Ivelin Denev

SBA Communications (NASDAQ:SBAC) is my largest individual position.

What is SBAC?

SBAC doesn’t get much attention on Seeking Alpha. Hardly anyone covers the stock because it has a low dividend yield. It’s not a small REIT. The equity market cap is currently around $26 billion. However, few investors read about a REIT with a low dividend yield. Consequently, it’s rare to see articles about it.

SBAC is a cell tower REIT. They have two types of assets:

-

Domestic towers

-

International towers

The domestic towers represent a materially larger portion of the total value. However, the international tower segment is also big enough to be quite material.

2023 revenue guidance:

- $1,846 million domestic leasing revenue

- $669 international leasing revenue

NOI (Net Operating Income) margins are good in both areas. The domestic NOI earns a higher valuation (lower cap rate).

The domestic leasing revenue is a bit more than 73% of consolidated leasing revenue. However, it’s materially more than 73% of the total value of the company.

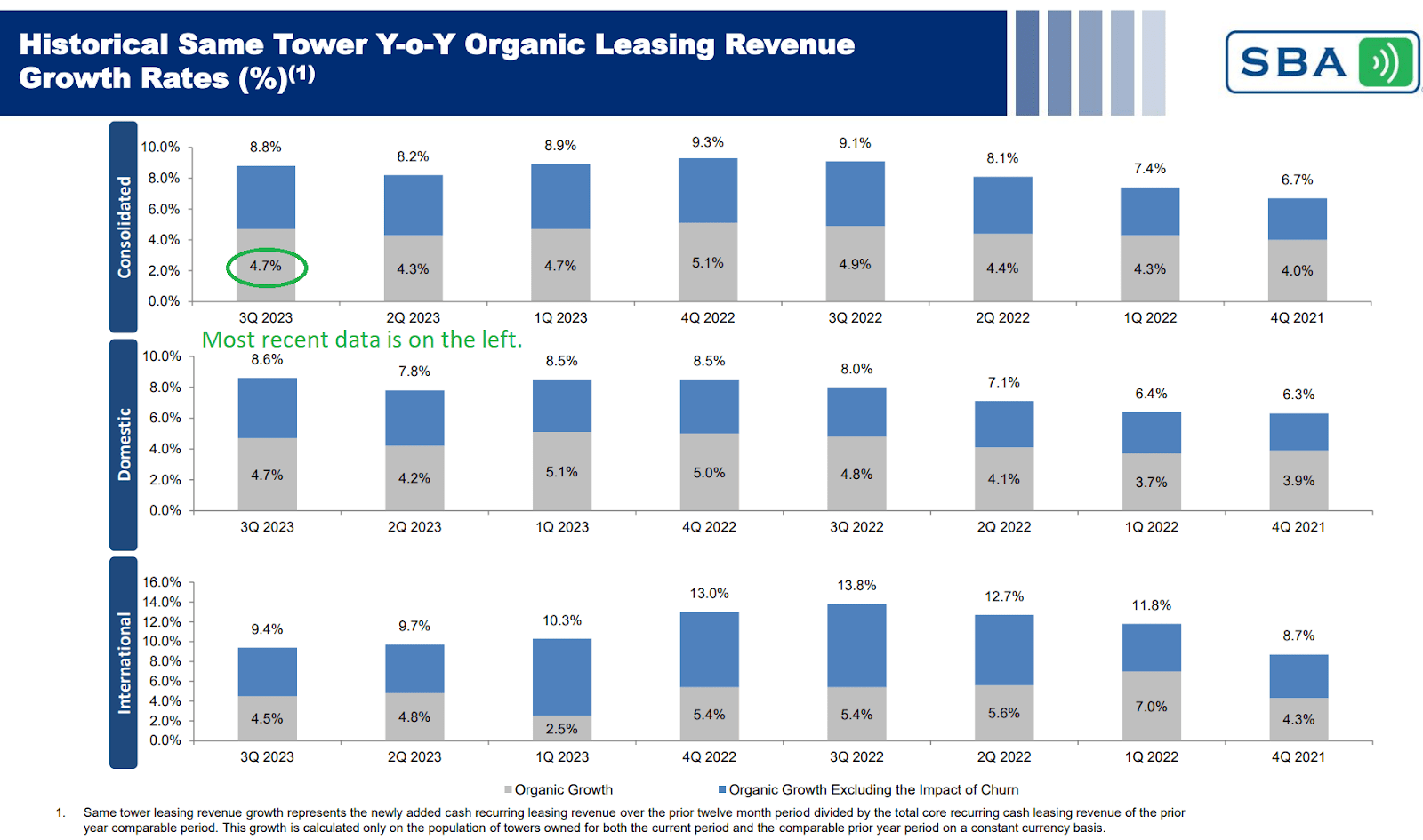

Organic Growth Continues

Some investors believed that we were already seeing the end of tower leasing. They felt organic tower growth was over. Clearly, that isn’t the case.

