Jeremy Poland

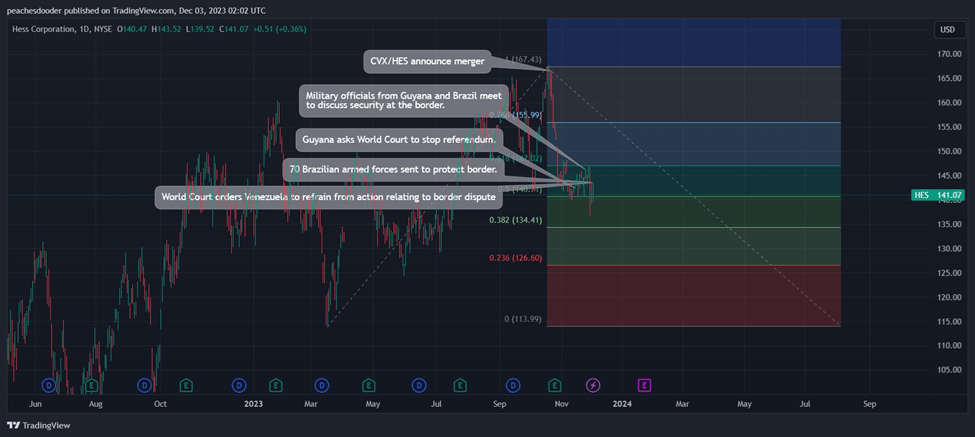

There’s been a lot of talk concerning the independence of Guyana as Venezuela presses forward with a referendum relating to the border. Overall, this shouldn’t be a challenge for Chevron (NYSE:CVX) given their authorization to work in Venezuela. What I’m most concerned about is if this escalates into an invasion, what will offshore drilling and production look admire after the fact, especially with the Hess (NYSE:HES) acquisition right around the corner? Guyana production accounts for 28% of Hess’s total production as of q2’23. With the addition of Payara, daily volumes in Guyana will account for closer to 40%. This assumes Hess’s 30% stake in the 620mboe/d in the Stabroek Block. Certainly, if the skirmish were to escalate and Venezuela potentially takes Guyana by force, I believe this could direct to advance sanctions and potentially a complete write-off of Guyana assets. This can also create challenges for Chevron’s Venezuelan production. My biggest concern is Chevron walking away from the acquisition or adjusting the acquisition price down if this were to occur. Until more information is released, I believe it would be prudent to furnish HES a HOLD recommendation and maintain my SELL recommendation on CVX maintaining my price target of $136/share for CVX.

TradingView

As a disclaimer, predicting geopolitical action is not in my field of expertise. The purpose of this report is to converse the potential effects of the border dispute in the instance of escalation.

The joint venture between Chevron and Venezuelan State oil company PDVSA produces 135mboe/d and exports 124mboe/d to the US. In total, using q3’23 production figures, this only accounts for 4% of Chevron’s total production. Bear in mind, Venezuelan assets are not accounted for in production and reserves figures, as disclosed in their 10-Q.

Corporate Reports

Relating to their reported financial statements, effects should not be visible if Chevron’s General License 41 were to be revoked and operations in Venezuela were to cease.

My eye is on Hess and their Guyana operations. Guyana accounts for 28% of Hess’s q3’23 production; and, with the added Payara project, will account for closer to 40% of total production.

Corporate Reports

Guyana accounts for 23% of Hess’s total proved reserves and 37% of their total oil and condensate reserves, in accordance with their last reported 10-k. The remaining assets are spread across North Dakota, the US Gulf Coast, and Malaysia & JDA. Though the Bakken assets are high-quality, short-cycle assets, I don’t believe these were the assets Chevron was targeting in the acquisition.

Holding constant q3’23 production volumes, losing the Guyana asset will reduce EBITDA by ~30%, assuming constant margins.

Corporate Reports

Again, this is purely a hypothetical exercise to comprehend the implications of the worst-case scenario of an invasion on Guyana and sanctions placed on the region. I believe the loss of the Guyana assets will place significant stress on the valuation of Hess and may direct to Chevron reconsidering the acquisition target. There’s no telling what will happen in Guyana until it happens; and advance, there’s no telling how the US Government will retaliate if an invasion were to occur. I don’t believe it would be appropriate to ring the alarm bells just yet. If you are a holder of Hess shares, my recommendation is to hedge your position by purchasing put options in the instance of this geopolitical risk going sideways. Otherwise, I maintain my SELL recommendation of CVX with a price target of $136/share and no price target for Hess as the stock will continue to track CVX and there are too many unknowns if otherwise.

Q2 2024 Earnings Call Transcript")