gorodenkoff

History is written by the victors.” – Winston Churchill.

Today, we are circling back on Aurinia Pharmaceuticals Inc. (NASDAQ:AUPH). Since our last article on this intriguing biopharma name in September, the company has posted better-than-expected Q3 results and there has been some news flow around the firm as well. An updated analysis on Aurinia Pharmaceuticals follows below.

Seeking Alpha

Company Overview:

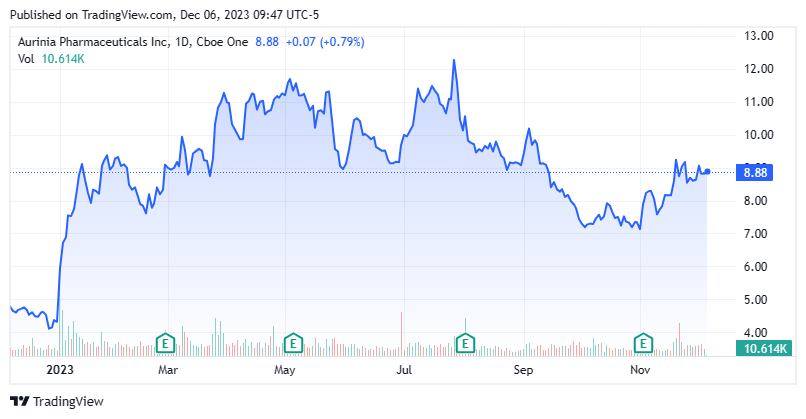

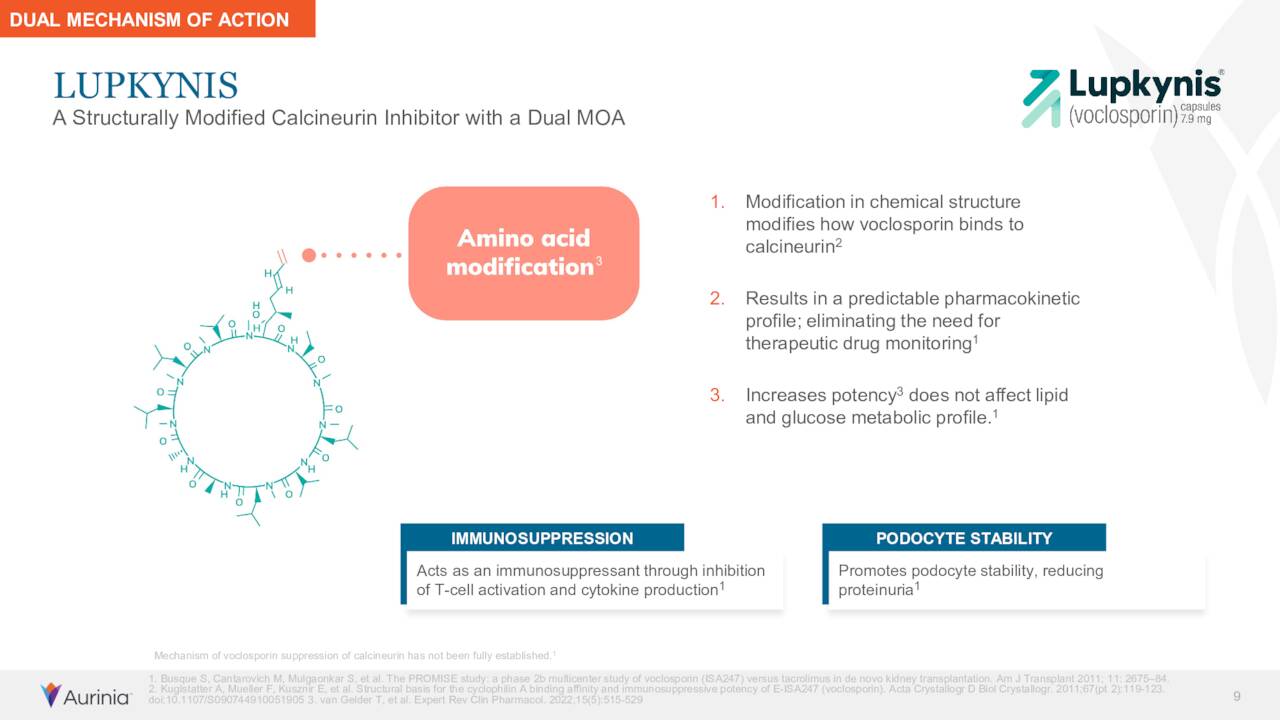

This commercial-stage biopharmaceutical company is headquartered in Victoria, British Columbia. The company’s primary asset is LUPKYNIS, which is also known as voclosporin. This compound is the first FDA-approved oral therapy for lupus nephritis, that was approved in 2021 for this indication. LUPKYNIS annual cost averages $65,000 per patient. The stock currently trades just under nine bucks a share and sports an approximate market capitalization of just south of $1.3 billion.

March Company Presentation

Third Quarter Results:

The company posted its Q3 results on November 2nd. Aurinia delivered a GAAP loss of 9 cents a share, 8 cents a share above expectations. Overall revenues fell slightly from the same period a year ago to $54.5 million. However, that was $16 million better than the consensus. It is also important to note that revenues included a $10 million payment from Aurinia’s marketing partner, outside the United States, Otsuka Pharmaceutical in connection with LUPKYNIS achieving European pricing and reimbursement approvals. Otsuka filed a new drug application in Japan around LUKYNIS on November 13th as well. Approval will net Aurinia another $10 million milestone payout from Otsuka as well as other regulatory/sales milestones and royalties on commercialized sales in Japan.