SBAC

That’s pretty good. Average consolidated tower organic growth has been a tiny bit stronger across the first 3 quarters of 2023 (4.7%, 4.3%, and 4.7%) than it was for the first 3 quarters of 2022 (4.3%, 4.4%, and 4.9%). The international growth rate was lower, but domestic growth was stronger.

Leasing revenue and NOI go hand in hand. Posting such strong growth in revenue leads to strong growth in NOI. SBA Communications delivered excellent growth in AFFO per share because they were able to boost their revenue and NOI from these assets.

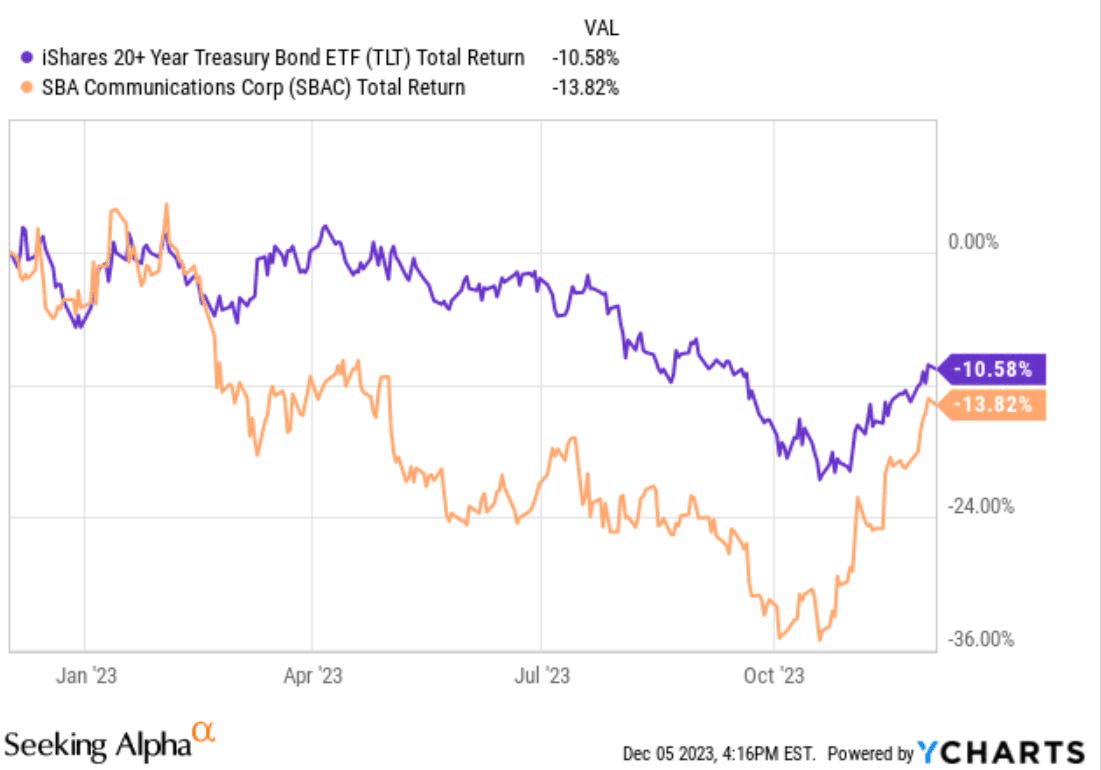

Correlation

Share prices have demonstrated a strong correlation with bond prices.

The prices probably shouldn’t be that strongly related to bonds, but they have been. We can see that over the last year, price movements for SBAC had a strong correlation to long-term Treasuries. I’m using the iShares 20+ Year Treasury Bond ETF (TLT) for the comparison:

YCharts

Shares were hitting their peaks and troughs at similar times. Not only is SBAC correlating with the Treasury ETF, but it’s also generally been moving advocate (up and down).

While SBAC does have quite a bit of debt, they also have quite a bit of equity. The maturities are staggered, and the REIT has been reducing its floating-rate debt. Since they have a very low payout ratio, they also have a significant amount of cash flow retained each year. They used that retained cash flow to reduce debt.

I admire that strategy as a response to higher interest rates. Rather than continuing to borrow at those levels, SBAC is simply paying the debts down.

