deepblue4you

Business Overview

Founded in Florida in 1969, Dycom Industries, Inc. (NYSE:DY) has evolved into a major player in the US telecommunication industry. It offers specialized services to the telecommunications and utility sectors in the United States.

The company’s services are categorized into two segments.

Engineering services: It encompasses planning, designing, and project management for both wired and wireless cable systems.

Construction, maintenance, and installation services: It involves tasks such as fiber and cable placement, trench excavation, and facility maintenance. These services cater to telephone companies and cable operators alike.

Essentially, DY operates as a versatile one-stop shop, providing expertise and labor for telecommunications and utility companies across the nation.

The company predominantly caters to major telecommunication customers, including AT&T (T), Verizon (VZ), Lumen Technologies (LUMN), Comcast (CMCSA), and others. In addition to telecommunication customers, the company also derives ~10% of its revenue from utility companies. This revenue is generated through long-term contracts secured via competitive bidding or occasional extensions of prior service contracts.

Financial Analysis and Outlook

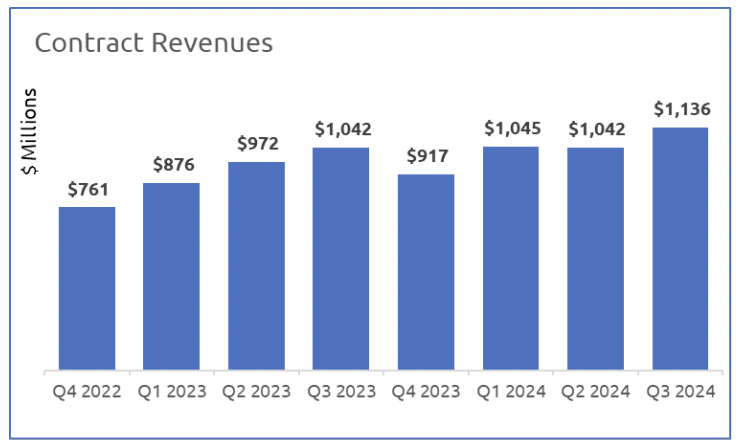

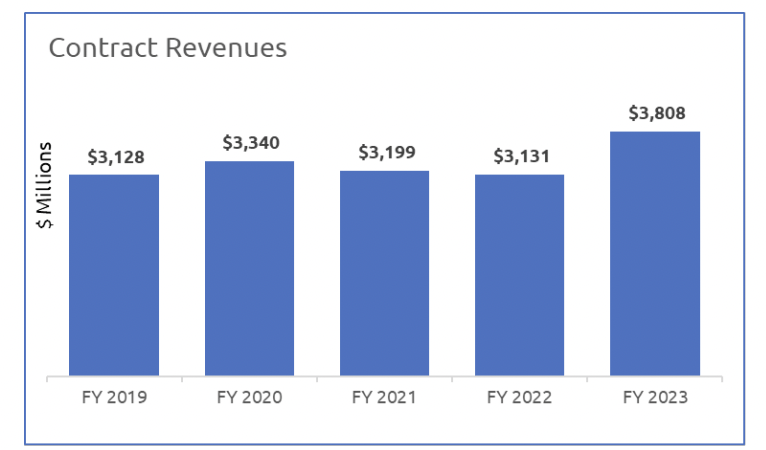

In FY23 (ending in January 2023), the company reported robust year-over-year (YoY) organic revenue growth of 21.4%, reaching $3.8 billion. This surge in revenue was primarily attributed to the alleviation of supply chain constraints, leading to an acceleration in backlog conversion.

The momentum in growth persisted throughout all three-quarters of FY24; however, the YoY organic revenue growth displayed a sequential slowdown over the year. Specifically, the company reported YoY organic revenue growth rates of 19.1%, 7.1%, and 4.6% for the first, second, and third quarters, respectively. The diminishing growth trajectory can be attributed to challenging comparisons with the preceding year which resulted from the supply chain easing experienced during that period.

