Leon Neal

Introduction

The aerospace and defense sector has been attractive lately. We see an increasing number of high-profile conflicts emerging. The war in Ukraine is still raging, and now there is also a conflict between Israel and Gaza. Looking forward, we see higher tensions in South America when Venezuela is looking to extend eastward and in Africa when Ethiopia is looking for access to the ocean. All these and possible conflicts may turn the sector into an interesting one.

A very interesting company within the sector is Northrop Grumman (NYSE:NOC). The company has a developed space segment and was a key James Webb Telescope project contractor. Therefore, it has both military and civilian products and services. A year ago, I analyzed the company and found it to be a HOLD, as the valuation was not compelling. It is time to revisit the company.

Seeking Alpha’s company overview shows that:

Northrop Grumman Corporation is a global aerospace and defense company with segments focusing on Aeronautics Systems, Defense Systems, Mission Systems, and Space Systems. Aeronautics Systems designs and sustains aircraft and autonomous systems. Defense Systems specializes in weapons and mission systems. Mission Systems provides cyber, intelligence, and reconnaissance systems. Space Systems offers satellites, missile defense, and launch vehicles.

Fundamentals

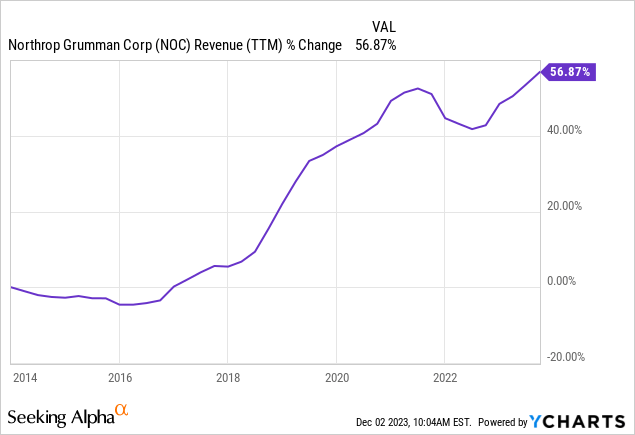

Northrop Grumman’s revenues have increased by 57% over the last decade. The graph below emphasizes how stable sales are, with almost no reject. The company derives over 85% of its sales from the U.S. government, a highly reliable client. It also grows using M&A, for example, the Orbital ATK acquisition for $9.2B. In the future, as seen on Seeking Alpha, the analyst consensus expects Northrop Grumman to keep growing sales at an annual rate of ~6% in the medium term.

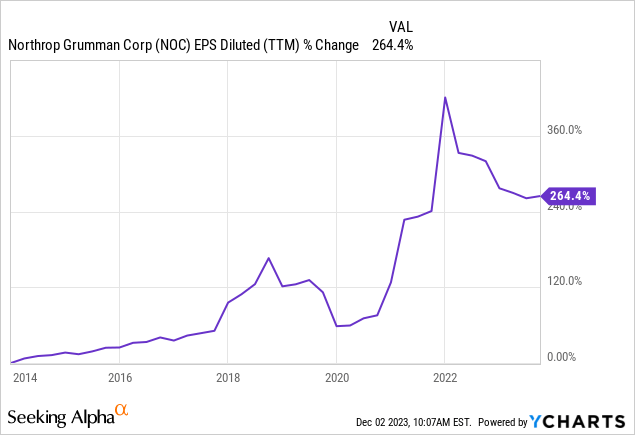

The EPS (earnings per share) of the company has grown at a much faster pace. The company achieved more rapid EPS growth due to buybacks and margin expansion. Operating margins have increased from 13% in 2013, peaked at 21% in 2021, and declined to 15% over the last twelve months. Higher inflation has increased costs, and the EPS has slightly decreased since its peak. In the future, as seen on Seeking Alpha, the analyst consensus expects Northrop Grumman to keep growing EPS at an annual rate of ~6% in the medium term.

