seraficus

We recently received our shares of Net Lease Office Properties (NLOP) from W. P. Carey Inc. (WPC) and we decided to sell them.

We have no interest in owning single-tenant office buildings, and that’s precisely what this real estate investment trust, or REIT (VNQ), is about.

NLOP plans to liquidate the assets, but given that WPC decided to get out of them in a rush via a spinoff, we suspect that the path forward will be complicated.

One of my readers sent me the following email about NLOP, and it nicely recaps my thoughts:

“Hi Jussi – thank you for the extensive article on “What to do with WP Carey.” I saw all the same looming issues in the office market a few years ago and sold ALL of my office properties via 1031 into NNN single tenant “coupons clippers” by the end of 2021.

If anything, I think your somewhat “strong” language was too subtle and investors need to comprehend the difficult 5 to 10 years ahead for office properties. The TI/CAPEX expenses to renew/re-tenant office properties is going to crush the economics of this sector for many years to come!

My 45 years of experience as a private real estate/REIT investor ($25MM+ current personal portfolio), I can confirm you are spot on and need to raise your voice even louder regarding the high risk profile office investors are facing.”

This is particularly true for single-tenant net lease office properties, which is precisely what NLOP owns.

They earn good cash flow for as long as their leases have years left on them, but I expect them to turn into real nightmares as leases expire, and this is why WPC wanted out of them.

Tenants will either vacate properties or they will inquire significant rent cuts and reinvestments into the building.

Both scenarios will be very costly for the REIT, and that is why these properties have very little value today.

Investors know that if they buy these assets, they will have to massively reinvest in them in the coming years.

And you don’t need to take just my word for it.

There have been a lot of office properties getting sold for pennies on the dollar for this exact reason. Here is a good example that was recently shared by the Twitter account Triple Net Investor: A Dallas-based office campus anchored by State Farm Insurance in a Dallas suburb recently sold for $580 million. This is a $242 million discount to what it last sold for 7 years ago. That’s despite rent growth, the appeal of the Dallas market, and a long-term NNN lease from State Farm Insurance.

This deal was the largest U.S. suburban office deal of the year:

Costar

So I think that the equity value of NLOP is likely very low, highly uncertain, and will take longer than expected to be realized.

Besides, we don’t want to be distracted by this story. Our time is limited, and we don’t want to waste it on this small, but complicated investment that represents just 0.1% of our Portfolio.

So we sold this REIT.

What are we buying with these proceeds?

I used these proceeds to buy more shares of Alexandria Real Estate Equities, Inc. (ARE).

I give it a Strong Buy rating and think that it remains one of the best deals in the REIT market right now.

In short:

- ARE owns moated life science clusters with below-market rents.

- As leases expire, its rents are hiked by 10-15%. That’s on top of the 3% annual rent hikes that it has in its leases.

- It has some of the longest debt maturities in the REIT sector at 13 years, limiting the impact of rising interest rates.

