Eloi_Omella

Investment Rundown

The green energy space is rapidly growing and I think having some type of exposure to the sector and industry is important for a well-diversified portfolio. With Enlight Renewable Energy Ltd (NASDAQ:ENLT) you are getting a rapidly growing business benefiting from exactly these types of tailwinds. The company had its IPO this year and the share price has roughly come back to the same level after being on quite a rollercoaster since February. One of the many positives of ENLT compared to other companies in the space is that they are already profitable with a TTM net income of $66 million, up from $11.2 million in 2021. With the production and business scaling up rapidly the premium it has against the sector seems justified as in a short time I think it can grow into it.

By 2026 the estimates are the ENLT will reach an annual EPS of $3.57 which puts them right now at an FWD p/e of 4.8. With the utility sector trading at a p/e of 16, I think ENLT is an exciting bet right now. What investors need to account for is some solution over the coming years and seeing as ENLT had its IPO this year in February, by next year I think the lock-up period could unveil some significant selling potential as early investors will want to get out, which is quite common in a lot of business. This could weigh on the stock price in the short term but in my view is not something that deters me enough to rate ENLT anything lower than a buy.

Company Segments

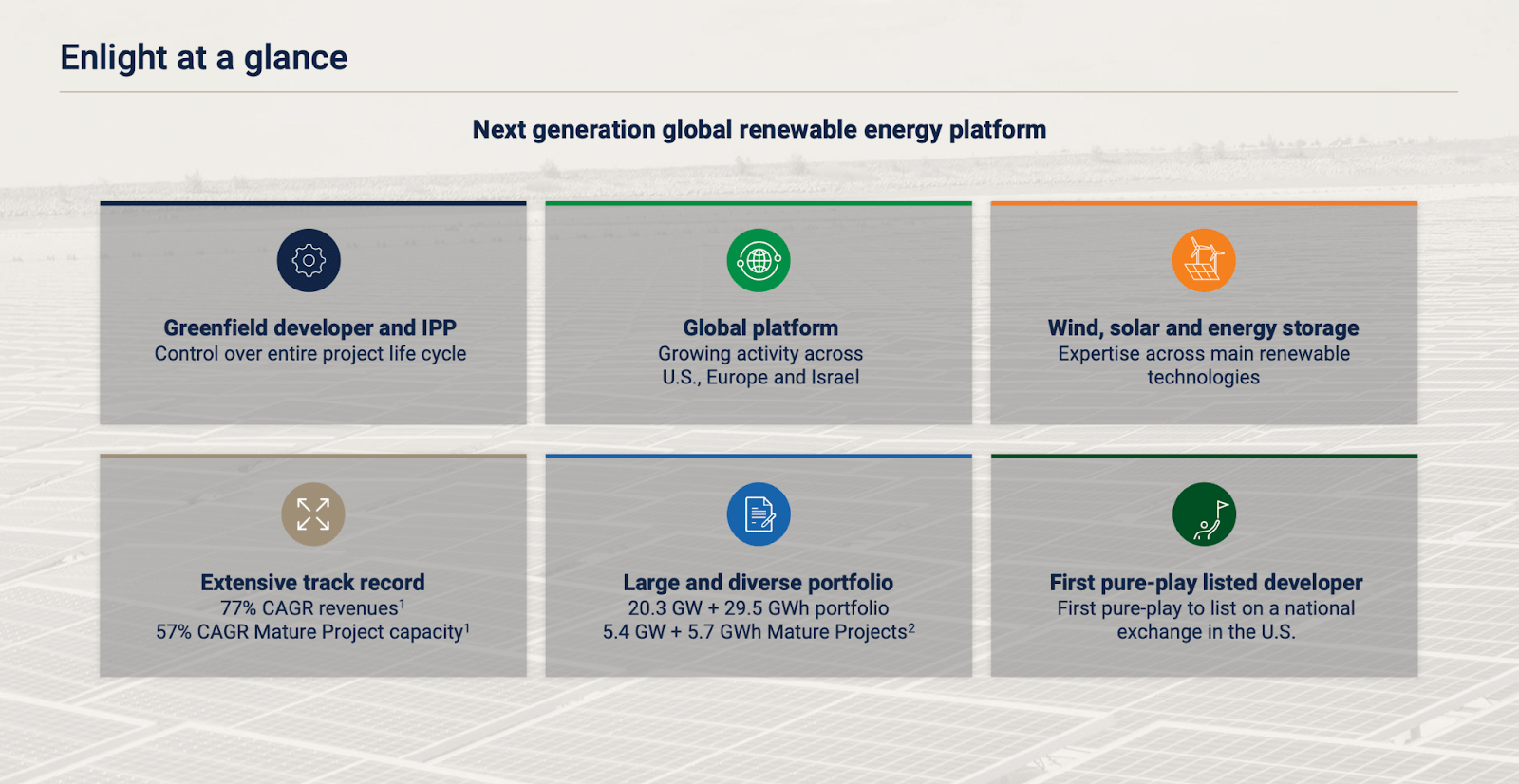

