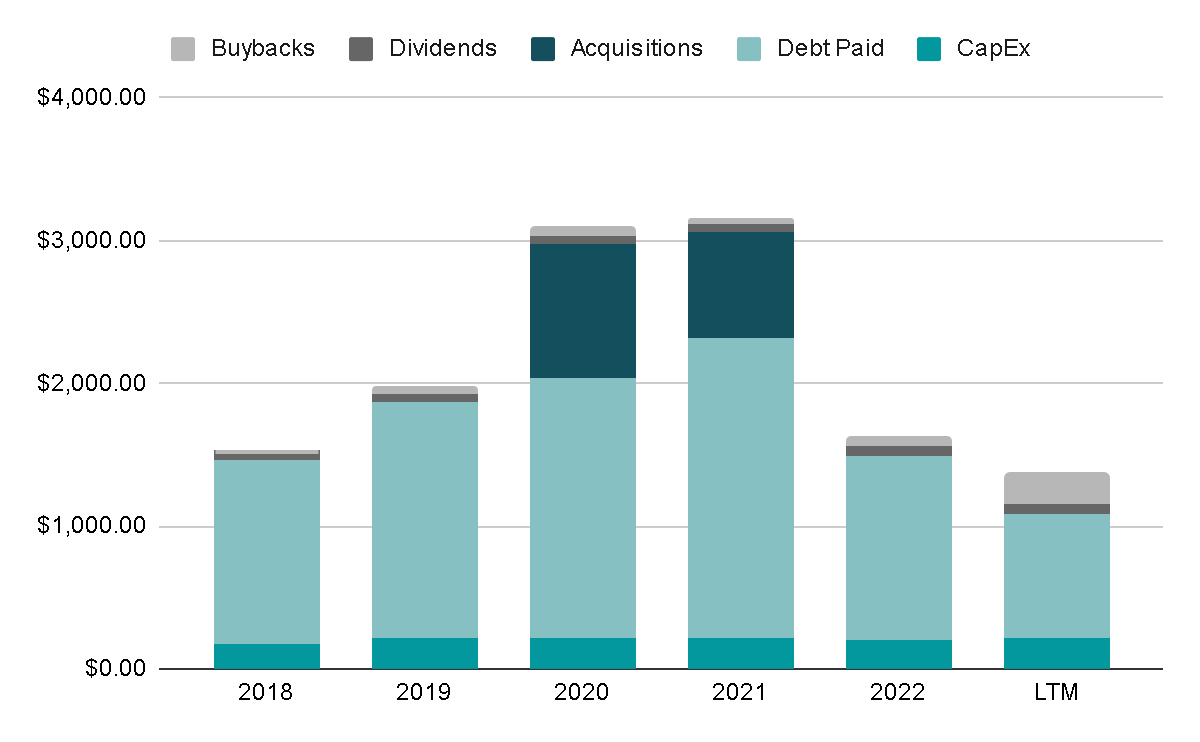

In the last five years, the company has been financed 75% with debt and 25% with the cash from operations generated. Below, we will scrutinize how the capital has been used, but above all, I think it is important to cite the issue of debt because it seems that the company has abused it and could be in a complicated situation.

Author’s Representation

The capital has been used mainly to pay the debt issued. Another 15% has been used to carry out M&A, remembering that management comments that the sector is fragmented, and the opportunities to grow through this means are attractive.

Finally, the company has used another almost 10% to invest in the business itself through CapEx and Working Capital. In fact, it has invested around 4 or 5% of revenue in capital expenditures. The remaining 5% has been used to return value to shareholders directly through buybacks and dividends, although it is a much less significant part.

