GCShutter

The steel business has been a notoriously difficult industry for shareholders over long-periods of time. The industry has proved challenging due to high levels of competition, significant cyclicality, and high capital intensity.

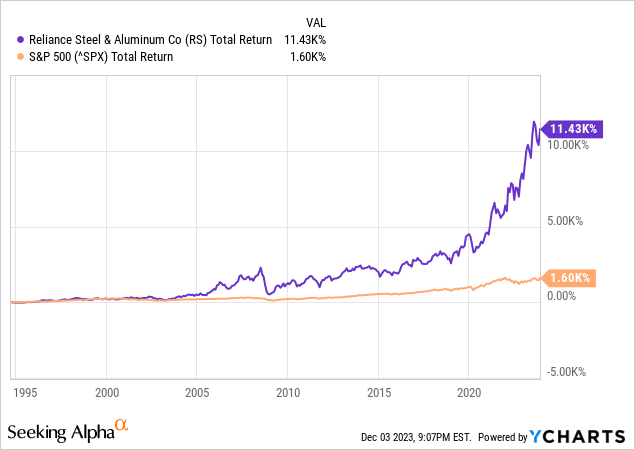

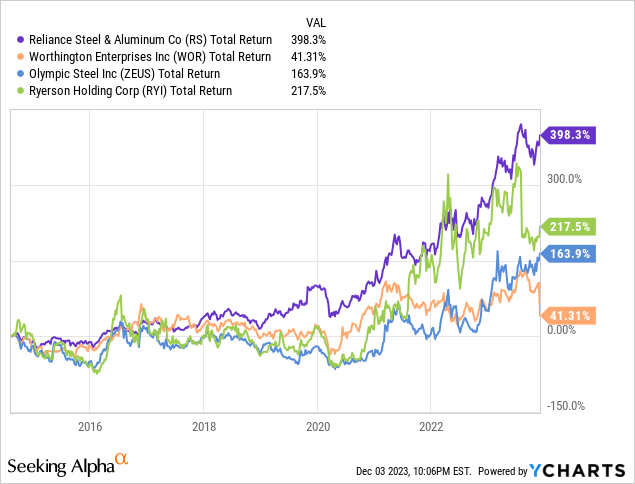

Reliance Steel & Aluminum Co. (NYSE:RS) stands out as having an excellent long-term performance history despite these challenges. Since becoming a public company in 1994, RS has delivered a total return of 11,430% compared to a return of 1,600% delivered by the S&P 500.

While the future is still bright for RS, I believe the valuation is not yet attractive and investors should expect for a pullback before buying the stock.

Largest Metals Service Center Company In North America

RS is the largest metal services company in the U.S. and Canada. The company was founded in 1939 as a single metal service center in California fabricating steel reinforcing bar.

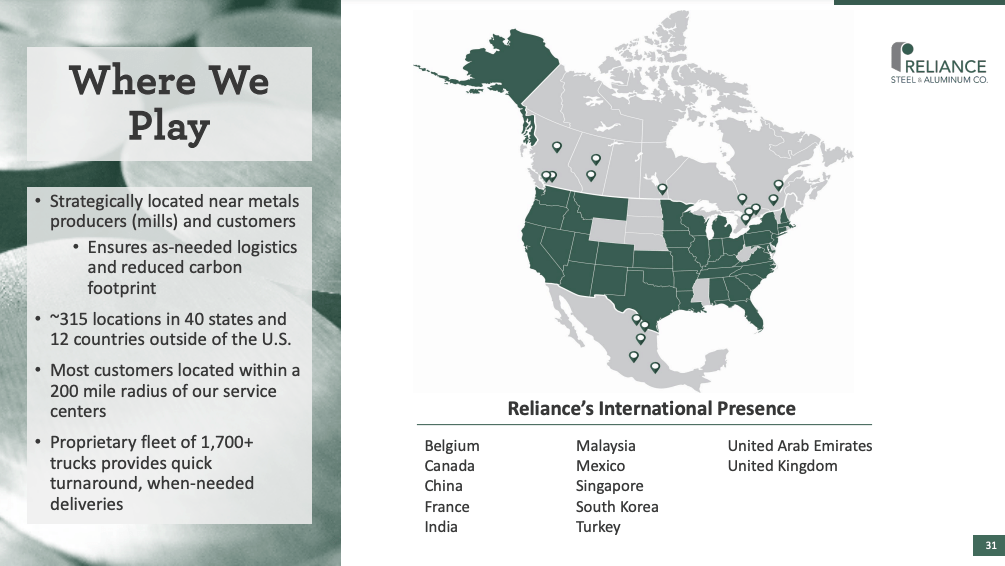

RS has grown steadily throughout its history organically and via acquisitions and now has a network of 315 locations across 40 U.S. states and 12 foreign countries. RS distributes over 100,000 metal products including alloy, copper, carbon steel, stainless, steel, specialty steel, and many other key products.