Quarterly revenue data (Company presentation) Annual revenue data (Company presentation)

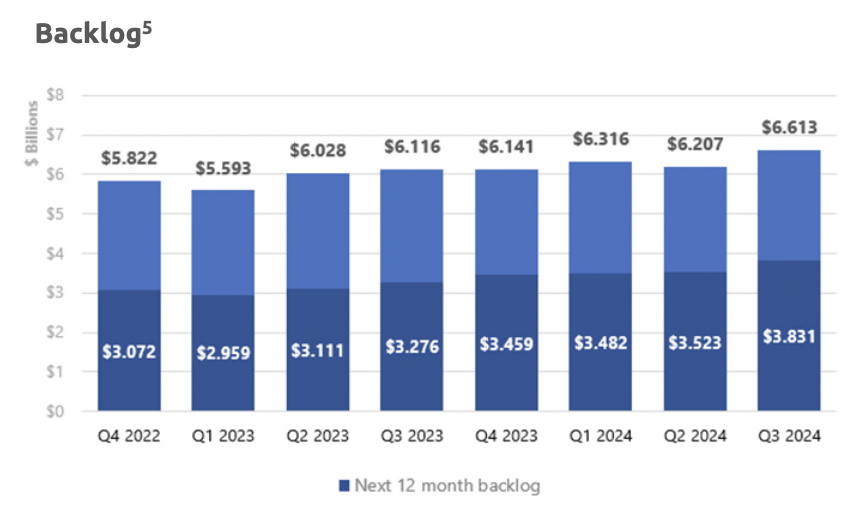

Nevertheless, the strength of underlying demand became apparent, as reflected in the increasing backlog figure, which reached an all-time high of $6.61 billion, marking an 8.12% YoY enhance. Within this $6.61 billion backlog, an anticipated $3.83 billion is expected to be realized in the coming 12 months.

Company presentation.

Looking ahead, I foresee that the company may experience somewhat subdued growth in 4Q24, largely attributed to challenging year-over-year comparisons from the previous year. However, the recent acquisition of Brigham Cable Construction is poised to contribute approximately $50 million to the topline in the upcoming quarter.