ENLT functions as a prominent renewable energy platform, both within Israel and on the international stage. The company is actively involved in the entire lifecycle of renewable energy projects—from initiation and planning to development, construction, and operation. Its portfolio encompasses a diverse range of projects focused on harnessing electricity from renewable sources, including wind and solar energy. Additionally, ENLT is engaged in the development of energy storage projects to boost efficiency and sustainability in the rapidly evolving renewable energy landscape.

Overview (Investor Presentation)

The renewable energy space is poised for significant growth in the coming years, driven by various factors. There is a global shift towards cleaner and sustainable energy solutions, spurred by increasing awareness of climate change and environmental concerns. Governments worldwide are implementing policies and incentives to encourage the adoption of renewable energy sources, contributing to the sector’s expansion. Ongoing technological advancements play a crucial role in enhancing the efficiency and cost-effectiveness of renewable systems. Solar and wind energy, in particular, have become increasingly competitive with traditional fossil fuels, thanks to declining costs.

Growth Numbers (Seeking Alpha)

The growth for ENLT over the last few years has been very good and I think it will continue that way as well for the foreseeable future. There are so many investments going into this space and I think ENLT won’t find it too difficult to find customers. ENLT engages it in rewarding projects that have helped it grow a portfolio to nearly 50GWh already resulting in a 77% CAGR of revenues.

