NicolasMcComber

Who are Canadian Tire?

Canadian Tire Corporation Limited, (TSX:CTC:CA) listed on the TSX under the ticker (‘CTC’), is a Canadian group of companies that includes a Retail segment, a Financial Services division and a REIT, (CRT.UN:CA) The flagship retail business dates back to 1922 and provides Canadians with products for life in Canada across its Living, Playing, Fixing, Automotive and Seasonal & Gardening divisions. Party City, PartSource and Gas+ are key parts of the Canadian Tire network. The Retail segment also includes Mark’s, a leading source for casual and industrial wear; Pro Hockey Life, a hockey specialty store catering to elite players; and SportChek, Hockey Experts, Sports Experts and Atmosphere, which offer the best active wear brands. Canadian Tire is a strong player in Canada, competing with the likes of Walmart (WMT) and Target (TGT).

Investment thesis.

CTC is a stable and well established player in the Canadian retail market.

Business performance has been under pressure in 2023 as the Canadian economy cools, and the stock valuation has come down to reasonable levels.

The balance sheet is in good shape, and while some debt has refinanced in 2023, the forward debt maturity profile and servicing costs look stable.

Business strategy seems solid, and progressing well.

CTC pays a decent forward yield of 4.84% with a 13 year dividend growth record and safe payout ratio.

I expect 2024 to show some continued performance challenges, and a lower price, but would look for an entry point with a 5%+ yield as I see CTC as a good, conservative dividend growth stock.

Recent performance.

CTC stock price has been quite volatile, with a 52 week trading range of CAD 131 to CAD 190, at current levels it trades at around 75% of the high and 10% above the October low.

CTC reported its Q3 results on Nov 9th, which showed the impact of the cooling Canadian economy on consolidated comparable sales, which dropped by 1.6% compared to Q3 2022.

The breakdown between brands showed a clear shift from discretionary purchasing to essential purchasing, with the biggest drop in the sports apparel segment (7.4%) partly offset by a 0.6% enhance in retail sales, and a 4% enhance in the automotive segment.

Earnings for the quarter were a negative CAD 1.19 per share, which reflects the impact of a one off charge of CAD 328m, (CAD 5.28 per share) relating to a Scotiabank transaction.

Scotiabank have held a 20% share of Canadian Tire Financial Services since 2014, with an option to demand CTC to repurchase these shares. This was exercised and CTC repurchased the shares in the quarter, resulting in the CAD 328m charge.

On a normalised basis, quarterly earnings we positive, but down 11.4% due to the impact of financing costs and credit impairments in the retail and financial services segments. This represents a direct impact from a cooling Canadian economy.

The snapshot below is from the full quarterly shareholder report.

Investor Report

Year to date, the consolidated revenue and net margins were both down about 2% year on year, financing costs due to increased cost of debt increased 40% year on year.

All this translated to a big drop in net income YTD from CAD 620.2m to CAD 141.9m.

Outlook

The key short term risk for Canadian Tire is tied to the performance of the Canadian economy, and consumer trends. While CTC has some products in the ‘essential’ category, the bulk of their revenues are consumer discretionary. as the economy continues to cool, revenues will continue to slide. My outlook would be for a advance 2-3% reduction in revenues through 2024.

Interest costs and debt impairments will also be a drag on short term performance, and again I would expect to see the bottom line income reduce by around 10% year on year in 2024.

The Bank Of Canada December meeting held rates at 5%, and the outlook is for this rate to hold well into 2024 before easing to 4.5% by year end, according to Reuters.

Strategy.

In the longer term, CTC have 2 key strategic areas.

Triangle Rewards – is their Reward programme, which they have been developing as a key data generator for an AI proposition to boost sales in both the retail, and financial services segments. The Scotiabank transaction mentioned above secures 100% ownership of this asset for CTC, and supports this long term strategy.

‘Better Connected’ is the key strategic investment being made by CTC, as they pivot into an Omni-sales business model, supplementing the established retail outlets with an integrated online sales proposition.

Both of these seem to be well founded strategically, and progressing well in execution. To keep costs in line with slowing revenues, some of the investments have been pushed advance out, but progress continues.