March Company Presentation

Net product revenue for the quarter was $40.8 million, a large jump from $25.5 million in net product revenue for LUPKYNIS of $25.5 million in the same period a year ago. Net product sales through the first nine months of 2023 came in at $116.2 million, up 55% from the same period in 2022. Leadership narrowed FY2023 net product revenue guidance to $155 million to $160 million from $150 million to $160 million previously. This is also significantly above their initial FY2023 net product revenue guidance, it should be noted.

March Company Presentation

Analyst Commentary & Balance Sheet:

Since third quarter results came out, four analyst firms including TD Cowen and RBC Capital have reissued Buy/Outperform ratings on the stock. Price targets proffered range from $13 to $15 a share. In addition, in late November, Aurinia Pharmaceuticals was again the subject of more takeover speculation. This has happened frequently since the company noted it would look at strategic alternatives in June of this year. At the time, RBC Capital speculated AUPH could be worth $20 to $30 a share in a buyout scenario. Management had this to say about that evaluation on its third quarter earnings call:

We continue to work through the process of reviewing strategic options for the company, which include a variety of possibilities ranging from a potential sale, a merger, or other strategic transaction.”

Approximately 12% of the outstanding float in the shares are currently held short. There has been no insider activity in the stock in more than six months now. The company ended the third quarter with just under $340 million in cash and marketable securities on its balance sheet after posting a net loss of $13.4 million for the third quarter. Management also noted that:

It believes that it has sufficient financial resources to fund its operations, which include funding commercial activities, such as FDA related post approval commitments, manufacturing and packaging of commercial drug supply, funding its supporting commercial infrastructure, advancing its R&D programs and funding its working capital obligations for at least the next few years.”

Aurinia has no long-term debt on its balance sheet and has burned through approximately $50 million worth of cash in the first nine months of 2023.

Verdict:

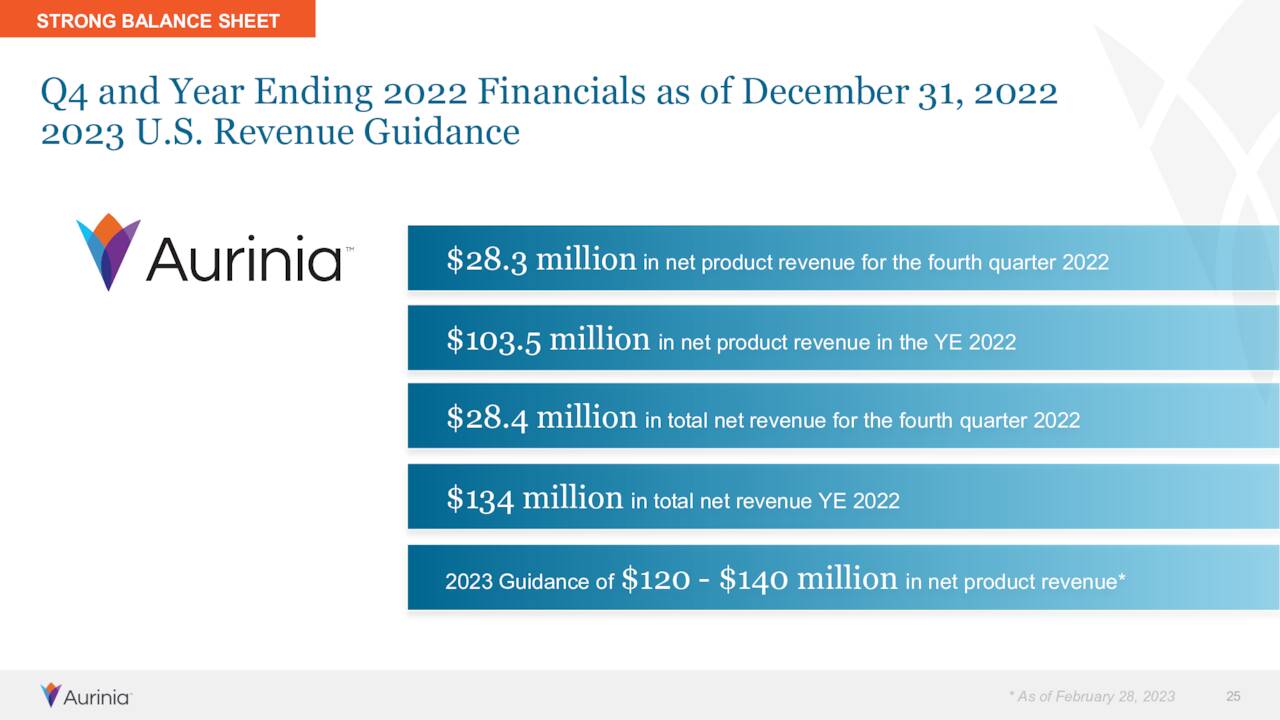

Aurinia Pharmaceuticals lost 76 cents a share on $134 million of revenues in FY2022. The current analyst firm consensus has the firm cutting losses to 52 cents a share in FY2023 as sales rise to just under $175 million. Both top and bottom-line estimates have noticeably improved since we last looked at Aurinia prior to Q3 results. Analyst firms see losses of 37 cents a share in FY2024 as revenues advance up to just north of $212 million.

Since we last looked at Aurinia, the company has posted better than anticipated third quarter numbers and has seen its marketing partner file a marketing application in Japan. Aurinia Pharmaceuticals Inc. continues to savor positive commentary from the analyst firm community and has a strong balance sheet. The stock is up nearly 10% since our last review, but continuing buyout speculation and strong results should continue to put a solid floor under the stock. Capital appreciation seems likely should the company continue to execute well against is goals. Therefore, I will preserve a decent size holding in AUPH via covered call positions.

What is history but a fable agreed upon?” – Napoleon.

Q2 2024 Earnings Call Transcript")