Aoraee/iStock via Getty Images

Introduction

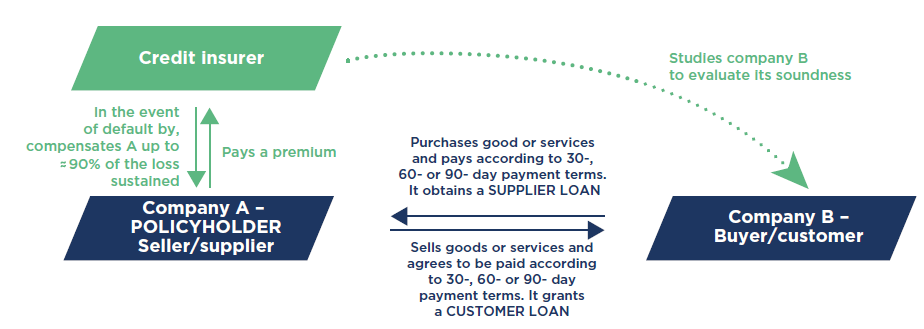

Coface (OTC:COFAF) is an insurance and reinsurance company focusing on an underappreciated and undercovered segment of the insurance market: trade credit insurance. Approximately 90% of the company’s business consists of these types of credit insurance, and the principle is very simple. A company can protect itself against a default or a non-payment of a customer by paying an insurance premium to Coface which will in turn cover any potential defaults (and can subsequently chase down the defaulting party).

Coface Investor Relations

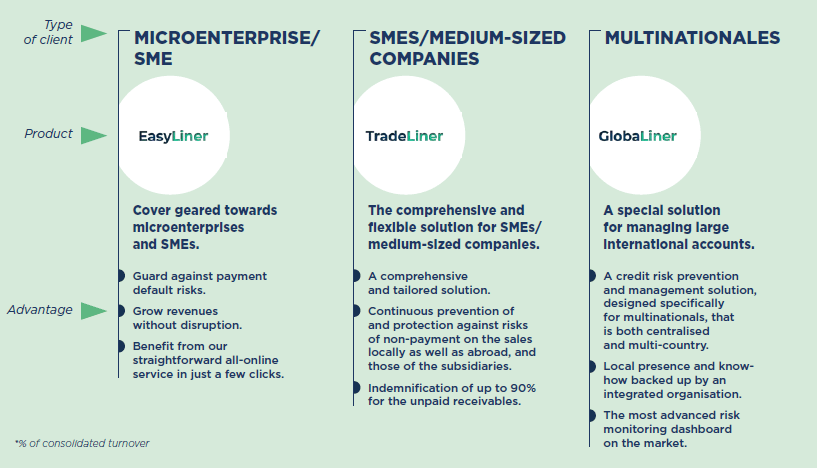

Trade credit insurance is well-known and well-integrated in today’s international trading environment, and Coface is one of the very few public companies specifically focusing on this subsector of the insurance industry.

Coface Investor Relations

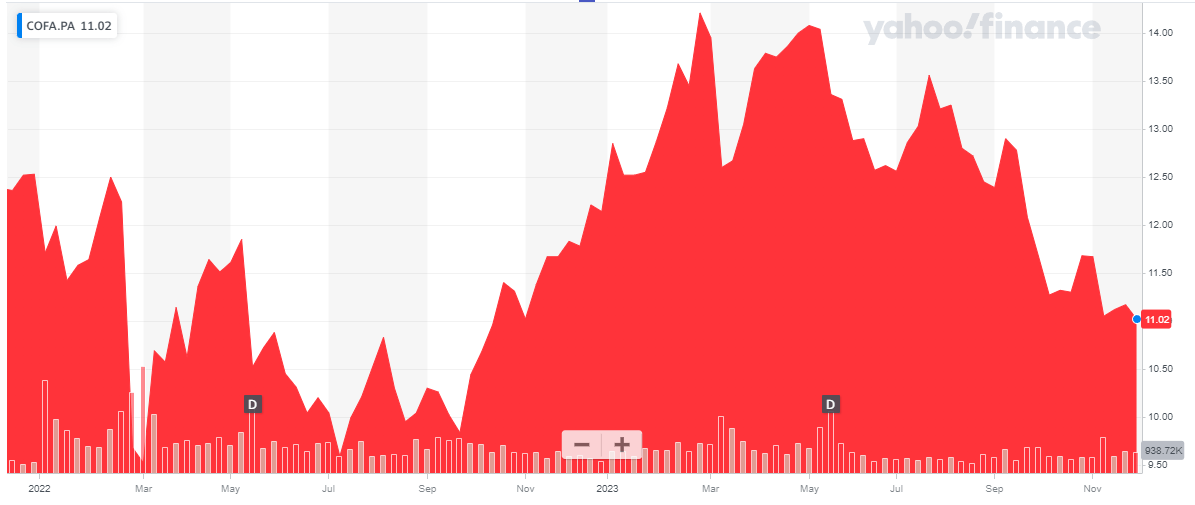

Coface is a French company and its listing on Euronext Paris definitely is the most liquid listing to trade in the company’s shares. The average daily volume in Paris is close to 200,000 shares, representing a monetary value of approximately 2.2M EUR. There are currently 149M shares outstanding, resulting in a market capitalization of approximately 1.65B EUR. The company’s largest shareholder is Arch Capital Group (ACGL), which has a market capitalization of almost $30B. Arch Capital has a stake of approximately 30%.