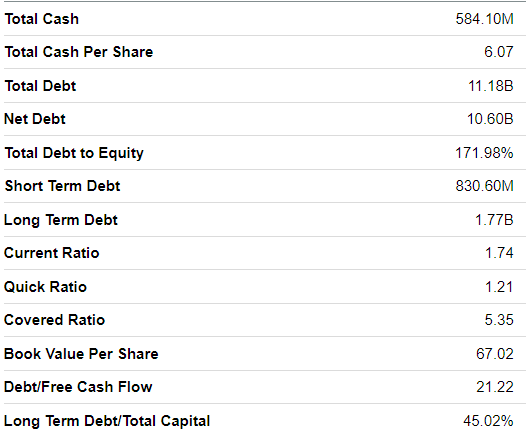

Balance sheet.

The balance sheet is in pretty decent shape for the retail segment, with long term debt to capital at 45%. I would prefer to see below 40% however.

Debt servicing metrics are good, with a current ratio of 1.74x and a quick ratio of 1.21x, so while dept servicing costs are increasing, the cash generation is strong enough to handle this.

Seeking Alpha

Rating agencies view of CTC reflects this, with both S&P and Moody’s issuing a BBB grade with a stable outlook.

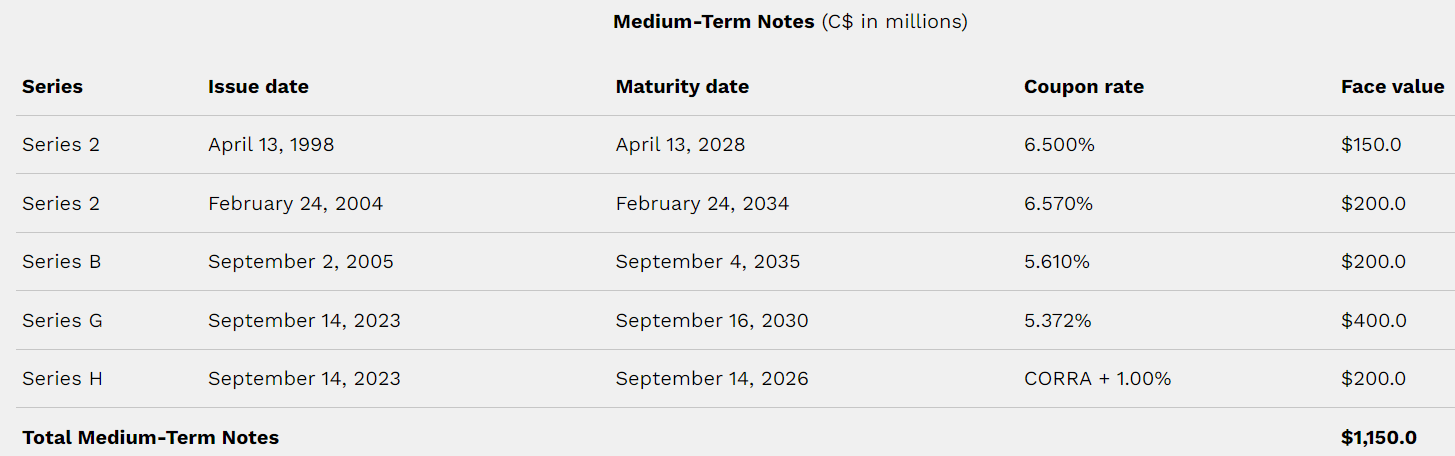

During the quarter, about CAD 1bn of debt was refinanced, with CAD 984m at a rate of 3.2% being repaid, and replaced with CAD 1.1bn with an average rate of around 5.5%.

The ongoing long term debt is well staggered, with maturities from 2026 though 2035.

CTC Disclosure

Dividend.

CTC dividend policy is to pay out 30-40% of earnings as dividend. Dividend history has been solid, with 13 years of dividend growth, and a 13.9% 5 year CAGR. The current dividend of just under 5% is well covered with a payout ratio close to the bottom of the long term guidance range,

Seeking Alpha

Valuation.

CTC is not well covered by analysts, so forward looking metrics are not simple to find. Morningstar rates CTC as a 5 star stock with no moat, and a fair value of CAD 340, at a 0.78 price to fair value rating. The stock is not covered by SA Quant.