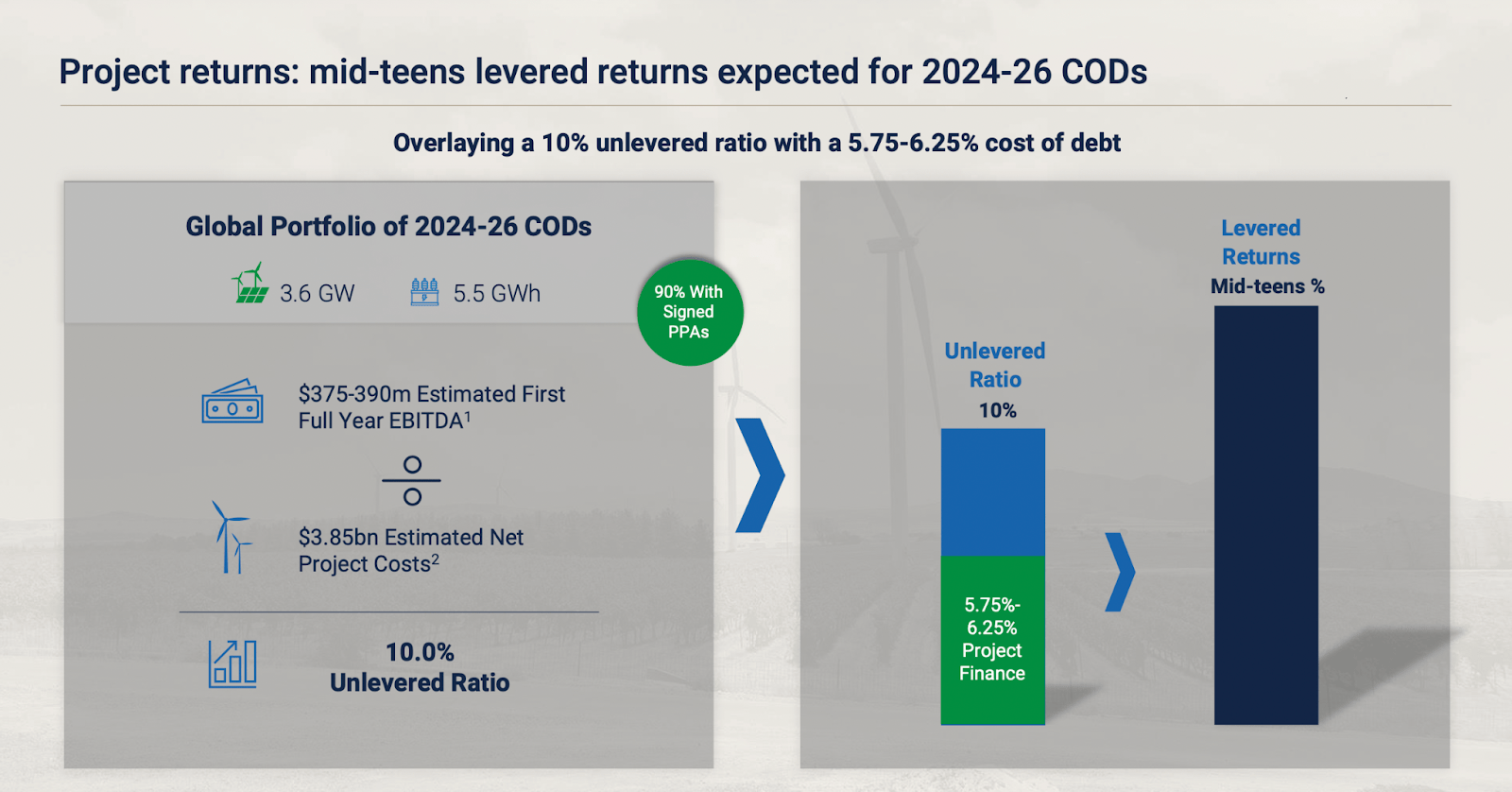

Project Returns (Investor Presentation)

The company manages approximately 17.0 gigawatts of power generation projects and possesses 15.3 gigawatt-hours of energy storage capacity, highlighting its substantial presence in the industry. As of September 30, 2022, Enlight has secured significant investments amounting to a fair market value of $765 million in equity. Notable contributors to these investments include key financial entities such as Migdal Insurance and Financial Holdings, Harel Insurance Investments & Financial Services, and Clal Insurance Enterprises Holdings. With strong institutional investments, I think the backing for ENLT right now is strong and will aid them in advance expanding their portfolio into a more mature state.