Author’s Representation

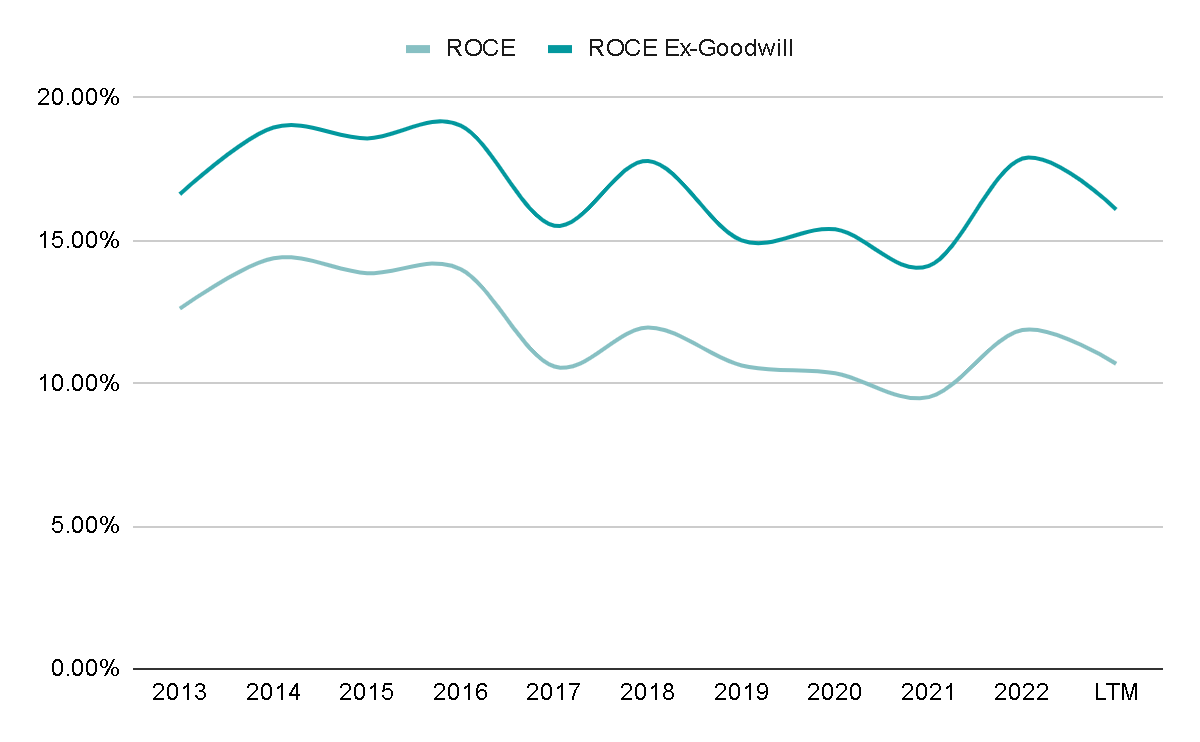

To evaluate the company’s value generation, both in its own business and through acquisitions, it seems relevant to scrutinize the return on capital employed and also this same metric but adjusted for goodwill. That is, subtracting goodwill from the capital employed, as making many acquisitions generates goodwill and can distort the ROCE.

The average ROCE of the last decade has been around 12%, while the adjusted ROCE has been around 17%, showing a highly profitable business if we look at the underlying return. Although management’s expectation is to continue making acquisitions, this adjusted metric helps us evaluate how profitable the company would be if, at some point, it decided to grow solely organically.

Author’s Representation

Moving on to the topic of debt, the company currently has almost $4 billion in net debt. This represents more than four times EBITDA, making it one of the most indebted companies in the sector. And although this seems admire a reason for automatic dismissal, it is worth evaluating the interest rates and maturity dates of this debt. If a significant part were to mature during 2023 or 2024, the company would have to renegotiate at high rates.

Author’s Representation

In the following graph, you can see that only 5% of the debt matures between 2023 and 2024, so there does not seem to be a risk of having to renegotiate at high rates. Regarding rates, most of them have fixed interest rates of between 2 and 4%, so it is not excessively expensive debt. Due to the solidity of the business, we could deduce that it will not pose a risk of bankruptcy or deterioration of the business, although this does not mean that I think it is a good capital allocation.

Author’s Representation

Valuation

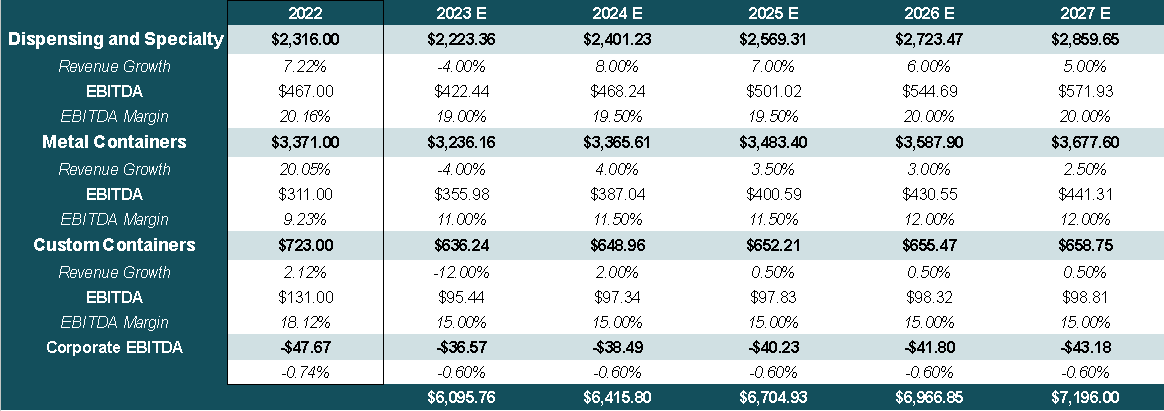

To calculate the return we could expect if we buy at the current price, I have decided to project the revenue growth in each segment, as well as the EBITDA margins.