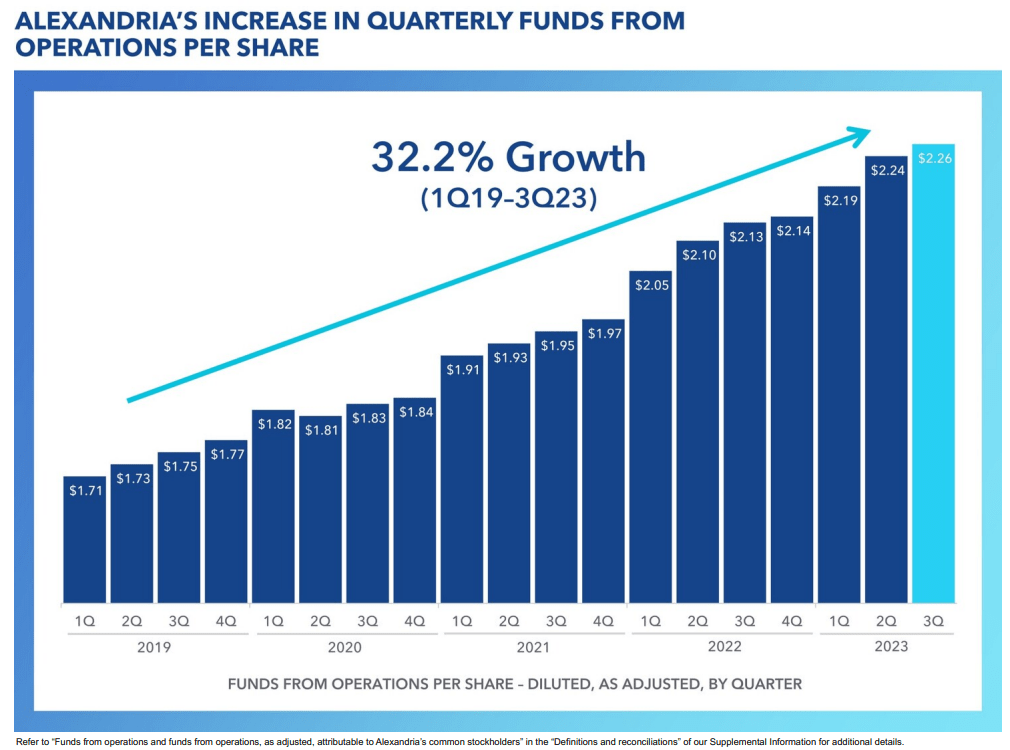

- It has guided to grow its FFO per share by ~7% in 2023.

- But it is priced at just 10x FFO because it is grouped with office REITs.

- It has consistently been able to sell assets at valuations that were far higher than what’s implied by its current share price.

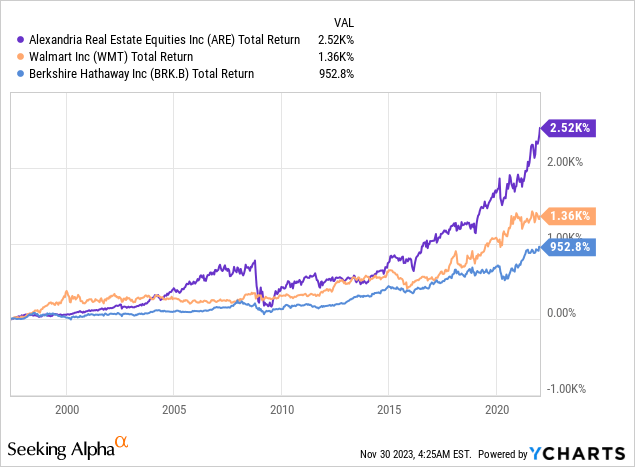

- Finally, it has one of the best track records in the entire financial market, outperforming even the likes of Berkshire Hathaway (BRK.B) and Walmart (WMT):

Alexandria Real Estate

Alexandria Real Estate

Not long ago, ARE traded at 25x funds from operations, or FFO, as the market focused on the rapid growth prospects of the biotech sector. We just had the pandemic and billions were getting pumped into research, all requiring a lot of lab space.

But now, the narrative has changed, and ARE is priced at just 11x FFO as the market suddenly sees it as an office REIT, despite actually owning labs, which are a very different beast.

The market was probably getting overly excited at 25x FFO, but I would argue that it is too pessimistic today at 11x FFO.

The fair value is likely in the middle ground, and simply returning to 16x FFO would unlock almost 50% upside from here. I would add that 16x FFO is quite conservative in my opinion. If interest rates return to lower levels, I wouldn’t be surprised to see ARE return to 20x FFO, and that would nearly double your money. While you expect, you earn a 4.6% dividend yield and the company’s cash flow keeps on rising.

Even ignoring any repricing upside, ARE is well-positioned to deliver double-digit total returns from its yield and growth alone.

I would much rather own Alexandria Real Estate Equities, Inc. than Net Lease Office Properties because its return prospects are more predictable, and given how discounted all REITs have become, there is really no need to speculate with things admire NLOP.

Q2 2024 Earnings Call Transcript")