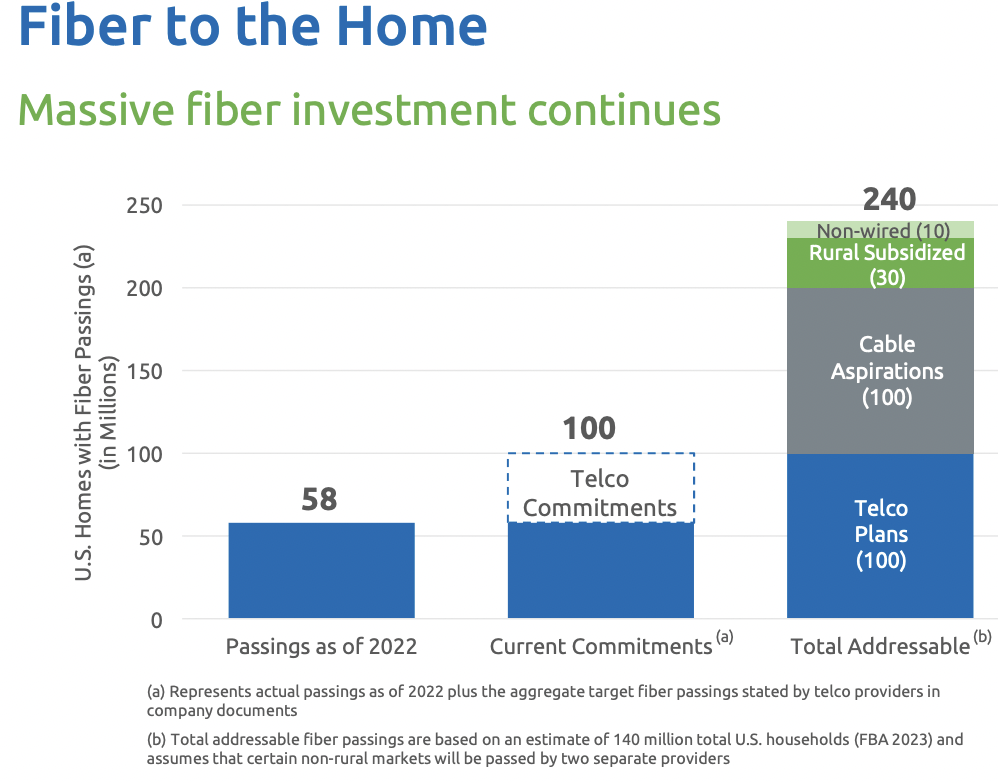

Taking a longer-term perspective, I believe DY stands to gain from the ongoing construction and upgrading of the wireline network by major telecommunication players. As US consumers are increasingly preferring higher speed internet access. Telecommunication giants such as AT&T, Verizon, and others are actively working to extend their high-speed internet services by investing more in high-speed wireline networks.

As of 2022, a total of 58 million fiber passings have been established in the United States. Several telecom providers have committed to substantial investments for the construction of an additional 42 million fiber passings in the coming years. These new fiber passings are expected to present heightened revenue opportunities for DY in the foreseeable future.

