bennymarty/iStock via Getty Images

Buying high and selling low is almost never a good idea, and yet many retail and professional investors fall into this trap. While there can be good reasons to call it quits, such as deploying capital into better perceived investment opportunities, it’s equally as important to evaluate one’s original investment thesis and to research whether if said thesis is fundamentally broken before selling.

This brings me to Corning (NYSE:GLW), which I last covered here back in August, highlighting its diverse products portfolio and potential tailwinds from technological advancement in the AI and clean energy sectors. GLW has continued to fall since then, declining by 11% since my last piece, as the market remains focused on near-term challenges, despite improving profitability.

In this article, I furnish an update and converse why GLW remains attractive with the stock trading well below its 52-week high and 15% below where it was 12 months ago, so let’s get started!

GLW Stock (Seeking Alpha)

Why GLW?

Corning is a global leader in materials science when it comes to glass and ceramic science, and optical physics. It has a long 170-year track record of innovation in this space and carries deep manufacturing expertise in products in the mobile consumer electronics, display, automotive, semiconductor, life sciences, and optical communications segments. This includes working with Apple (AAPL) to deliver durable color-infused glass, a first for any smartphone, in the iPhones 15 and 15 Plus.

Corning carries nearly 37,000 patents globally, and its industry-positioning and scale has enabled it to achieve above average EBITDA margin of 20.8%, sitting well above the 9.2% sector median. These factors combined with global demand for its products has produced a total return for GLW that’s surpassed that of the S&P 500 (SPY) for much of the past decade, before recent share price weakness over the past year, as shown below.

GLW vs. SPY Total Return (Seeking Alpha)

One of the core drivers behind the negative market sentiment around GLW is weakness in its optical communications segment, due to lower order rates from carriers admire AT&T (T) and Verizon (VZ), as the ramp for their 5G buildouts is starting to mature. Net sales in GLW’s optical communications was down by 30% YoY during the third quarter, contributing to the 9% refuse in total company net sales.

Despite challenges in GLW’s traditionally largest segment, it’s seeing encouraging growth in display technologies, which is now the largest after growing net sales and net income by 42% and 81% YoY, respectively. This was driven by the popularity of the iPhone 15, which is expected to see a strong holiday season, according to investment advisory firm Wedbush.

Technology in the smartphone market continues to evolve, and this includes the aforementioned color-infused glass and ultra-thin bendable glass, with which Corning announced plans to enlarge capabilities in South Korea for Samsung’s (OTCPK:SSNLF) products. The market may be overly-rotated on GLW’s top-line result, and not so much on its improving profitability (with display technologies being a core driver), as its new smart glass technologies helped to drive a 340 basis point YoY improvement in gross margin to 37% during the last reported quarter. This helped GLW to produce 83% YoY free cash flow growth despite lower sales.

Looking ahead, optical communications is expected to remain weak for GLW in the current fourth quarter and car and TV unit sales are also down as well heading into 2024. However, management noted the cyclical nature of the business during the recent UBS (UBS) global technology conference and expects for consumer demand to bounce back to its upward trajectory in the second half of 2024 as its customers work down inventory.

Meanwhile, GLW carries a strong BBB+ rated balance sheet with a reasonably safe net debt to EBITDA ratio of 2.5x. It’s worth noting that the leverage ratio is somewhat elevated compared to historical norms due to inventory oversupply that plagued GLW this year. Should EBITDA return to 2022 levels, the leverage ratio would be 2.0x. GLW also has one of the longest debt maturities in the S&P 500 (SPY) with an average maturity of 25 years, and no significant debt being due in any given year.

Risks to the thesis include potential for a harder than expected economic landing due to higher interest rates, as GLW is reliant on a healthy level of consumer spending, particularly in its display technologies segment. Moreover, telecom carriers may continue to pull back on their spending should interest rates revert higher, since they would need to focus more on servicing and/or paying down debt in such a scenario.

Nonetheless, it appears that the market has already baked plenty of risks into GLW, as it currently yields 3.9% with a dividend payout ratio of 62%. GLW has raised its dividend consecutively over the past 13 years, and has a 5-year dividend CAGR of 9%. While the quarterly dividend rate was raised by just a nominal $0.01 this year, investors are getting paid to expect while the cyclical nature of the business turns around.