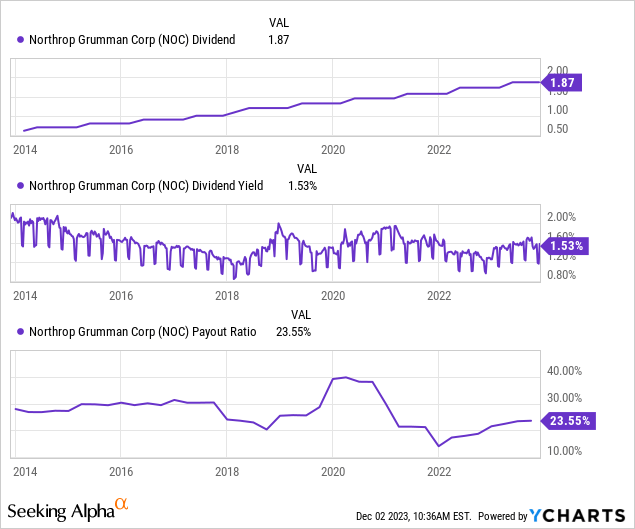

The company is a consistent dividend payer. Its 2024 dividend enhance will mark its 20th annual enhance in a row. The company also has not reduced the payment for more than 30 years. Despite its consistent earnings, the company maintains a conservative 23.5% payout ratio, which implies that the dividend is relatively safe and unlikely to be cut. The current entry yield is 1.53%, which may seem low, but the company has plenty of room to enhance it. I believe the company will preserve a mid-single-digit enhance, which aligns with its EPS enhance.

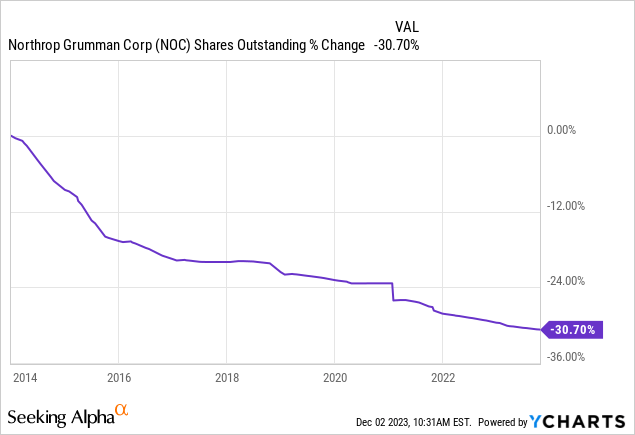

In addition to dividends, Northrop Grumman, appreciate many other blue-chip companies, returns capital to shareholders via buybacks. These share repurchase plans uphold EPS growth by decreasing the number of shares outstanding. Thus, the same income is divided by a smaller number of shares. Northrop Grumman has been highly efficient in its buybacks and bought back more than 30% of its shares in the last decade. Buybacks are effective when the valuation is low, and the company should execute them when the opportunity arrives.

Valuation

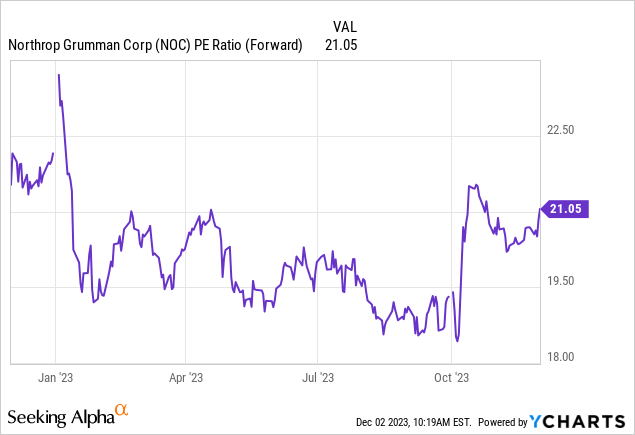

The P/E (price to earnings) ratio of Northrop Grumman stands at 21 when using the 2023 earnings forecasts, which show a 10% reject. The current valuation is almost the highest over the last twelve months. The company grows consistently but still not fast enough to defend such a rich valuation. The interest rate is high at 5%, allowing investors to access risk-free investments and gain decent returns. In that environment, the current valuation, which is even higher than when I analyzed it a year ago, is attractive.