Yahoo Finance

Unfortunately, the company’s website mainly contains ‘download-only’ links, but you can find all relevant information and documentation I will be referring to on this page of Coface’s website.

Strong results so far suggest FY 2023 will be a good year

Although a lot of French companies only publish detailed financial statements every six months, Coface does publish a detailed income statement and balance sheet overview on a quarterly basis.

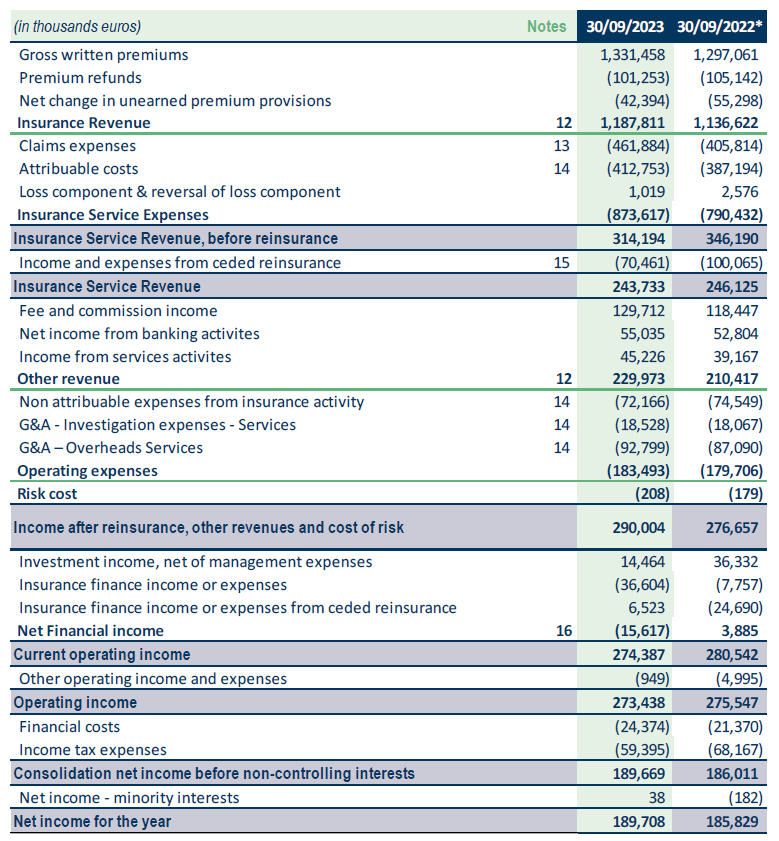

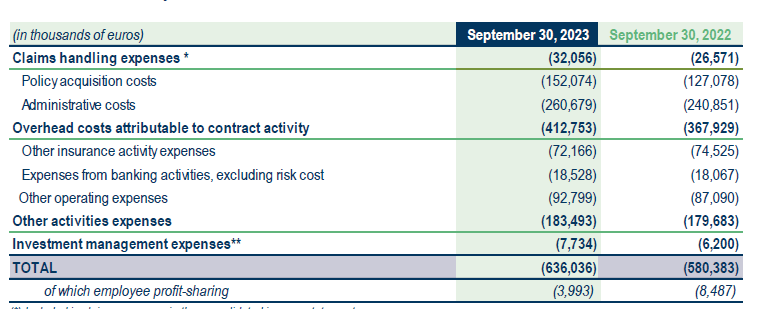

Looking at the insurance company’s performance in the first nine months of the year, we see Coface reported a total amount of 1.33B EUR in gross written premiums, while the total insurance revenue came in at 1.19B EUR.

Coface Investor Relations

Interestingly, the total cost structure remains under control and as you can see, even though the total amount of claims expenses increased by a double-digit percentage, the 462M EUR in total claims expenses actually is a pretty low percentage of the total insurance revenue.

Of course, the ‘attributable costs’ are relatively high as well, and these are predominantly the G&A expenses related to handling the claims and managing the investment portfolio.

