Alexyz3d

Rocket Pharmaceuticals, Inc. (NASDAQ:RCKT) is a multi-platform clinical-stage biotechnology company based in Cranbury, New Jersey. RCKT focuses on developing gene therapies for rare and life-threatening heart and bone marrow genetic disorders. RCKT’s pipeline has four programs with clinical results for which the FDA granted a Regenerative Medicine Advanced Therapy designation [RMAT]. RP-L201 for severe LAD-I has a PDUFA, and RP-A501 gene therapy for Danon disease is in Phase 1. Still, it already has PRIME (EU), RMAT, Fast Track, Orphan Drug (US), and Rare Pediatric designations. RP-A501 represents a significant commercial opportunity for RCKT, with an estimated $1.3 billion in sales by 2030, which is likely the company’s main selling point as an investment. However, after looking at RCKT’s still early stages research and P/B ratio, its valuation already incorporates its positives. RCKT trades at a premium compared to its peers, making it a “hold” for now but a good buy if it dips back to a P/B ratio comparable to its sector’s P/B multiples.

Business Overview

Rocket Pharmaceuticals, Inc. is a multi-platform biotechnology firm founded in 1999 and currently headquartered in its state-of-the-art Cranbury, New Jersey facility. The company specializes in developing gene therapy treatments for rare, life-threatening genetic childhood disorders focusing on heart and bone marrow. RCKT uses adeno-associated viral vector [AAV] and lentiviral vector [LVV] platforms to address the root causes of such diseases. However, its RCKT hasn’t yet commercialized or fully developed IP portfolios and has yet to make meaningful revenues. Its product pipeline has research projects in clinical trials in Phase 1 and Phase 2.

Source: Form 10-Q, November 2023.

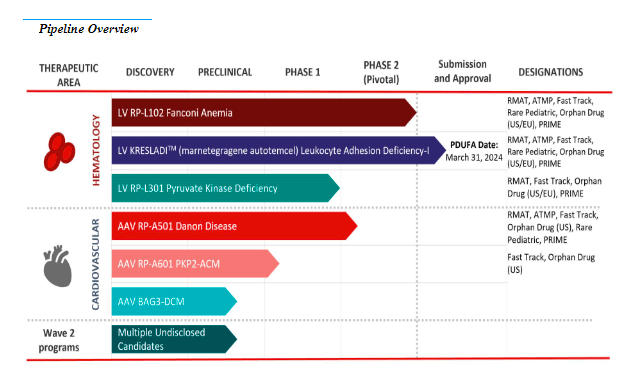

Concretely, RCKT’s product pipeline includes six known products: three for hematology and three for heart disorders. In hematology, they have the LV RP-L102 drug for Fanconi Anemia [FA], which is in the submission and approval phase, and LV RP-L201 for Leukocyte Adhesion Deficiency-I [LAD-I], which is finalizing clinical trial phase 2. Also, the LV RP-L301 therapy for Pyruvate Kinase Deficiency [PKD] in phase 1. In the cardiovascular therapeutic area, they have one therapy in phase 1, the adeno-associated virus AAV RP-A501 for Danon Disease, and two more in the preclinical stage: AAV RP-A601 for PKP2 arrhythmogenic cardiomyopathy [ACM] and another for AAV BAG3-associated dilated cardiomyopathy [DCM]. The company has achieved regulatory milestones such as Regenerative Medicine Advanced Therapy designation [RMAT] for all RCKT programs with clinical data. Additionally, on September 13, the FDA filed a Biologics License Application [BLA] with Priority Review for RP-L201 for severe LAD-I. The FDA is expected to announce its decision before March 31, 2024.

Source: Rocket Corporate Presentation, September 2023.

RCKT develops gene therapies using in vivo and ex vivo platforms to correct genetic disorders by directly delivering a therapeutic gene copy to the affected cells. With the in vivo platform, the AAV vector is introduced into the patient for Danon Disease, PKP2-ACM, and BAG3-DCM. In the ex vivo approach, the patient’s hematopoietic stem cells [HSCs] are removed, modified in the laboratory with an LVV, and reinserted into the patient. This method is used in the hematology therapeutic area for FA, LAD-I, and PKD disorders. This methodology is cutting-edge in gene therapy and is a promising approach with potentially transformative and effective results.