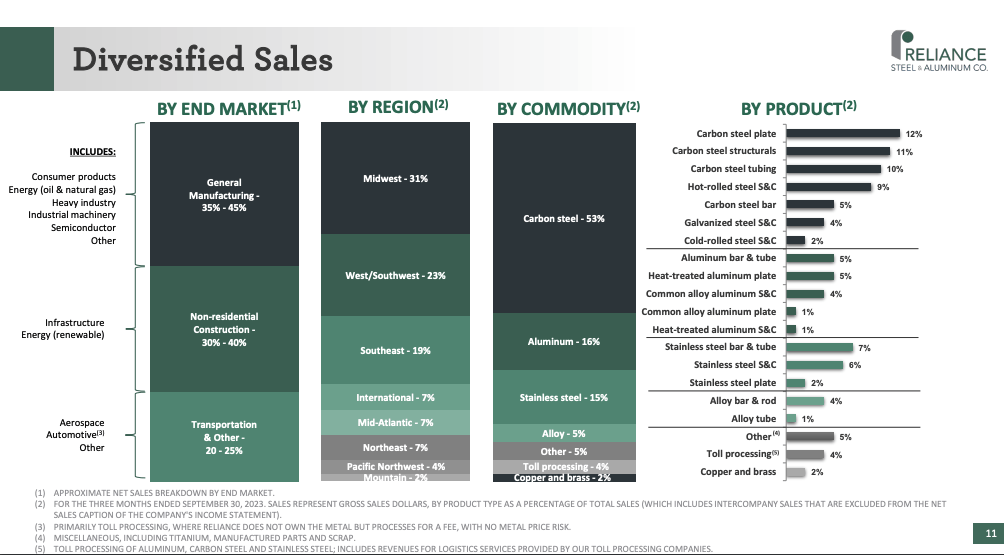

RS is well diversified with no single product accounting for more than 12% of revenue. In terms of break down by commodity, carbon steel represents the largest portion of sales at 53%. Aluminum products account for 16% of sales while Stainless Steel products account for 15% of sales.

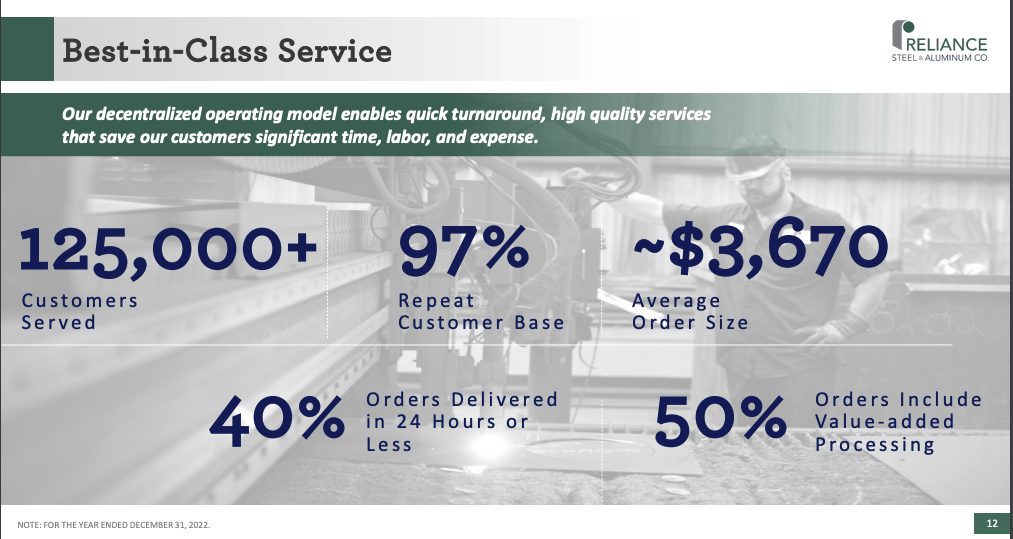

The company serves over 125,000 different customers and 97% of customers are repeat customers.

RS Investor Presentation RS Investor Presentation RS Investor Presentation

Differentiated Operator In A Highly Competitive Industry

The metal services business is highly competitive. It is estimated that there are ~11,200 metal wholesale locations operated by ~8,800 companies in the U.S.

Many of these companies are single stand-alone service centers or regional players. Additionally, RS competes with larger players such as Ryerson Holding Corp (RYI), Worthington Enterprises (WOR), Olympic Steel (ZEUS), and others.