Company presentation

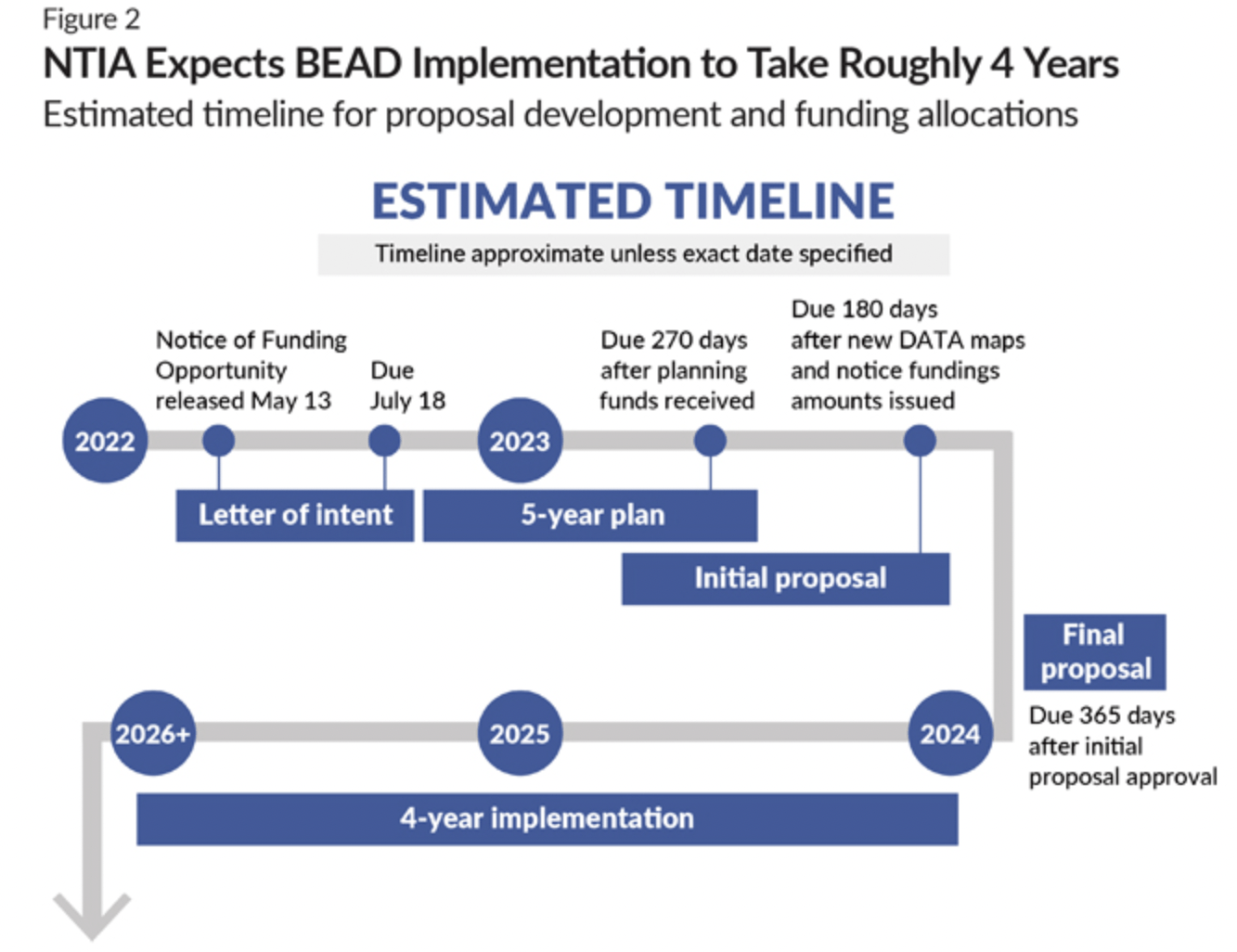

In addition to the commitments from telecom companies, DY is poised to benefit from a government-backed funding program such as Broadband Equity, Access, and Deployment [BEAD]. It is a $42 billion federal funding program aimed at providing broadband services to remote and underserved areas in the US. The implementation of this program is expected to benefit DY’s topline starting from 2024.

Pew Trust (primary source: NTIA)

Regarding margins, I foresee that the company is likely to report adjusted EBITDA margins surpassing its last five-year average range of 9%-10%. There are two reasons for my conclusion of higher adjusted EBITDA margins.

Firstly, as previously discussed, the anticipated surge in capital expenditures for fiber line networks by various telecommunication operators in the near future is expected to raise competition for the services provided by DY. Being one of the key players in its field, DY is poised to negotiate favorable contract terms, which should boost its margins.

Secondly, over the past few years, DY has consistently reduced its reliance on major customers. The company has successfully decreased its revenue dependence on its top five customers from 78.4% in FY20 to 54.4% during the trailing twelve months (TTM). This diversified revenue stream should empower the company with stronger negotiation capabilities with its large customers, which should also guide to improved margins.

In summary, the combination of higher topline growth and improved margins compared to historical averages is expected to benefit DY’s bottom line, contributing to enhanced earnings per share (EPS) growth in the foreseeable future.

