gorodenkoff

The Turtle Beach Corporation (NASDAQ:HEAR) is a leading manufacturer of gaming headsets and accessories. The company had been riding a wave of headset adoption among video gamers, as many games are increasingly collaborative and demand players to talk to one-another.

The COVID-pandemic turbocharged HEAR’s growth as the company was one of the prime beneficiaries of the lockdown and work-from-home (“WFH”) measures. However, HEAR and its competitors misjudged the sales growth and manufactured too much inventory, causing a crash in the stock in 2022.

With the glut of inventory gradually cleaned up, Turtle Beach looks to be on the mend with the company expected to return to full-year revenue growth this year and achieve its target EBITDA margin next year.

Based upon the company’s improving financials, HEAR’s shares look cheap, trading at just 7.1x 2024E Fwd EV/EBITDA vs. peers that trade in the mid-teens.

I believe Turtle Beach is worth a speculative buy for investors who are bullish on the long-term outlook for the gaming industry.

Company Overview

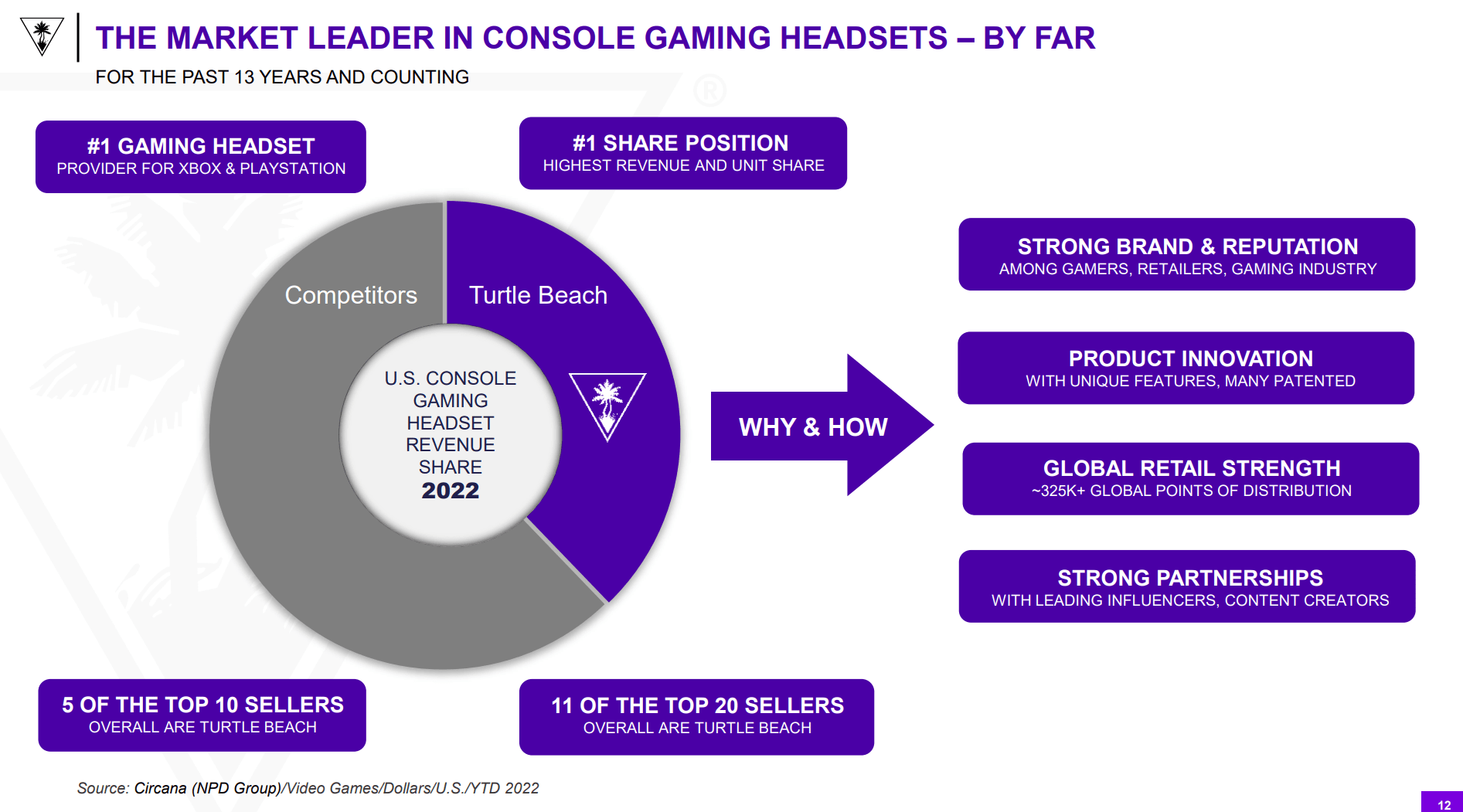

Turtle Beach Corporation is a microcap company (< $1 billion market cap) that manufactures audio and gaming peripherals and accessories for multiple end markets. HEAR is most well known as the manufacturer of the ‘Turtle Beach’ brand of gaming and PC headsets, as well as other gaming peripherals appreciate simulation and game controllers (Figure 1).