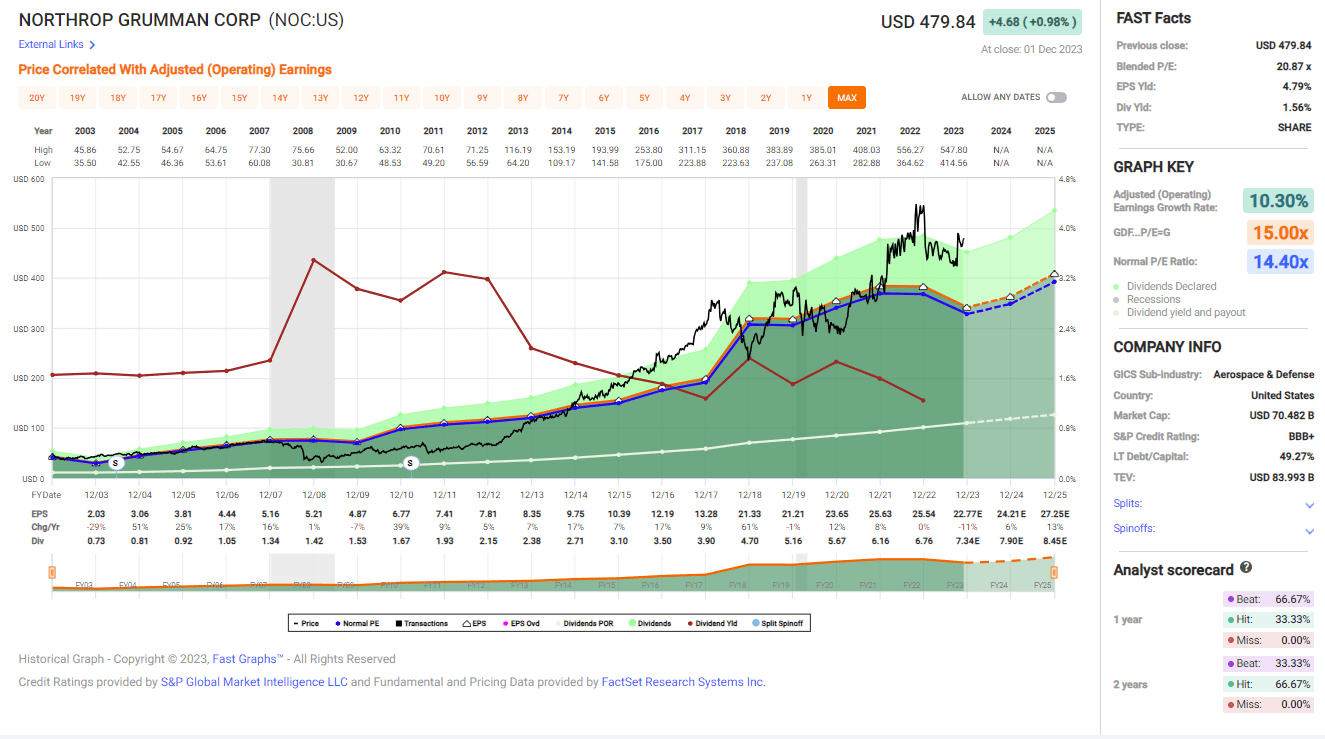

The graph below from Fast Graphs shows how the company in 2021 detached from its historical valuation. Over the last two decades, the average P/E ratio of the company stood at 14.4, and the compound annual growth rate was 10.3%. The company’s P/E ratio is around 21, while the forecasted growth rate is 6%. Therefore, while the company has solid fundamentals, its current valuation is unattractive. It reflects either very high expectations or investors flocking to safer havens.

Fast Graphs

Opportunities

The first opportunity is international demand for its weapon systems portfolio. Northrop Grumman is experiencing a significant surge in global demand for its weapon systems portfolio, particularly in missile defense technologies appreciate the IBCS product line. The company has received interest from more than a dozen countries for the AARGM-ER, and a foreign military sale opportunity to Finland has been announced. This growing international demand underscores the global recognition and trust in Northrop Grumman’s advanced weapon capabilities.

We are also seeing an enhance in international demand for our capabilities, with particular growth in our weapon systems portfolio and missile defense technologies appreciate the IBCS product line.”