Coface Investor Relations

After taking all these elements into consideration, the company reported a total insurance service revenue of almost 244M EUR, a small decrease compared to the result in the first nine months of last year. Fortunately, the total amount of other revenue minus the other expenses was very strong thanks to a strict cost control (operating expenses increased by just over 2% while the other revenue increased by almost 10% to just under 230M EUR) and this was a major help to boost the income after reinsurance and other revenues to 290M EUR. The operating income was 273.4M EUR after deducting the net financial expenses (related to the investment income and insurance finance expenses). Coface also faced a 59.4M EUR tax bill and a 24.4M EUR finance cost on the corporate level, resulting in a net income of 189.7M EUR. An boost of just over 2% compared to the first nine months of last year.

As there are currently 149M shares outstanding, the EPS in the first nine months of the year was approximately 1.27 EUR per share, and this indicates the company is likely heading towards a full-year EPS of at least 1.60 EUR per share. And as Coface has a payout ratio of ‘at least 80% of its earnings’, the dividend per share could very well come in at 1.28 EUR per share for a dividend yield of approximately 11% based on the current share price. The dividends paid in the past few years were even higher than the 1.28 EUR I just mentioned to a high dividend shouldn’t come as a surprise. The dividend payable over FY 2022 was 1.52 EUR per share.

So, what’s the catch? Why is the stock trading at just around 7.5 times earnings with a 11% dividend yield? First of all, it is a smaller insurance company focusing on a niche segment of the market. Secondly, insurance companies all over Europe have been hit pretty hard this year and while some have seen their share prices recover, others haven’t, and I think Coface belongs to this group. And finally, as the world economics and politics are very volatile, it is not unreasonable for the market to slap a higher risk premium on an insurance company specifically focusing on trade insurance. Sure, it can boost the premiums to account for the increased uncertainty and volatility, but that may not fully cover the increased risks.

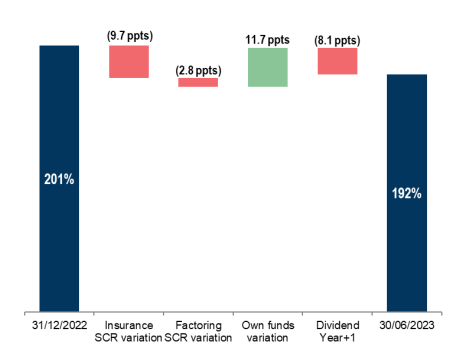

That being said, Coface’s Solvency Ratio currently vastly exceeds the company’s own targets. At the end of June, Coface’s Solvency Ratio was 192%, as you can see below.

Coface Investor Relations

As Coface has a target solvency ratio of 155-175%, the current solvency ratio still exceeds the company’s own targets, so there should be no issue to preserve a generous dividend policy.

As of the end of September, the total equity value on the balance sheet was 1.98B EUR resulting in a book value of 13.29 EUR per share and even after deducting all the intangible assets (155.5M EUR in goodwill and 77.8M EUR in other intangible assets), the tangible book value per share remains robust at 11.7-11.75 EUR per share which means Coface is currently trading at a mid-single digit discount to its tangible book value.

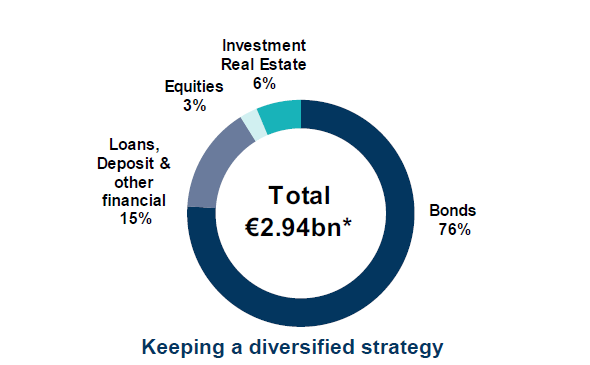

At the end of September, its 2.94B EUR investment portfolio mainly consisted of bonds, but Coface also invested close to 200M EUR in real estate.

Coface Investor Relations

While the quarterly update did not disclose a whole lot of details on this investment portfolio, 63% of the bonds had a credit rating of A and higher. Only 5% of the bonds had a credit rating of BB and lower.

Investment thesis

While I admit the trade credit market isn’t an easy one to fully grasp, let’s not neglect Coface has a long-standing history in this sector and currently is the third-largest player in the world (behind Allianz Trade and a subsidiary of Grupo Catalana Occidente). Coface also recently dealt with an upcoming maturity of a debt security as it issued 300M EUR of Tier 2 notes with a 5.75% coupon and a maturity in 2034 to fund the maturity of the 227M EUR 4.125% loan due in March 2024. This removes another key risk.

Considering the stock is currently trading at less than 8 times earnings and considering we are likely looking at an 11% dividend yield (subject to the 12.8% dividend withholding tax in France), I think a long position in Coface is warranted. I currently have no position in Coface, but I will likely begin a long position in the next few days. Initially for the dividend, but I wouldn’t be surprised to see the stock proceed towards a 9-10 times earnings multiple over the next 12 months.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")