JamesBrey

TORM plc (NASDAQ:TRMD) is one of the leading shipping companies active in the product tanker space. It is arguably the highest-quality, best-managed company in the industry, a point that will be discussed later on. Interestingly, TORM is also one of the oldest companies in its field, having been founded in 1889 and first listed on the Copenhagen Stock Exchange in 1905.

A Look at the Fleet

TORM operates a fleet of 84 product tankers, diversified across all major segments: MR, LR1, and LR2. Product tankers are vessels that transport refined oil products such as gasoline, jet fuel, naphtha, and diesel oil. Medium-range (MR) tankers, the smallest in the fleet, offer the highest flexibility for entering ports and covering shorter routes. Long-range tankers, which include LR1 and LR2, have approximately 50% and 100% greater capacities than MR tankers, respectively. The current composition of TORM’s fleet includes 60 MR tankers, 12 LR1, and 12 LR2. However, the company has expressed a desire to enhance its presence in the long-range sector to reach better diversification.

The average construction year of the fleet is 2012, which means that the fleet is nearly 12 years old. This figure is comparable to the average age of the global product tanker fleet. The global fleet is aging significantly, with 9% of tankers over 20 years old. This aging trend is a bullish driver for the company’s future earnings, particularly given the relatively low order book (around 11%, with deliveries through 2027). The typical age for scrapping is around 25 years, which means that TORM’s vessels are, on average, in the middle of their useful life, although TORM tends to divest them around the age of 18. TORM does not have the most modern fleet among listed companies. For example, Scorpio’s fleet is much younger, averaging 7.8 years, as is Hafnia’s, averaging 8.1 years.

The company is aware of the need to modernize its fleet, a necessity that is even more pressing with the upcoming enforcement of stricter environmental regulations. To address this, TORM has been engaged in fleet optimization through selective fleet renewal, which includes some moderate growth. For instance, in 2023, TORM increased its fleet capacity by about 10%. It acquired 22 new vessels and sold seven older ones. The average construction year of the acquired vessels was around 2013, while for the divested vessels it was 2004. One of its most recent transactions involved the purchase of four MR fuel-efficient eco-vessels built between 2015 and 2016. The deal was financed with 60% cash and 40% through the issuance of 2.68 million new shares (approximately a 3% dilution). TORM has utilized its stock to finance deals on three other occasions, leveraging both its premium valuation and higher liquidity compared to peers without access to the US markets.

The modernization effort will necessitate a larger proportion of cash flow in the coming years compared to companies with younger fleets, such as Scorpio’s. However, it appears that TORM is making significant progress in its modernization process, which has not stopped it from distributing substantial dividends in the meantime. As of November, 67 of its vessels (about 80% of its fleet) have been fitted with scrubbers.

Top Quality Management

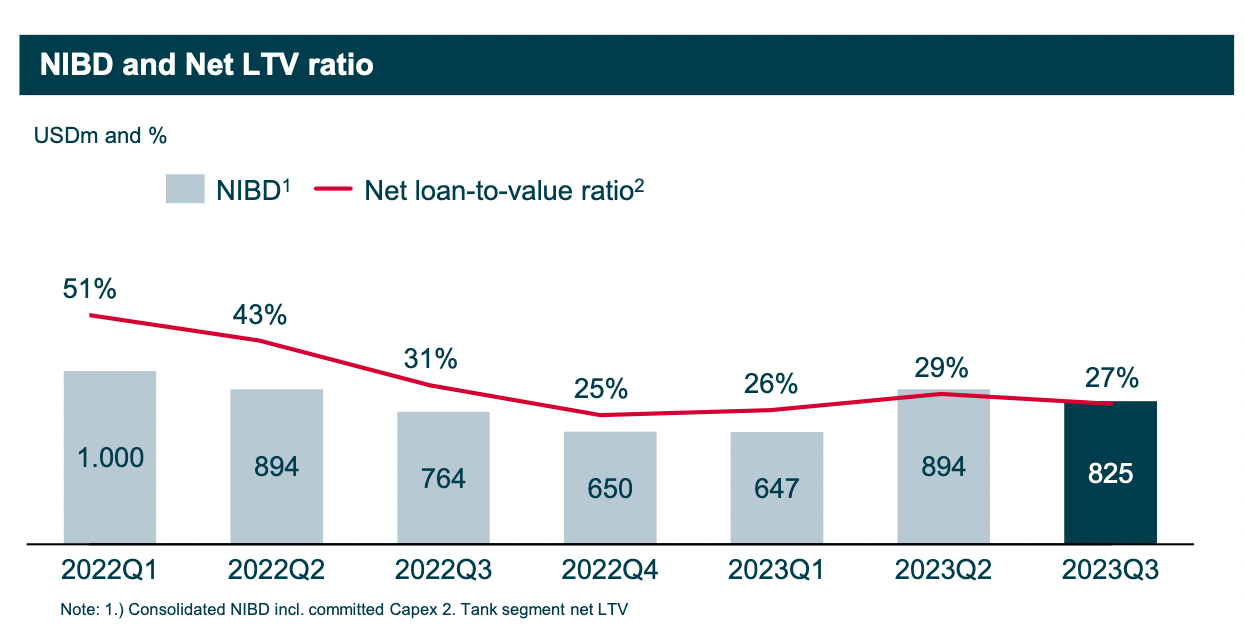

It seems to me that TORM’s management is among the highest-quality in the shipping industry. This is evidenced by their track record of capital allocation and their generous policy of shareholder returns. In recent quarters, even while pursuing moderate growth, the company has avoided taking on excessive debt. In fact, it has been deleveraging its balance sheet (the loan-to-value ratio is now below 30%), while returning the majority of its free cash flow to shareholders.