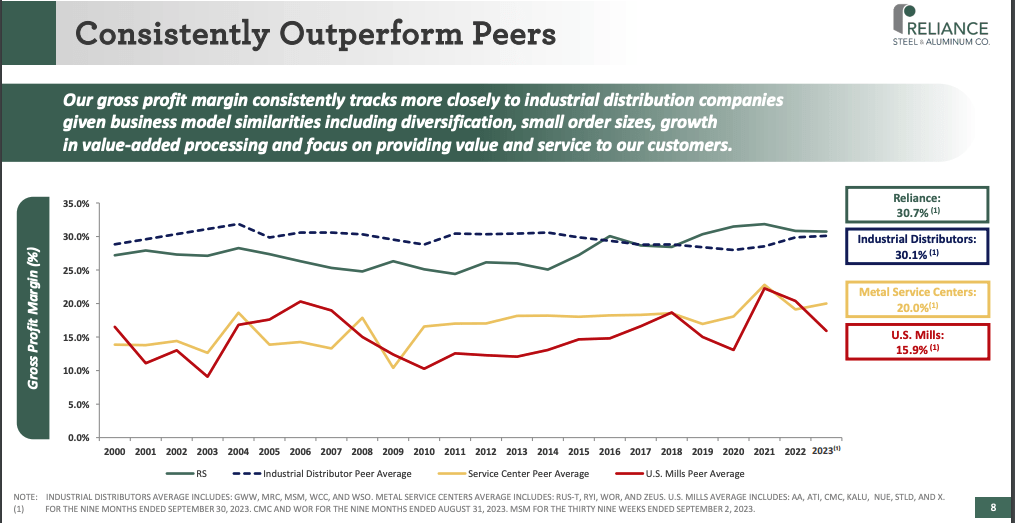

RS’s competitive advantage is driven by its scale. RS is the largest metal services company in North America with ~14.5% market share of all tons sold in the U.S. market. RS is able to leverage its scale and relationships with suppliers to drive better prices and superior product availability compared to smaller players.