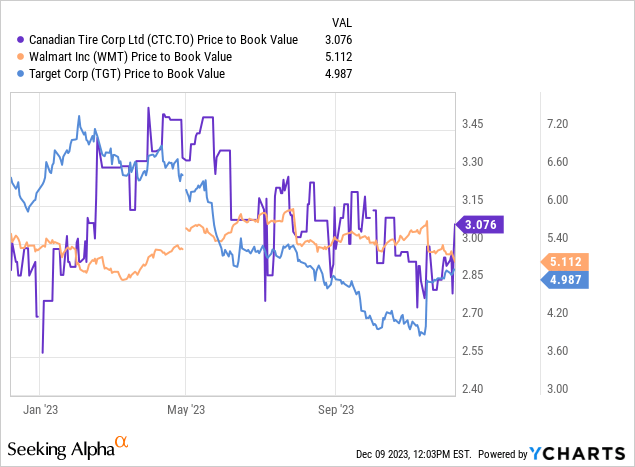

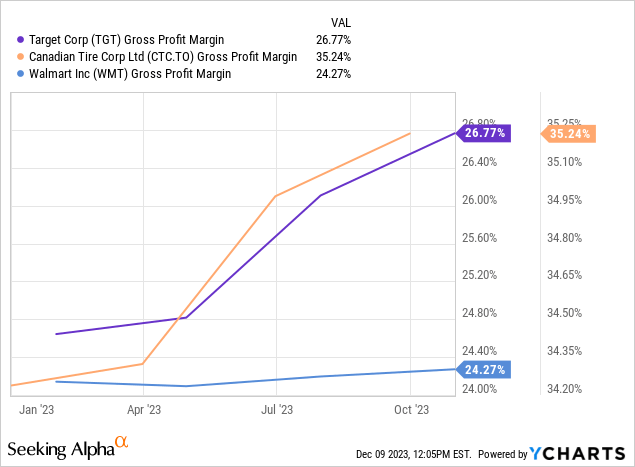

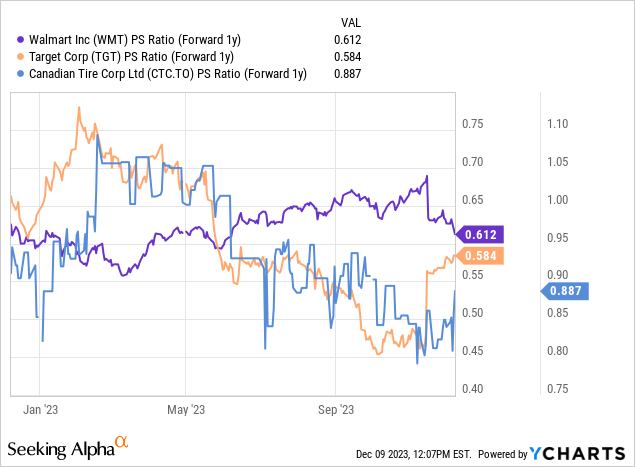

As a competitor comparison I have chosen (WMT) and (TGT) both of which have Canadian operations.

On a price to book basis, CTC shows up well trading at 3 x book vs around 5x for the peers. CTC runs at a higher gross margin, at around 35% compared to around 25% for both peers, and while the price to sales ratio of CTC is higher at 0.9 compared to 0.6 for WMT and TGT, in my view this just reflects the slightly different business profile, and overall valuation seems a wash.

In my view, the Morningstar fair value calculate which has CTC at around 80% of fair value is a reasonable long term FV calculate. I do expect to see margins under pressure in 2024, and don’t see valuation upside next year. In my mind CTC is a hold for current shareholders, and I would be looking for a slightly better entry point in 2024, targeting a dividend yield above 5%. My normal strategy would be to target an entry point using short puts, but CTC does not offer options trading.

Risks

Clearly CTC as a Canada focused company has a high market concentration risk, compounded by a business model which is sensitive to the Canadian economy.

If inflation and interest rates persist longer and higher than current estimates, CTC earnings and cashflow could come under pressure. Given the stable forward debt profile, and low dividend payout, I do not expect to see the dividend under pressure.

CTC does bear some currency and supply chain risk, as much of the inventory is imported.

For Canadian investors, dividends are qualified and taxed at preferential rates. Non Canadian investors will need pay withholding tax, which is withheld at a standard rate of 25%, but reduced for residents of many countries, including the US, where the rate is 15%. PWC supply a comprehensive summary.

Conclusion.

CTC is an iconic Canadian brand, and well supported by the Canadian consumer.

The business is well managed, has a stable balance sheet, and a growing well covered dividend.

Due to economic headwinds, the stock value has reduced from recent highs, and now offers reasonable value at these levels, however, I will look for a slightly better entry point in 2024, targeting a dividend yield above 5%.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")