Earnings Highlights

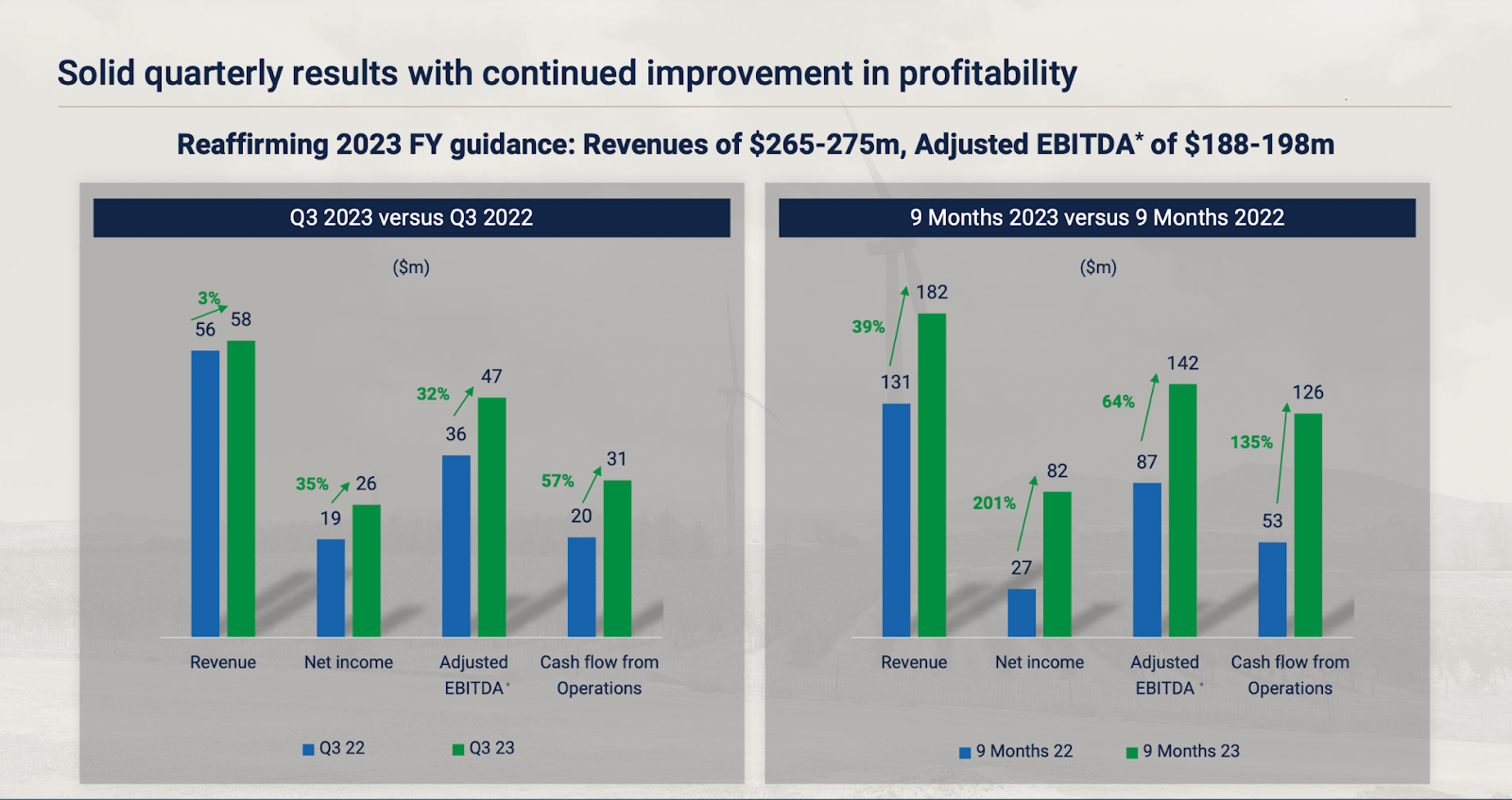

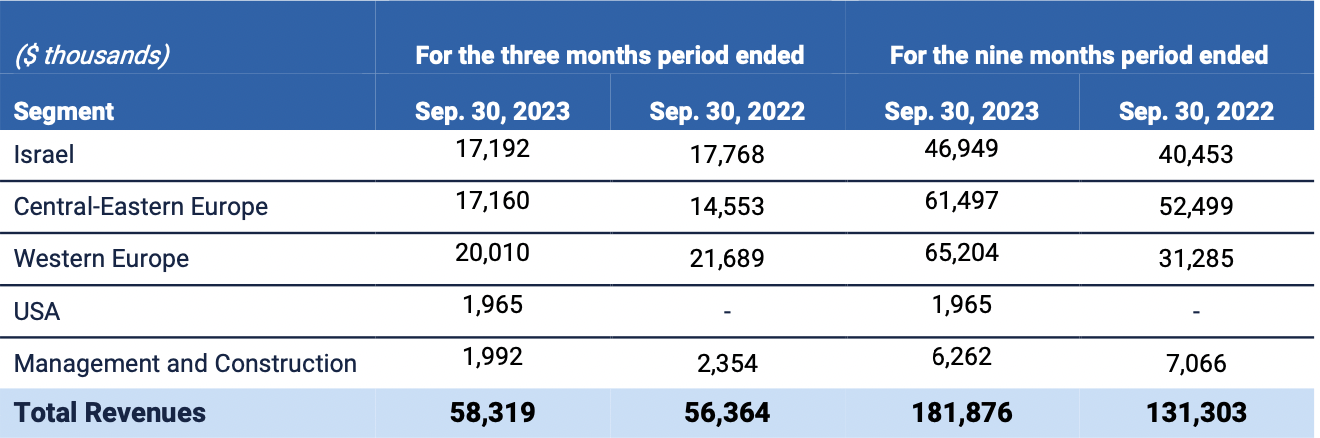

The last quarter for the company showcased strong results as the management reaffirmed the guidance set for 2023. One of the positive trends that occurred last quarter though was the impressive margin expansion. Whilst the revenues perhaps didn’t show as strong growth numbers as one would have hoped, just up 3% YoY, the net income grew by 35% YoY. This shift was much due to the refuse of commodities costs which made the projects and products the company makes far more profitable and less expensive.

Quarterly Results (Investor Presentation)

As I mentioned, the guidance for 2023 was reaffirmed at revenues of $265 – $275 million and adjusted EBITDA of $188 – $189 million. This puts ENLT at an FWD p/s of 7.3 and an FWD p/e GAAP of 25. Some of the project updates for ENLT were very positive in Q3. The definitive documentation was finalized for projects in both the US and Israel with both transactions amounting to over $500 million. This has led the management to expect around $300 million more excess equity to be returned to the company.

Market Overview (Investor Presentation)

I think that the development the company has had in the US is one of the most important. Seeing as the revenues from there are not that high and Western Europe being the highest means they have access to a massive market opportunity still. The market size here is over $269 billion which I certainly want to see ENLT proceed more aggressively into in the coming decade.

Risks