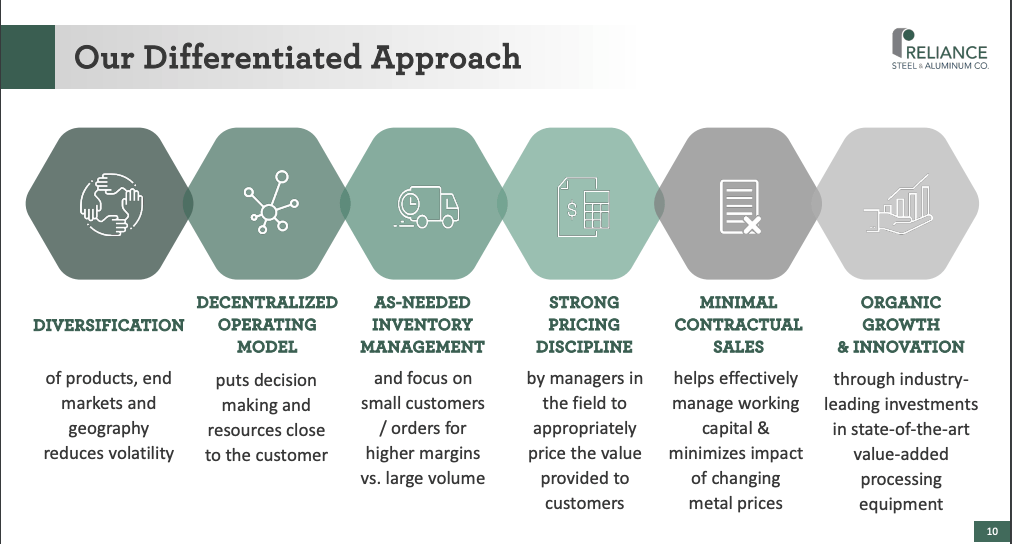

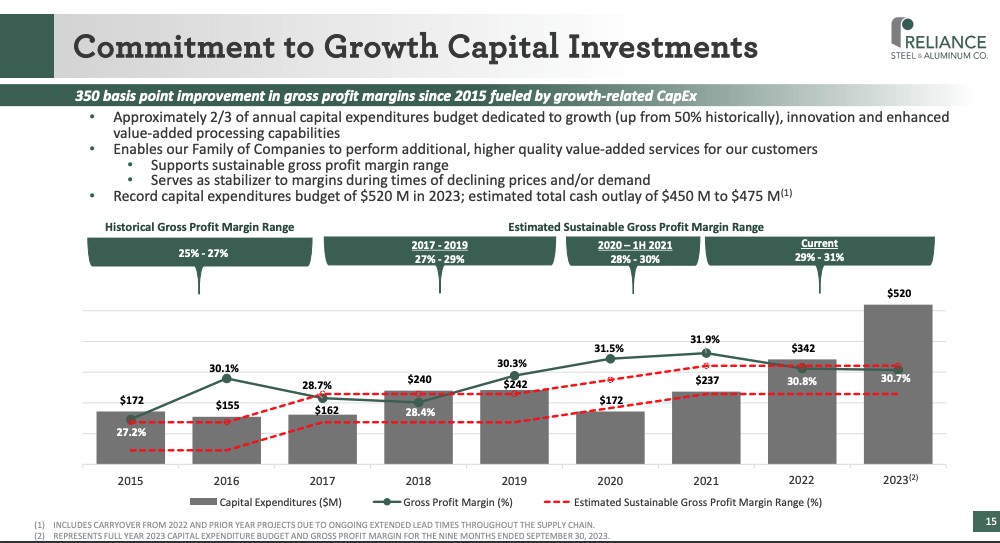

RS also benefits from its significant diversification across products, markets, and geography. Diversification helps to reduce the volatility of RS’s financial performance compared to smaller less diversified players. The result of this is that RS is better able to make necessary investments to boost efficiency throughout economic cycles.

Another way in which RS reduces the volatility of financial performance is by minimizing reliance on contractual sales. This allows RS to minimize the impact related to changing metal prices.

Finally, RS benefits from an as-needed inventory management system and a focus on smaller customers which tend to offer higher margins.

The result of all these factors is that RS has a long history of outperforming peers in terms of profitability and shareholder returns.

RS Investor Presentation RS Investor Presentation

Strong Recent Financial Performance But Signs Of A Slowdown

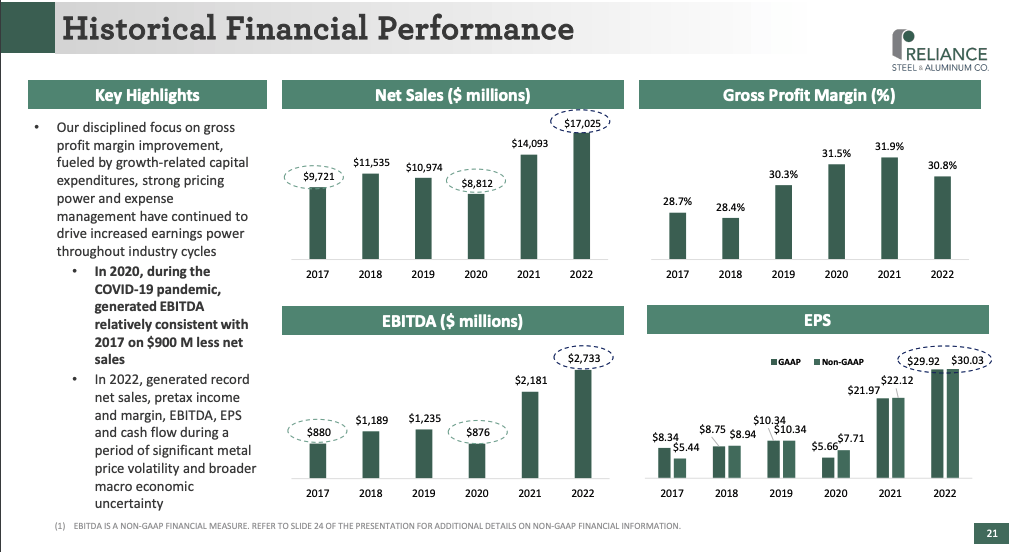

RS has experienced very strong financial performance over the past few years. FY 2022 EPS of $29.92 is nearly triple the company’s 2019 EPS of $10.34. The boost in profitability has been driven by higher net sales and improving gross profit and EBITDA margins.