(Kathy Warden, Chairman, CEO & President, Q3 2023 Conference Call)

Another opportunity is the development of advanced weapons capabilities. The company secured a $705 million contract from the United States Air Force to evolve the Stand-in Attack air-to-ground weapon designed to strike mobile defense targets. This initiative showcases the company’s commitment to providing new advanced weapons capabilities. Leveraging its mature product baseline, Northrop Grumman aims to reduce developmental time, cost, and risk for the SAW program, positioning these missiles as the air-to-ground weapon of choice for advanced fighter jets appreciate the F-35, the future fighter jet.

We are working with the U.S. government to furnish new advanced weapons capabilities. During the second quarter, we received a $705 million contract from the United States Air Force to evolve the Stand in Attack weapon, also known as SAW.”

(Kathy Warden, Chairman, CEO & President, Q3 2023 Conference Call)

Within the growing space business, the company has another growth opportunity. Northrop Grumman’s Space business is thriving, with a focus on being at the forefront of technology. The company has secured contracts, such as the $712 million award to design and build 36 satellites for the Space Development Agency’s tranche two transport layer data constellation. With approximately 100 satellites in the pipeline, Northrop Grumman’s success in space highlights its ability to contend and win.

Our success in this area highlights our ability to contend and win in highly competitive and dynamic new markets within the space domain.”

(Kathy Warden, Chairman, CEO & President, Q3 2023 Conference Call)

Risks

The uncertainty regarding defense budget spending is a significant risk, as the U.S. government is by far its largest customer. Northrop Grumman faces uncertainty in the U.S. defense budget, given the federal government’s operation under a continuing resolution for the start of fiscal year 2024. While there is bipartisan uphold for national security priorities, delays in reaching a full-year appropriations agreement pose a challenge. The company’s guidance assumes a full-year budget passed by the end of the calendar year or early next year, emphasizing the importance of political decisions to mitigate risks.

As is common in recent years, the federal government is operating under a continuing resolution to start fiscal year 2024. We’re encouraged by bipartisan uphold for national security priorities and are hopeful an agreement will be reached on full-year appropriations soon.”

(Kathy Warden, Chairman, CEO & President, Q3 2023 Conference Call)

A second risk is the operating margins declining from 21% to 15% due to inflationary pressures and higher costs. Northrop Grumman faces the challenge of inflationary pressures impacting operating margins. As global economies contend with inflation, rising costs for materials, labor, and other inputs squeeze profit margins. The company is already more optimistic and sees some improvement, but this is nevertheless a risk, especially when dealing with long-term contracts.

I would say that we are still on track for the trends that we have spoken of in operating margin. We see improvements, which is reflected in our guidance for 2023 in the fourth quarter.”

(Kathy Warden, Chairman, CEO & President, Q3 2023 Conference Call)

Another opportunity lies in the connection between pension obligations, market volatility, and financial market movements. Northrop Grumman acknowledges the challenge of market volatility and financial market movements, which can impact the company’s economic performance. Since the company pays for its employees’ pensions, there is a dynamic environment that the company has to steer. Financial market movements and interest rate movements change the company’s obligations towards its former employees. While sometimes it may benefit the company, it can also be risky and affect the EPS and performance.

Through September 30, financial market movements have led to a roughly 50 basis point enhance in discount rates and a year-to-date asset return of 1% to 2%. This combination of results would reduce net FAS pension income and enhance CAS recoveries from our prior projections.”

(David Keffer, Chief Financial Officer, Q3 2023 Conference Call)

Conclusions

In summary, Northrop Grumman is a major blue-chip in the aerospace and defense sector and presents a mixed outlook for investors. The company has demonstrated consistent revenue growth and global demand for its advanced weapon systems, positioning itself as a critical player in the industry. However, uncertainties surrounding U.S. defense budget spending and the impact of inflationary pressures on operating margins are also present.

Despite its resilient financial performance, I am concerned with the company’s current high valuation and lack of margin of safety. The current P/E of 21 and the lack of a clear path to a higher-than-average growth rate make me believe that, at the moment, the company is a HOLD until it reaches a P/E ratio of 15-16, which will better ponder the growth rate.

Q2 2024 Earnings Call Transcript")