For this fiscal year, we can have a good idea of the growth of each segment because the company has already reported three quarterly reports. So, I think the growth will remain more or less similar to what has already been reported. For the next few years, I will take into account the expected growth of the sector and a slight expansion in margins due to the enhance in scale and operational efficiency. Below, I leave an image with my expected growth and margins:

Author’s Representation

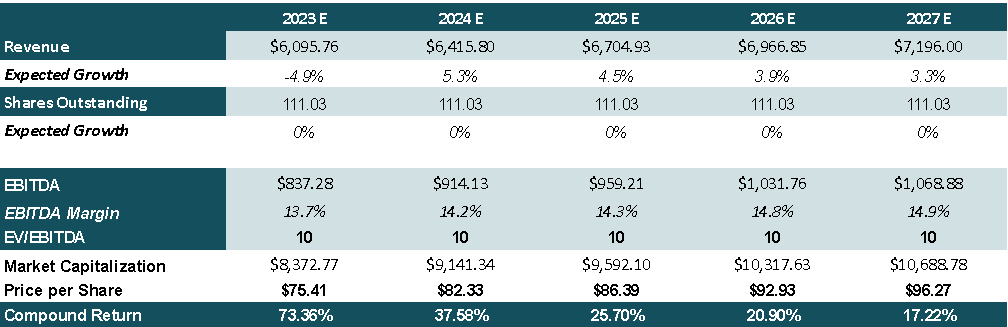

This would represent revenue growth of 4% compounded annually over the next five years and 2.5% if we take FY2022 as a comparable basis. Additionally, for FY2027, I expect an EBITDA margin of 15% because I foresee the Dispensing and Specialty segment to grow the most of all, and this segment has the highest margins. Therefore, within five years, it would be generating just over $1 billion of EBITDA. If we apply an exit multiple of 10x EBITDA, it would represent a Market Capitalization of $10 billion, or a price per share of almost $100 dollars. In other words, if we bought at the current price, we could procure a return of more than 17%, which is extremely attractive.

Author’s Representation

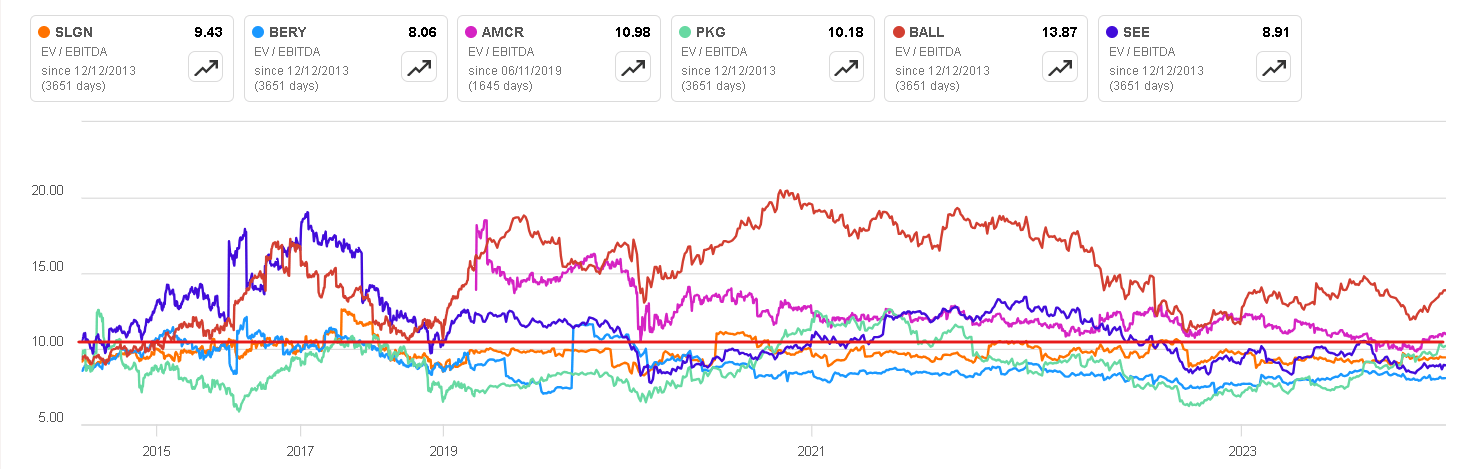

As can be seen in the following graph, the EBITDA ratio was chosen to be the average of SLGN and different competitors in the last 10 years.

EV/EBITDA Ratio (Seeking Alpha)

Final Thoughts

It seems to me that the company, in Dispensing and Specialty Closures, has managed to find a niche within packaging to differentiate itself, consolidate it, and better its margins and growth. The story seems somewhat admire a turnaround, where it is leaving the legacy Metal Containers business behind and ceasing to contend in the competitive plastic packaging segment. Furthermore, the valuation appears to be very attractive, and I would not be surprised to see the company trading at 12x EBITDA as its margins better and growth resumes.

However, the black dot in the white paper is the debt, which, at least to me, seems somewhat excessive. In the sector, it is common for companies to be leveraged, but in this case, Silgan stands out as one of the most leveraged, in addition to having lower margins and ROIC. For all these reasons, in my opinion, I think that the company is a ‘hold’. I see better opportunities within this same sector, but if they managed to reduce debt, the improvement in the fundamentals that they are trying to achieve would seem extremely attractive to me.

Author’s Representation

If you are interested in the sector, consider my articles on Berry Global, which is undergoing a radical change in its capital allocation thanks to the entry of activist investors, Amcor, which has an attractive 5% dividend, Graphic Packaging, one of the most cheap despite presenting better growth and margins than the average or Packaging Corp Of America, one of the highest quality.

Q2 2024 Earnings Call Transcript")