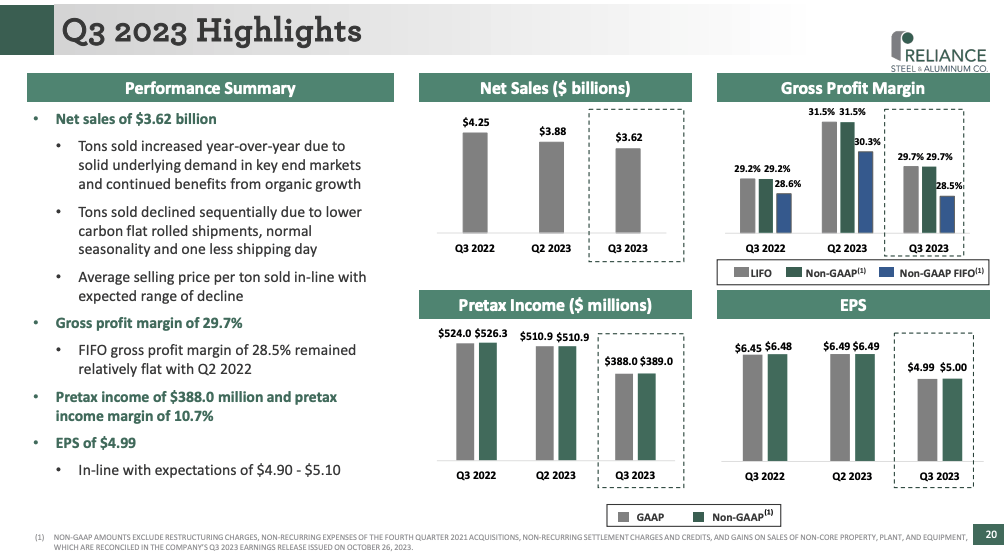

The company recently reported Q3 2023 results which, while strong, represented a reject on a sequential and year-over-year basis. Tons sold increased 3.4% but the average selling price per ton dropped to $2,602 from $2,626 during Q2 2023 and $3,156 a year ago representing respective reject of 2.8% and 17.6%.

RS expects Q4 2023 volume increases in the range of 3.5% to 5.5% compared to the same year ago. However, the company expects average selling price to reject 4%-6% compared to Q3 2023. Additionally, RS expects downward pressure on its gross margins as a result of declining prices. For Q4 2023, RS expects EPS of $3.70 to $3.90 which is inline with current analyst estimates.

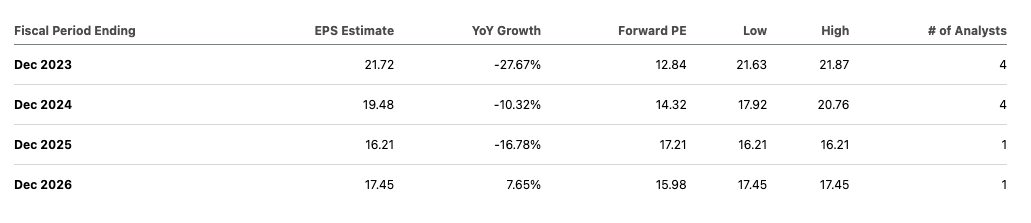

Consensus estimates call for FY 2023 earnings of $21.72 per shares and FY 2024 earnings of $19.48 which suggests market participants expect the recent earnings downtrend to continue over the next year.

RS Investor Presentation RS Investor Presentation RS Investor Presentation

M&A Driven Growth Opportunities

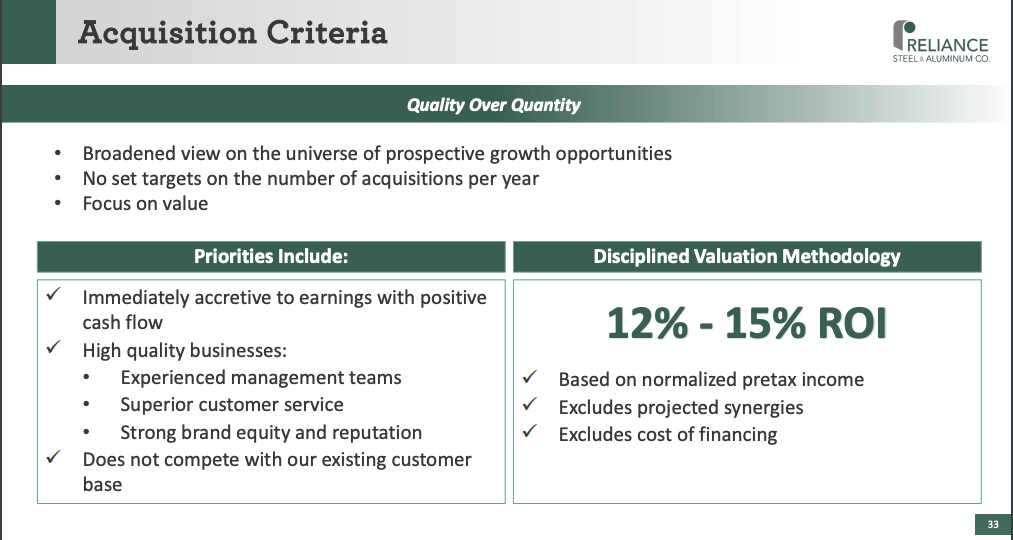

A key part of RS’s long-term growth history has been acquisitions. The company is able to acquire smaller players and improve operational efficiency to drive margin improvement.

Given the highly fragmented nature of the industry (RS is the largest player with just 14.5% market share) I believe RS has substantial M&A driven growth opportunities going forward.