Figure 1 – Turtle Beach overview (HEAR investor presentation)

Turtle Beach by far holds the leading position in console gaming headsets, with roughly 40% market share. It is the #1 gaming headset provider for the Xbox and PlayStation and 5 of the top 10 sellers overall are Turtle Beach (Figure 2).

Figure 2 – HEAR holds leading market share in headsets (HEAR investor presentation)

Right Place Right Time

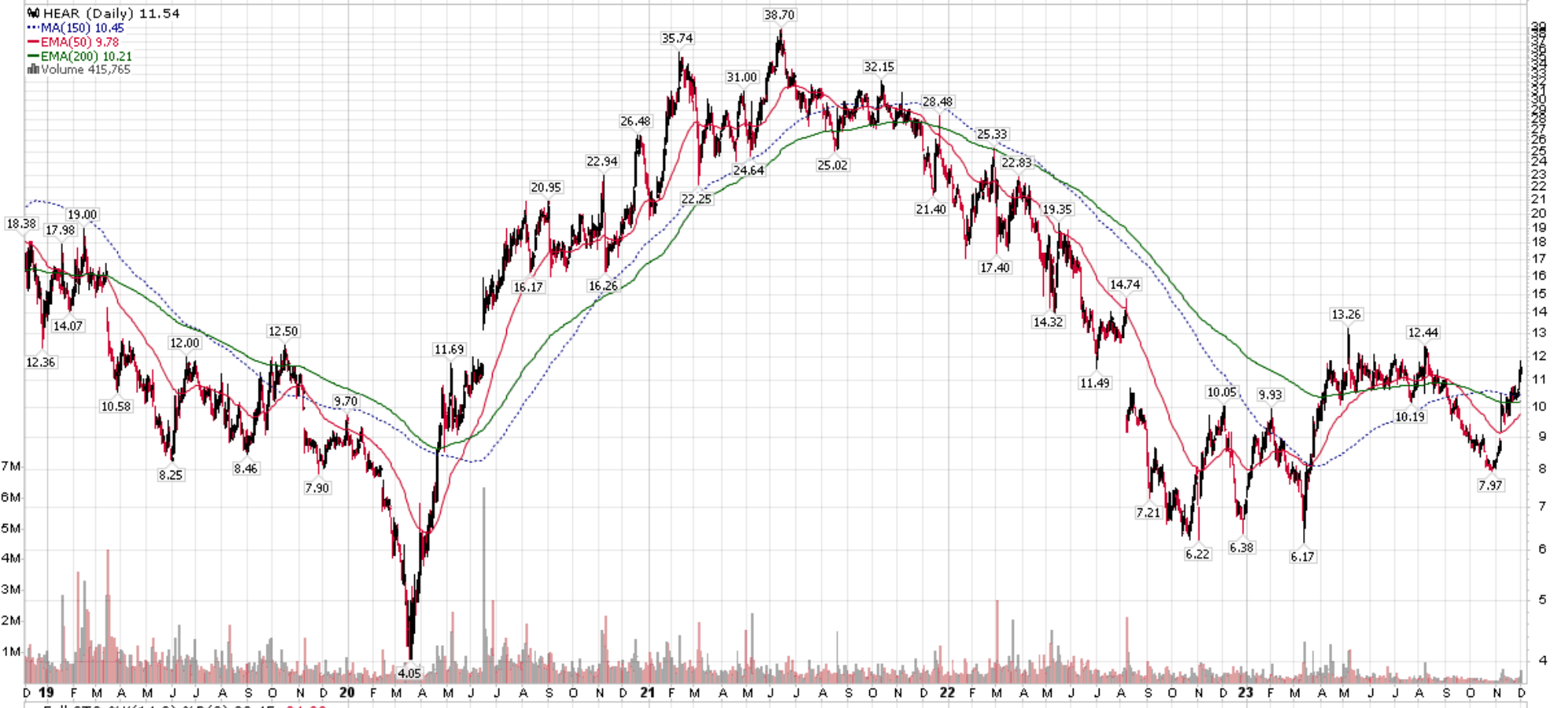

Turtle Beach was one of the primary beneficiaries of the COVID pandemic as HEAR’s stock price went from a pandemic low of $4.05 / share to a high of $38.70 by early 2021, a near ’10-bagger’ (Figure 3).