Valuation

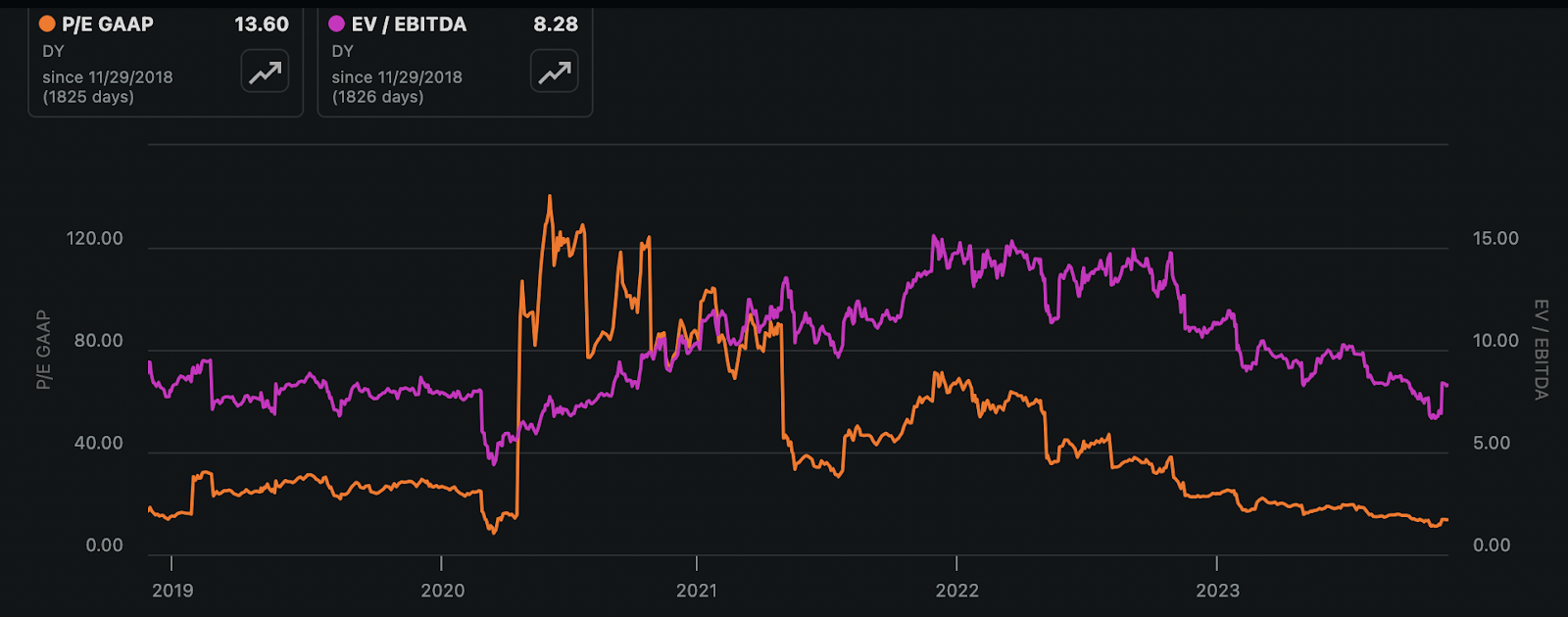

From a valuation standpoint, DY appears to be an attractive investment opportunity. Currently, its stock price is trading at $100.6 per share, representing a valuation of 13.6 TTM earnings and 8.28 times TTM EBITDA.

Source: Seeking Alpha

Both valuation ratios currently live at the lower end of their respective ranges, indicating that the market foresees diminished earnings growth for the company. This aligns with a broader trend affecting many cyclical stocks, resulting in reduced P/E ratios for such equities.

In contrast, I argue that DY should not be similarly valued, considering the revenue and margin prospects highlighted in this article. I believe that the company deserves a valuation of at least the last 5-year average trailing twelve-month EV/EBITDA multiple of 10x. I believe this valuation approach is reasonable as the growth prospects of DY have not been changed, on the contrary, the prospects have been improved.

Risk

DY Industries derives its revenue from a cyclical industry, a factor that has historically impacted DY’s earnings during business cycle downturns. While this concern is valid, I preserve the view that the underlying industry demand, telecom capital expenditures, and government funding are poised to serve as significant tailwinds for the company in the event of a full-blown downturn. Consequently, I believe the stock should outperform the market.

Notably, DY generated 54.4% of its TTM revenue from its top five customers. Despite the company actively reducing its dependence on these key customers, their proportion in the revenue mix remains high.

Conclusion

Dycom Industries exhibits resilience and growth potential in the telecommunications sector. Despite a slight slowdown in YoY growth, the expanding demand for wireline networks should benefit the company. Anticipated higher margins, reduced revenue concentration, and favorable valuation multiples emphasize DY’s attractiveness as an investment.

While I confess industry cyclicality, strong tailwinds such as wireline infrastructure spending by Telecommunication players and investments through the BEAD program should help the company weather a potential downturn. Hence, I am bullish on the stock.

Q2 2024 Earnings Call Transcript")