On the Q3 2023 earnings call the company touched on acquisitions:

While we did not complete any acquisitions during the third quarter, the pipeline remains robust. We will follow opportunities that confront our disciplined criteria of well-managed companies that would be complementary to our diversification strategy and immediately accretive to earnings. Our acquisition strategy is supported by our strong balance sheet and consistent ability to produce cash throughout industry cycles.

While it is difficult to forecast when pipeline opportunities will be converted to actual acquisitions, I believe the company will be successful over the long-term in driving advance consolidation of the industry.

RS Investor Presentation

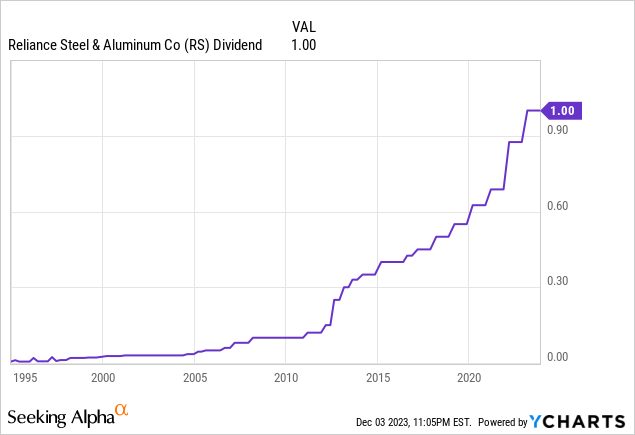

64 Consecutive Years of Dividend Payments

RS is a solid dividend grower having completed 64 straight years of quarterly dividend payments. Moreover, the company has increased its dividend 30 times since its 1994 IPO.

This level of dividend stability is especially impressive given the fact that the company operates in a highly cyclical industry. I view the company’s dividend performance as evidence that its differentiated business model has been able to supply less financial volatility compared to other smaller players.

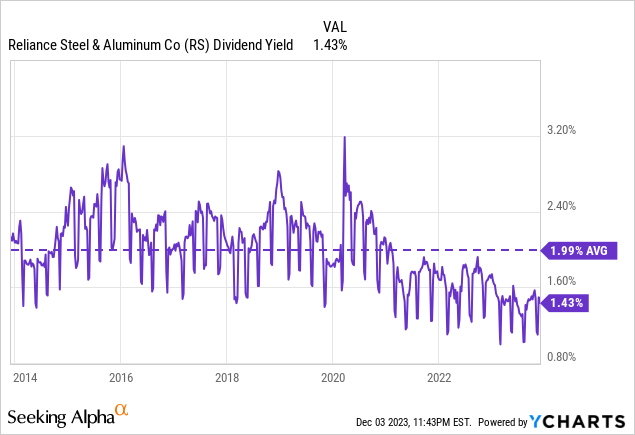

RS currently yields ~1.4% and thus the stock is more of a dividend growth story as opposed to a high yield story. RS’s current yield is below its historical average yield.

Aggressive Share Repurchase Program

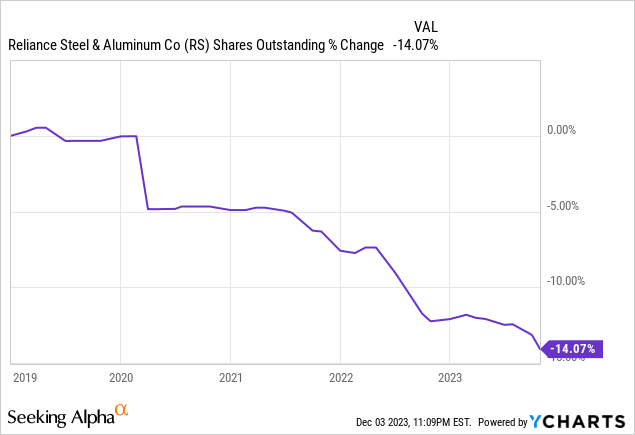

RS has been a consistent repurchaser of its own stock and has reduced its share count by ~14% over the past 5 years.

During Q3 2023, RS repurchased 467,213 shares at an average cost of $270.49 per share. After the end of the quarter, RS repurchased an additional 575,060 shares at an average cost of $255.15.

On October 24, 2023 RS announced that the company’s Board of Directors had approved an amendment to the repurchase program which increased the authorization to $1.5 billion. Based on a current market cap of ~$16 billion, this authorization represents ~9% of the current share count.

I view the company’s commitment to the buyback as a positive signal as it suggests that management views the stock as undervalued.