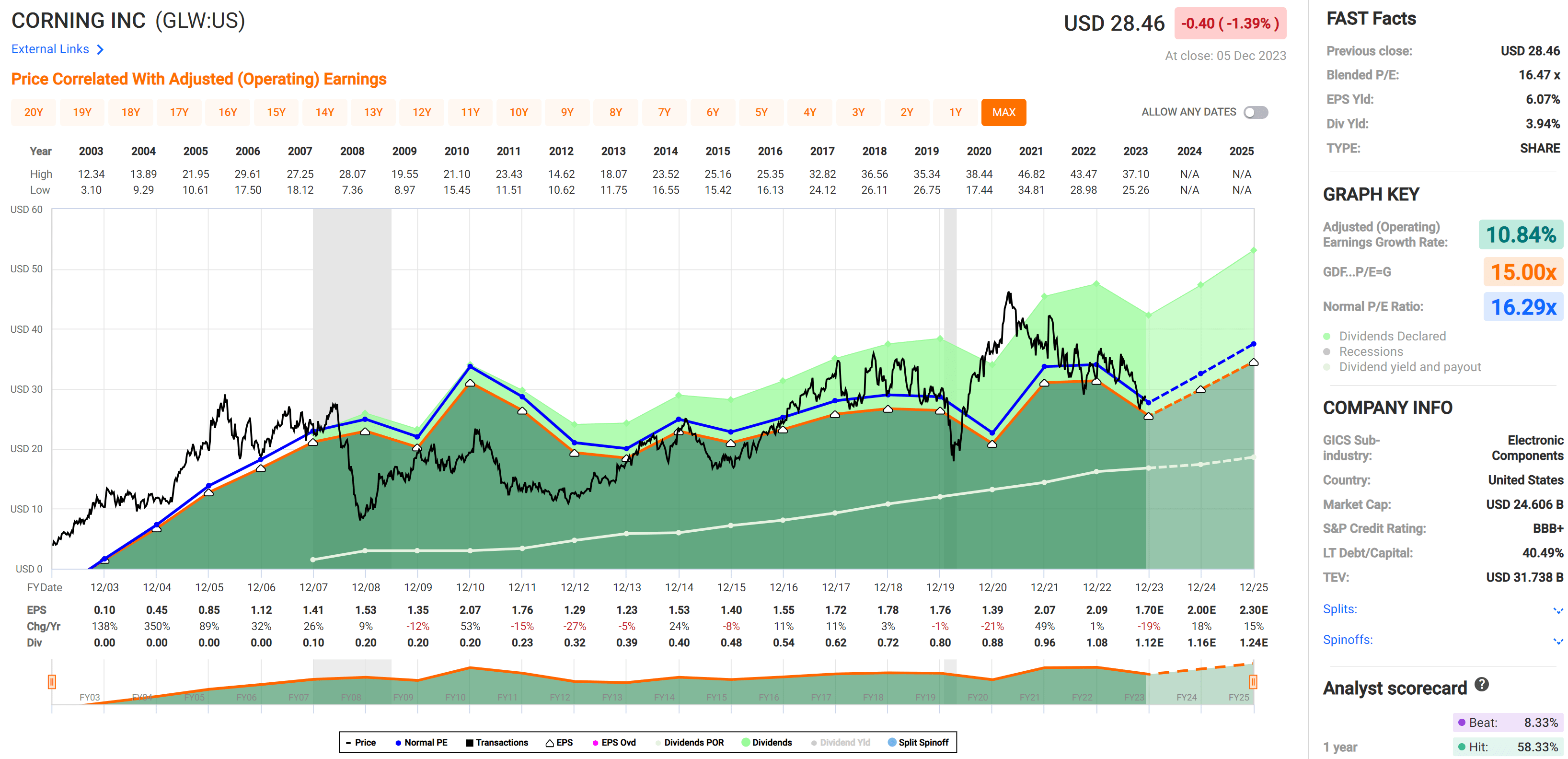

Lastly, I see value in GLW at the current price of $28.46 with a forward PE of 16.9. While this may not seem to be cheap, considering that it sits slightly higher than its normal PE of 16.3, its worth noting that this is more of a function of the earnings refuse this year due to industry oversupply and weakness in optical communications. Analysts expect for earnings to bounce back next year by 18%, and rise by another 18% in 2025, reflecting their confidence in a turnaround. Considering these factors, I believe a price target for GWL in the low to mid-30s is attainable in the near-term, and analysts have an average price target of $32.71.

FAST Graphs

Investor Takeaway

In conclusion, despite the recent challenges faced by Corning, the company remains a strong player in the global glass industry with a solid balance sheet and diversified product portfolio. Its focus on innovation and expansion into new markets, as well as its strong financial position, make it an attractive investment opportunity for long-term investors. Meanwhile, investors get paid a healthy near-4% yield while waiting for the business to potentially turn around next year, after which time I would expect more meaningful dividend growth to resume. As such, I reiterate a ‘Buy’ rating on the stock.

Q2 2024 Earnings Call Transcript")