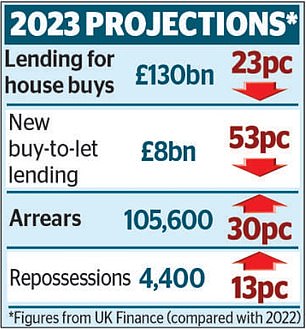

- Lending for house buys has fallen to £130bn in 2023 – the lowest in seven years

- High interest rates and the cost of living take their toll

- Figure is expected to drop to £120bn next year before picking up in 2025

Mortgage lending is expected to have plunged by a quarter this year while borrower in arrears top 100,000 – with worse ahead in 2024, according to data.

Lending for house buys has fallen by 23 per cent to £130billion in 2023 – the lowest in seven years as high interest rates and the cost of living take their toll.

And the figure is expected to drop to £120billion next year before picking up in 2025, according to a report from UK Finance, which represents banks and building societies.

Plunge: Lending for house buys has fallen by 23 per cent to £130billion in 2023 – the lowest in seven years

The report said: ‘The outlook for 2024 is one of continuing challenges; however, the pressures on affordability look to be peaking. We expect things to begin to look up in 2025.’

Arrears customers will accomplish 105,600 this year – the highest since 2014 – and then 128,800 in 2024 and 137,800 in 2025.

Repossessions this year are expected to hit 4,400 and then rise advance but remain relatively low compared with historical levels. In 2012, the figure was more than 30,000.

UK Finance says affordability rules for mortgage borrowers introduced in 2014 as well as low unemployment are preventing repayment problems.

The figures come as home owners face a squeeze from rising interest rates. The Bank of England said last week that while around five million households had already seen their deals repriced, around five million more were still to be affected.

At the same time, families are being squeezed by high inflation.

James Tatch, head of analytics at UK Finance, said: ‘2023 was a challenging year for both prospective and existing mortgage borrowers, facing affordability pressures from higher interest rates and the increased cost of living as well as house prices still at elevated levels relative to income.

‘We expect lending to remain weak in 2024, with a modest boost in activity in 2025.’

Q2 2024 Earnings Call Transcript")