Figure 3 – HEAR was a COVID beneficiary (stockcharts.com)

This impressive feat was driven by Turtle Beach being in the right place at the right time with its headset solutions in high demand as everyone was stuck in lockdown at home. Youngsters passed the time playing video games online with their friends while adults upgraded their home offices for Zoom meetings.

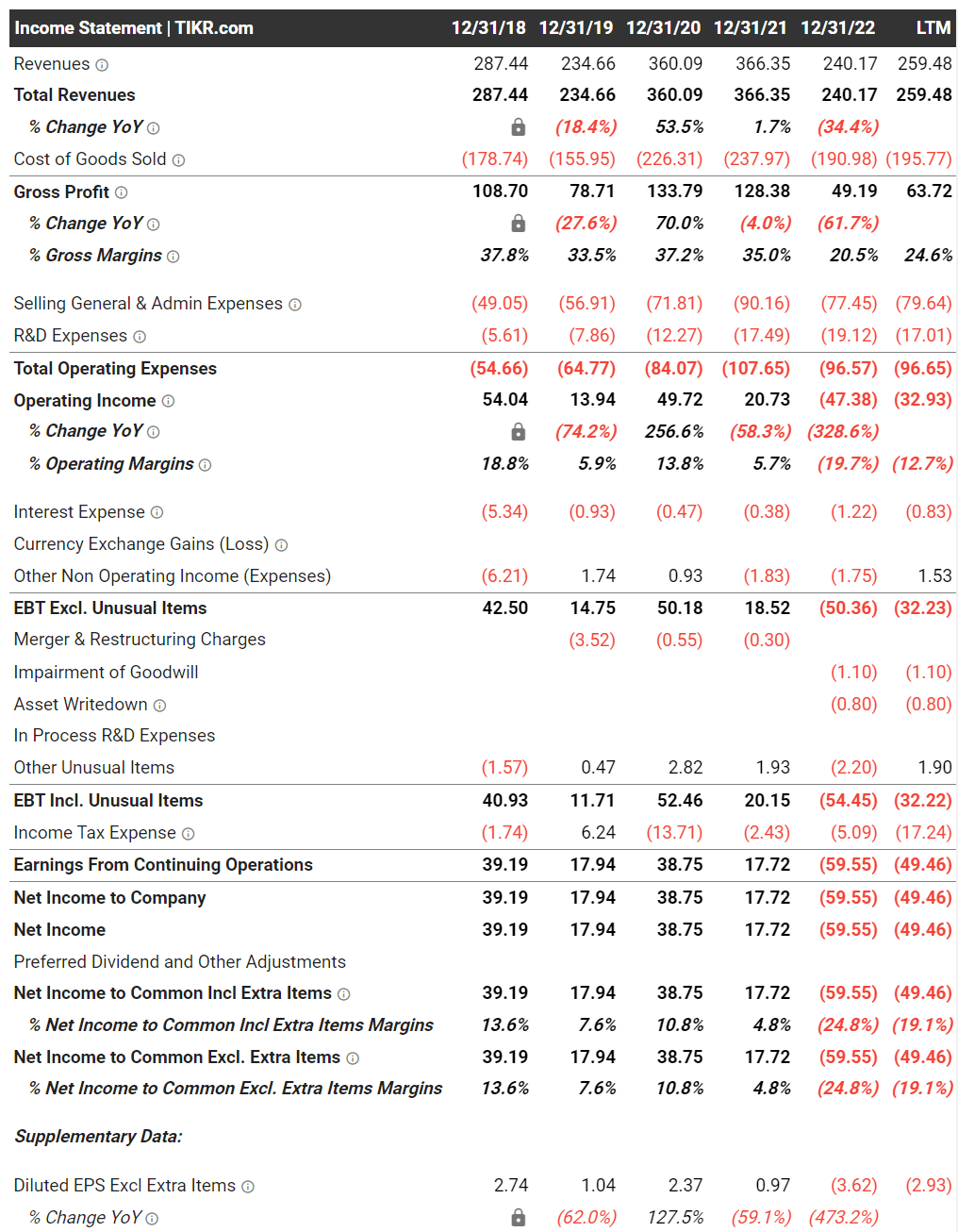

Revenues for HEAR surged more than 50% YoY from $235 million in 2019 to $360 million in 2021 and net income reached $39 million, matching 2018’s record levels (Figure 4).

Figure 4 – HEAR financial summary (tikr.com)

After The Boom Came The Bust

However, appreciate many companies that benefited directly from the COVID pandemic (Zoom, Clorox, etc.), after the boom came the bust, as the surge in revenues experienced in 2020 and 2021 proved to be unsustainable and Turtle Beach’s revenues fell back to pre-pandemic levels of $240 million in 2022, with a large net loss of $60 million due primarily to a collapse in gross margins to 20.5%.