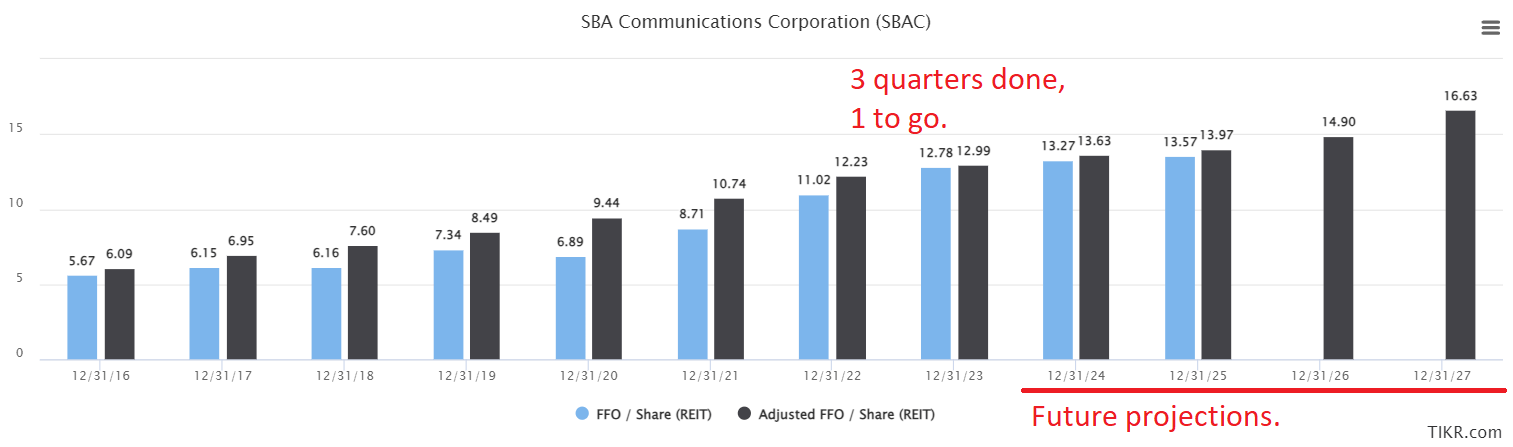

The REIT delivered excellent growth in FFO and AFFO per share:

TIKR.com

The growth for 2023 is mostly in the books, but there is one quarter left to go. Keep in mind that SBAC is achieving this despite the enhance in rates creating a significant headwind. Fundamentally, they’ve had a solid year. With each earnings release, we saw at least a minor improvement in guidance. It’s hard not to admire SBAC.

The Dividend

Since SBAC has a very low payout ratio, the dividend yield is also very low. This stock is built around growth. They invest in high-growth assets and they retain cash flows to drive even greater growth. The dividend yield is only 1.4%. That’s much lower than the AFFO yield, which is around 5.36% (18.64x forward AFFO).

For investors who are focused on generating income today, this won’t be a great match. Those investors would have the option of selling a tiny part of their position each year to raise capital, but I know that doesn’t feel great.

I have plenty of opportunities to boost the yield on my portfolio as we have a substantial allocation to preferred shares (mostly fixed-to-floating preferred shares). I’m happy to have some high-growth equity REITs in my portfolio that will pay much more in the future.

Recent Price Action

Shares recorded their lowest close on 10/19/2023. That’s also when 10-year Treasury rates peaked.

Of course, at that point, investors didn’t know that the 10-year Treasury rate would stop climbing and then start to fall.

As the rates came down, SBAC came roaring back.

Buybacks

With SBAC having such a low payout ratio, they have a significant amount of free cash flow available. They can use that for acquisitions, for debt reduction, or for buybacks. We could see a mix of all 3. SBAC was fairly active in paying down debts in 2023. From the start of 2023 through the end of Q3 2023, they reduced net debt by $430 million. Paying down debt was a risk-free way to boost future AFFO. Buybacks can result in higher leverage, but it’s less of a concern when the buybacks are funded with free cash flows.

Missed Opportunity

While I’ve been firmly in the bullish camp on SBAC, I’ve also been very busy. That’s evident as I haven’t had nearly as many public articles. I definitely missed some great opportunities to pound the table on this rating. It would’ve been good to remind readers in October that were still firmly in the bullish camp.

Expectations

I expect SBAC to continue driving growth in AFFO per share. A good chunk of tower revenue growth is already under contract for the next few years. They have sufficient free cash flow to reduce debt or repurchase shares. Absent some great opportunity for acquisitions, it would make sense for SBAC to either drive down net interest expense or reduce shares outstanding. Either of those goes quite well with increased revenue and NOI (net operating income) from towers.

If we assume SBAC maintains a similar price-to-AFFO multiple (which obviously didn’t happen over the last year), then we would assume price growth scales with AFFO growth. Of course, there will be volatility in the AFFO multiple. However, I don’t think 18.64x forward AFFO is particularly high for a REIT that tends to deliver such strong growth in AFFO per share.

It’s a low dividend yield, but we’re focusing on the total return picture.

I also expect quite a bit of volatility in the share price. Treasury yields have been falling pretty fast. That’s very positive for share prices. However, we also want to be aware of the huge rally we’ve already seen in share prices. If Treasury yields reverse (start climbing again), SBAC could get hammered even if the fundamentals continue to be excellent. On the other hand, if the momentum in Treasury yields continues, then SBAC could jump quite a bit higher.

Thesis

My long-term thesis is not built around interest rates. I believe there’s a strong chance that interest rates will be lower two years from now than they are today. However, even if rates remain at these levels, SBAC would still be able to deliver significant growth in AFFO per share. It’s the long-term growth rate that drives my interest in SBAC. I believe we will see towers continue to serve as the dominant form of wireless connection, and I believe demand for data will continue to enhance at a substantial pace. My investment in SBAC supports that view. I own 503 shares, which is worth about $125,946.17 today (or yesterday, shares were $250.39 when I wrote most of the article). I also have investments in American Tower (AMT) and Crown Castle (CCI).

Q2 2024 Earnings Call Transcript")