LTV ratio (Company’s Presentation)

TORM claims to reach “optimal vessel positioning through in-house business intelligence/algorithms.” This might explain why they consistently outperform peers in their Time Charter Equivalent (TCE) rates. For example, they have managed to cover 64% of earning days in Q4 at $38,822 per day (compared to $29,893 for Hafnia, for instance). In Q3, they achieved a TCE of $33,010 per day (Hafnia: $28,954).

Valuation

Quality comes at a price. TORM’s valuation tends to be higher compared to its peers. The superior management and US listing command a premium. Other companies, such as Scorpio, may be cheaper on an absolute basis and offer better value at the moment. However, I am willing to pay more for the peace of mind that comes with having a great management team protecting my interests. I believe that investors in both types of tanker companies will see solid returns over the next few years.

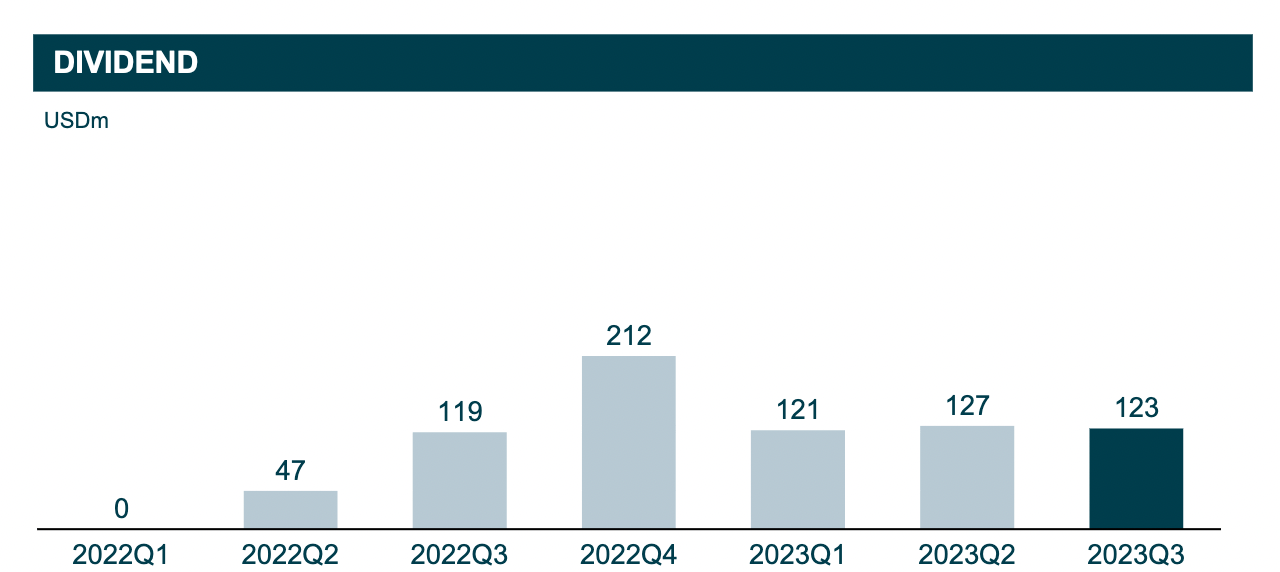

TORM’s market capitalization is around $2.4 billion. Since the beginning of the war in Ukraine in 2022, the company has been paying an average of approximately $125 million in dividends per quarter. Dividends are not subject to withholding tax. If earnings remain at these levels over the next few years, I see no reason why TORM would not continue to pay such dividends. The forward dividend yield would be 20.8%, which is slightly larger, but more or less in line with Hafnia’s.

Dividend payments over last two years (Company’s Presentation)

Oaktree Capital

California-based private equity firm Oaktree Capital Markets holds a controlling 65% stake in TORM. The stock has risen almost 300% since their investment, and they have naturally expressed a desire to sell. After a failed attempt in March, when the stock plunged 13% following the announcement of their intent to sell 5 million shares, Oaktree has recently managed to begin the divestment process by selling 2.8 million shares at the end of November. Oaktree still owns around 50 million shares. It is likely that they will attempt to encourage cash in on these shares in the coming months, which would put downward pressure on the stock price.

Fundamentals of the Tanker Market

I have discussed the fundamentals of the product tanker market in a separate article on Hafnia. Geopolitical tensions following the outbreak of the war in Ukraine have caused a significant enhance in ton-miles and, consequently, freight rates. Low product tanker deliveries and environmental regulations are expected to keep supply in check for the next few years. In the short term, demand should be bolstered by low European diesel stockpiles and the addition of refinery capacity in the Middle East.

Conclusion

While Hafnia remains my main holding in the product tanker space, I have taken a starting position in TORM following the recent sell-off in tankers. It is reasonable to expect that Oaktree will continue its divestment over the next year, which may weigh on the stock price. However, as I scheme to hold my position for the next 2-3 years, the majority of my returns are likely to come from dividends. Sell-off events triggered by announcements of encourage block sales, or by a temporary weakening of charter rates, should furnish opportunities to build a full-sized position. Therefore, while the stock price faces some idiosyncratic headwinds, I believe these same headwinds can offer attractive entry points in the near future. As the company continues to pay out substantial dividends quarterly, the opportunity to buy at a discounted price is not unwelcome.

Q2 2024 Earnings Call Transcript")