Strong Balance Sheet

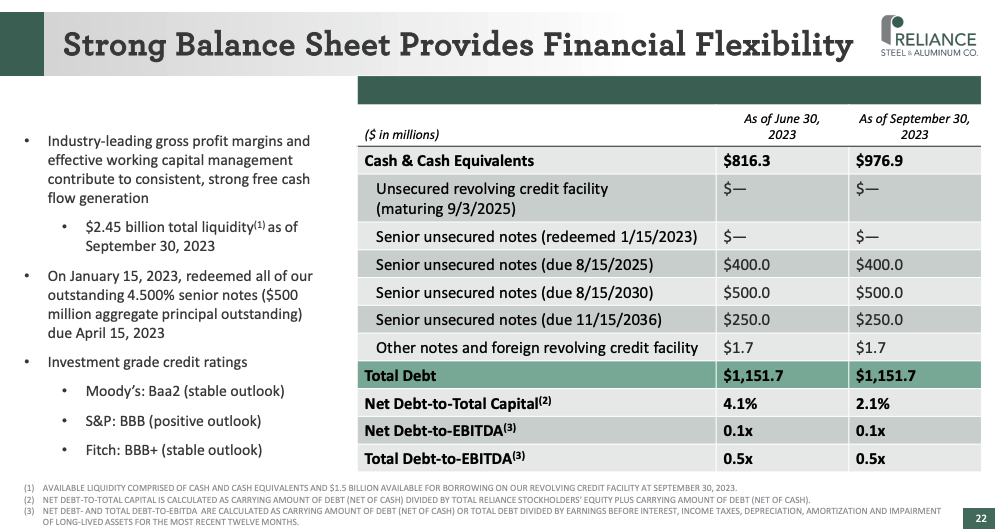

RS has a very strong balance sheet. The company’s net debt to EBITDA is just 0.1x. This is an important strength of the company given the current interest rate environment.

In addition to having a low level of debt, RS also benefits from a relatively long dated maturity structure as the company does not have any maturities prior to August 2025 and the majority of the company’s debt does not come due until 2030 or later.

RS Investor Presentation

Valuation Picture Is Mixed

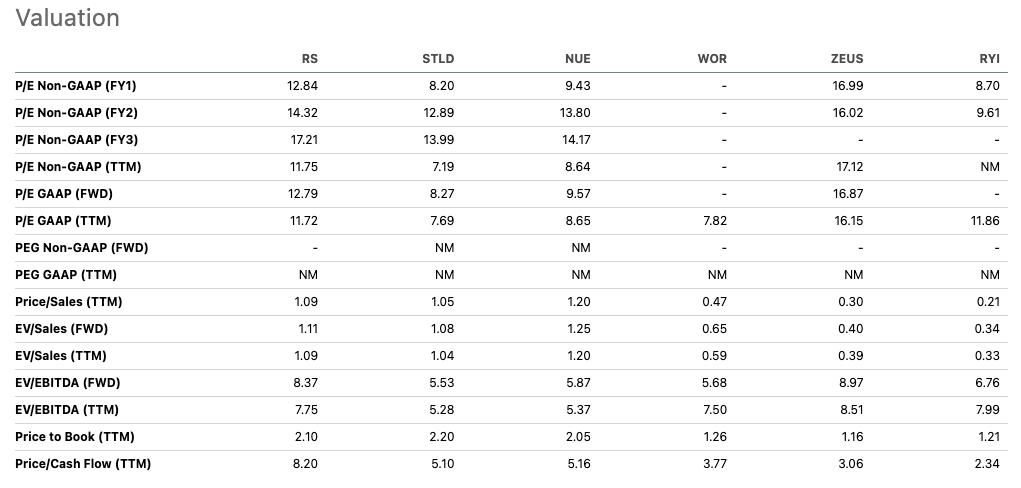

RS is currently trading at 12.8x estimated FY 2023 earnings, 14.3x estimated FY 2024 earnings, and 17.2x estimated FY 2025 earnings. Comparably, the S&P 500 trades at ~18.9x consensus FY 2024 earnings. While RS is clearly trading at a cheaper valuation, it is cheaper because its earning profile is much more volatile than the S&P 500. Additionally, the S&P 500 is expected to grow earnings over the next year by ~12% while RS is expected to experience a 10% drop in earnings.

Despite a high level of earnings volatility, RS has been able to produce above market EPS growth historically having grown EPS at a 10 yr CAGR of 18.4%.

While I am confident that FY 2023 earnings will be inline with expectations, FY 2024 and FY 2025 earnings will be heavily driven by the commodity market environment. If recent macroeconomic headwinds continue, RS could post more severe earnings declines than are currently forecast. On the flip side, RS could post better than expected earnings if the economy is better than expected.