Considering the company’s location in Israel, the current geopolitical situation adds an element of risk to its share price. The ongoing conflict in the region puts pressure on the company’s infrastructure. Despite being in the renewable energy sector with a robust reputation, the impact of the conflict may pose challenges. On a positive note, given the societal importance of progress in renewable energy, there’s potential for aid to preserve rebuilding efforts. However, investors must confess the inherent risk associated with the company’s location and consider this factor in their investment decisions.

Shares Outstanding (Seeking Alpha)

Some of the risks that are facing investors include the story of share dilution that ENLT has. I think those who seek a more stable and more shareholder-focused business may want to look elsewhere instead. But I have a strong conviction that in time ENLT will be able to efficiently modify into a dividend-distributing business that can also afford to allocate capital to buying back shares too. I think that ENLT is, however, growing its bottom line quickly enough that the dilution isn’t having such a negative effect on the business but rather enables it to more aggressively enlarge and build a robust portfolio of projects.

Final Words

The renewable energy space is a very exciting one to be a part of and I think one of the better options right now is ENLT. The company is operating in a risky environment right now seeing as the conflict in Israel and Gaza has escalated rapidly over the last several weeks. I think however that the risk/reward with the business is still too good to pass up on. ENLT has proven itself capable of quickly growing both the top and bottom line and will be a very solid investment over the next decade and beyond.

Q2 2024 Earnings Call Transcript")