The Promising Future of Rocket’s RP-A501 in Treating Danon Disease

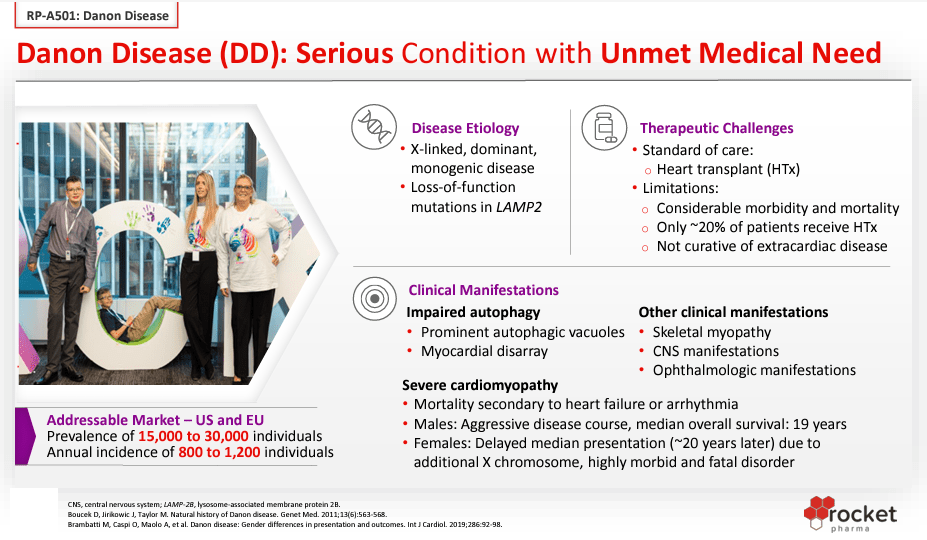

Analysts recognize the importance of the gene therapies RP-L201 for LAD-I, which is already under FDA review, and RP-L102 for FA. However, the treatment with the greatest commercial potential is RP-A501 for Danon disease because the forecast is that sales of this gene therapy will be greater than $1.3 billion by 2030. RP-A501 is expected to gain FDA approval in 2026.

Danon disease is a hereditary disorder that affects the heart. There are approximately 15,000 to 30,000 Danon disease patients in the US and Europe. Presently, it does not have any other treatment than cardiac transplantation. In May 2023, based on the clinical trial Phase 1 results, the RP-A501 gene therapy was accredited Priority Medicines [PRIME] designation by the European Medicines Agency [EMA] for treating Danon disease. This denomination underscores the advantages that these therapeutics present over existing treatment options. PRIME designation offers early uphold for developing medicines and the opportunity for an accelerated review of marketing applications. RP-A501 also has RMAT, Fast Track, Orphan Drug (US), and Rare Pediatric designations.

Source: Rocket Corporate Presentation, September 2023.

Danon Disease is a particularly exciting opportunity for RCKT because of the lack of treatment and severity. As a research project, RCKT could overcome a tragic disease. From an investment perspective, this also puts RCKT in a promising position because it can potentially restore cardiac function, ostensibly giving RCKT commanding pricing power in the marketplace once it’s commercialized. This suggests that the company’s IP in this disease will likely be a high-margin product.

Danon Disease is estimated to affect roughly 15,000 to 30,000 people in the US and EU. Likewise, Fanconi Anemia is estimated to affect 1 out of every 160,000 people. With that data, I calculate that in the US and EU, there are roughly 4,867 people with Fanconi Anemia. This is a markedly smaller patient base than Danon Disease, but RCKT’s research program is advance along the FDA’s approval roadmap. RCKT’s FA research project has completed its Phase 2 clinical trials, according to the company’s latest 10-Q. Thus, I believe These two research projects are RCKT’s most promising.

Baked-In: Valuation Analysis

However, from a valuation angle, it’s worth noting that RCKT’s products target rare diseases. This caps their TAM, which is their main weakness as a business. Naturally, this also likely gives them a commanding position in these niches, as no alternative treatments would contend with RCKT’s IP. Also, I imagine the company would have enough pricing power to give it reasonably good margins. Furthermore, neither of these research projects is in Phase 3, meaning RCKT is still far from generating revenues from its research.

Author’s elaboration.