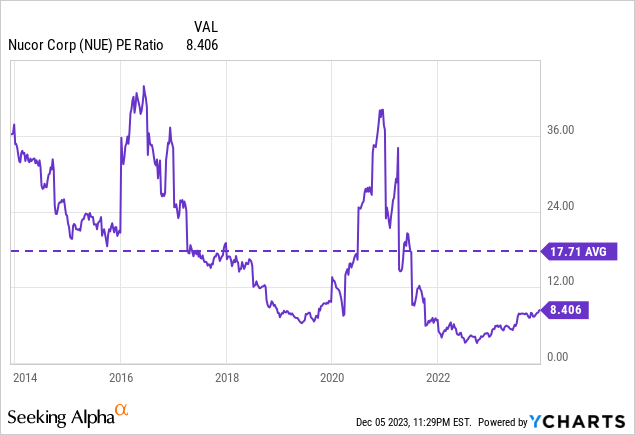

RS is trading toward the higher end of its peer group based on key metrics such as forward P/E ratio and forward EV/ EBITDA. Additionally, RS is trading at a premium to high quality steel producers Nucor and Steel Dynamics.

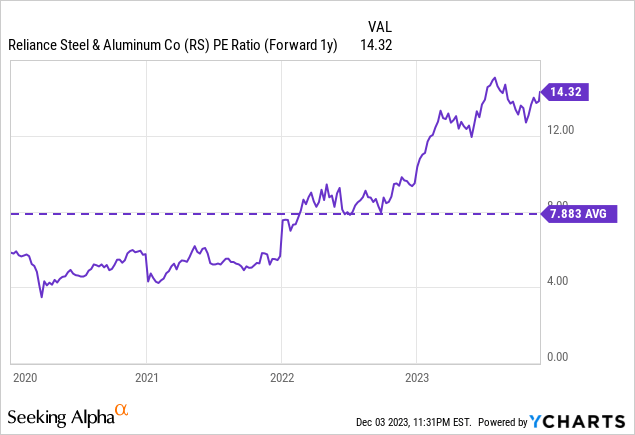

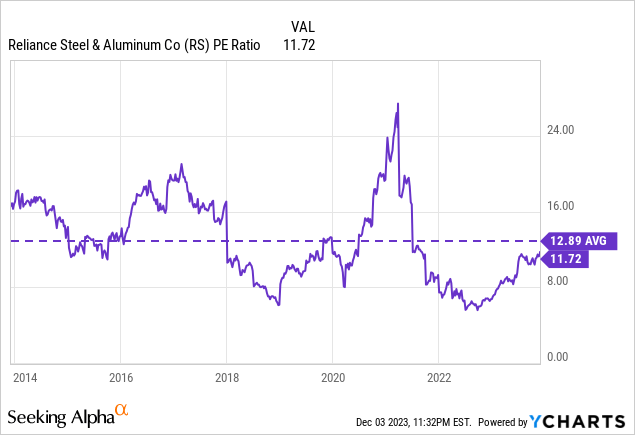

RS is trading toward the upper end of its recent forward earnings historical valuation range while trading close its historical average trailing P/E ratio.

Given these factors, assuming the earnings outlook remains constant, I believe RS would become much more attractive should the stock pull back closer to $251 per share. My $251 level is based off the company’s long-term average historical P/E multiple of 12.9x times expected FY 2024 consensus earnings of $19.48 per share. I do not put as much weight on FY 2025 and FY 2026 estimated earnings as the business is so cyclical that the actual earnings result will likely be materially different. Additionally, I believe RS at a $251 level and forward P/E of 12.9x is much more reasonable valuation vs peers such as NUE and STLD than the current forward P/E of 14.3x.

Seeking Alpha Seeking Alpha

expect For A Pullback Before Buying

RS is a very high quality metal services company. The company is a market leader and has a differentiated business model which has allowed it to build a competitive advantage despite being in a very competitive business.

RS has historically generated very strong financial performance which has led to strong shareholder results.

A key driver of historical growth for the company has been its acquisition strategy. The metal services industry remains highly fragmented and thus I believe RS will continue to benefit from additional acquisitions going forward to drive earnings growth.

The company has experienced very strong financial performance over the past few years driven by significant revenue growth and margin expansion. However, recent results have been somewhat less encouraging given declining end market prices. Consensus estimates currently call for earnings declines on a year-over-year basis for the next two years.

RS has a strong history of paying increasing dividends but the current yield is relatively low relative to its historical average.

RS is currently trading at a fairly high valuation relative to peers. Moreover, the company is also trading at a fairly high valuation relative to its own historical range.

RS is a great company that investors should have on their radar. However, I do not view the current valuation as highly attractive. I am initiating the stock with a hold rating and would consider upgrading my rating in the event that the valuation picture improves.

Q2 2024 Earnings Call Transcript")