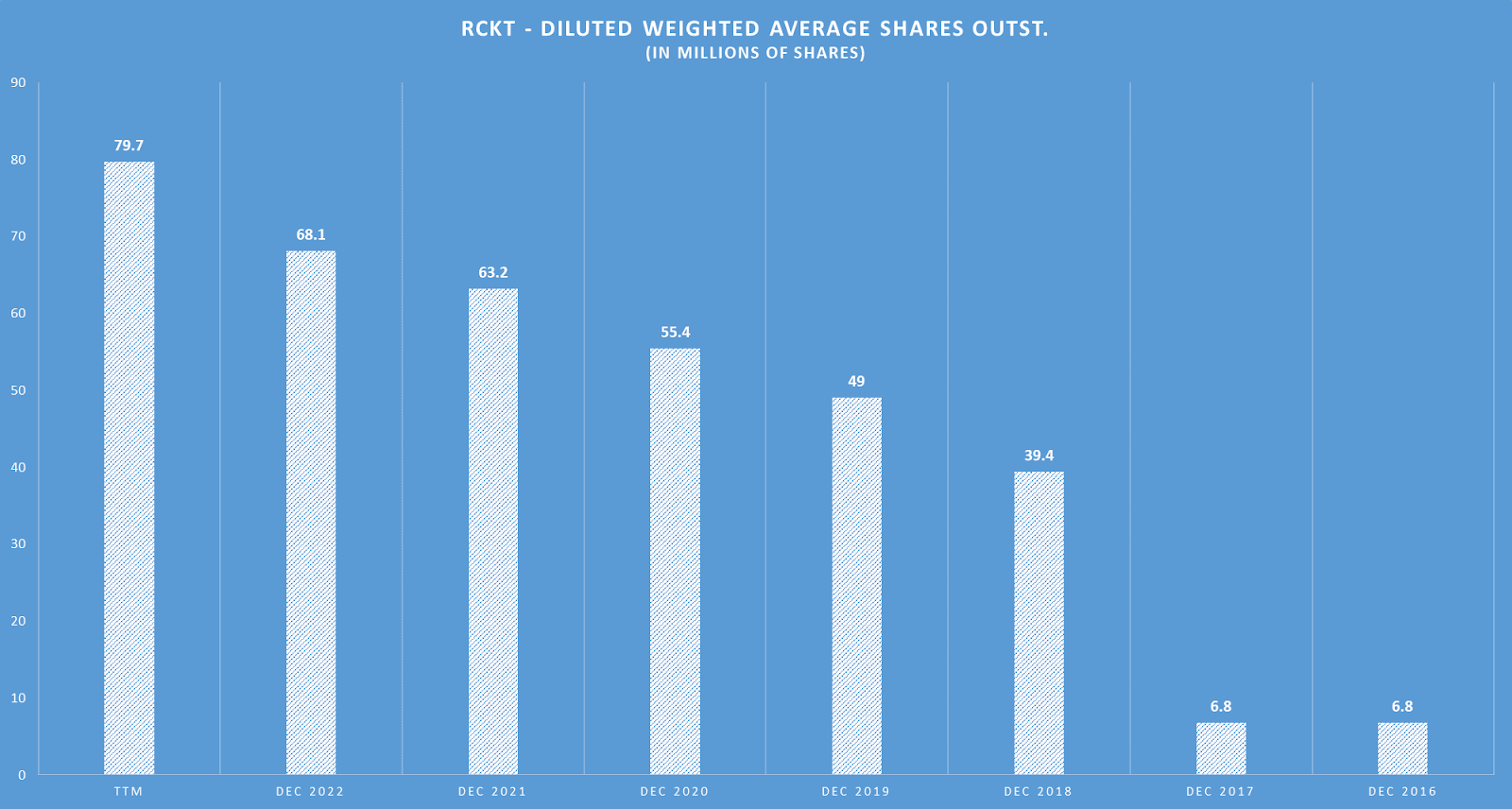

Also, since RCKT has no revenues, our next best valuation approach is multiples. In particular, RCKT’s balance sheet currently has $437.2 million in cash, with just $25.2 million in debt. However, RCKT’s latest quarterly cash flow from operations was $ 57.1 million with a net CAPEX of $ 4.7 million, which I calculate to be a quarterly cash burn of $61.8 million. If we annualize that figure, that implies a yearly cash burn rate of $247.2 million. Thus, juxtaposed against its cash reserves, the latest quarterly cash burn suggests a cash runway of 1.77 years. This is not a terrible figure, but given that RCKT still has no project in Phase 3 trials, I think it’s likely that RCKT might raise additional funds down the road. For context, since 2016, RCKT’s diluted share count has increased from 6.8 million to 79.7 million in their latest report. This means the total diluted shares have increased at an annual CAGR of 42.14%, which points to significant shareholder dilution over time.

Yet, despite the notable lack of revenue, RCKT trades at a $2.11 billion valuation. This surprised me as the IP is still years from being FDA-approved, and the company has yet to license any of its IP. If we look at the company’s book value, RCKT currently has $541.1 million in equity, which implies a P/B ratio of 3.90. This is almost twice as much as the sector’s TTM P/B ratio of 2.05, and recollect that RCKT is burning $247.2 million per year (45.7% of its book value). Thus, I’d argue that RCKT appears slightly expensive, and coupled with the long road to eventual FDA approval, it leads me to rate RCKT a “hold” at this juncture.

RCKT has been historically significantly volatile. TradingView.

Conclusion

RCKT is a promising company addressing relatively rare diseases with innovative AAV and LVV approaches. However, its research is still very much in the early stages, and its target market is fairly niche due to the rarity of the diseases it addresses. Moreover, RCKT appears to already trade at a premium compared to the rest of its sector. Thus, as a whole, it’s difficult to argue that RCKT is cheap, especially after considering its long history of shareholder dilution. Yet, I remain optimistic about its product pipeline over the long term. I think RCKT has the potential to be a good investment, particularly as time passes and it successfully develops its IP. However, I believe RCKT is better to add to your watchlist than your portfolio. Hence, I rate RCKT a “hold” but a good buy on dips that bring its P/B ratio in line with the rest of the sector.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")