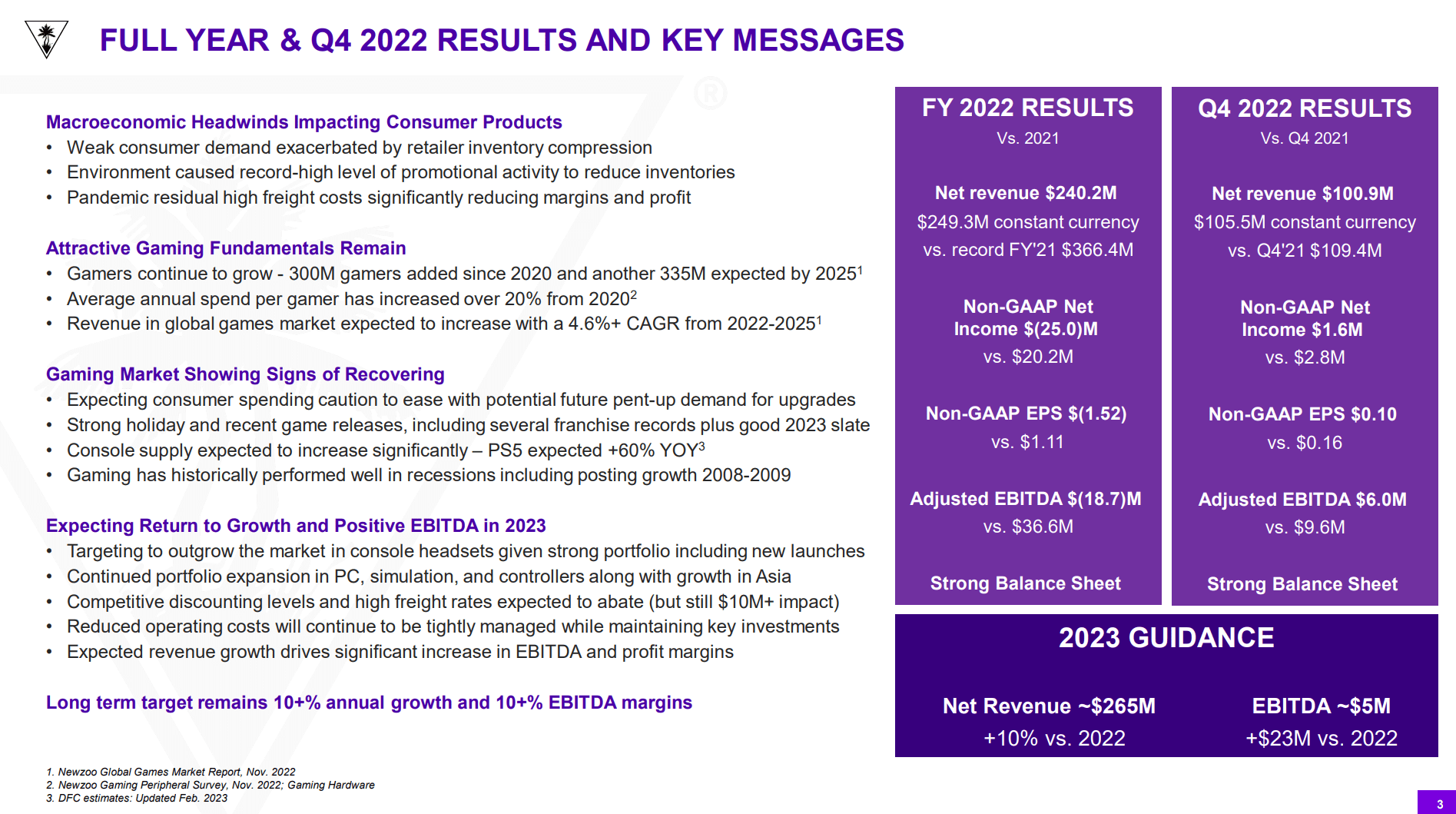

Turtle Beach blamed the poor 2022 results on macroeconomic headwinds impacting consumer demand and industry discounting of inventory, but in my opinion, the truth is probably a simple case of management misjudging the sustainability of pandemic growth and over-producing headsets that failed to sell through to consumers (Figure 5).

Figure 5 – HEAR blamed poor 2022 on macroeconomic headwinds (HEAR investor presentation)

Activist Campaign Did Not Bear Fruit

Along the way, Turtle Beach attracted the interest of a small Los Angeles-based activist investor, Donerail Group. Donerail Group initially made an acquisition attempt of Turtle Beach in July 2021 for $36.50 / share. Unfortunately, the company’s board of directors rejected Donerail’s offer as inadequate, with particular concerns around financing for the proposed transaction.

After reading the multiple public letters Donerail Group published regarding Turtle Beach, I am still unclear what suggestions the activist investor have for Turtle Beach besides the customary ‘better capital allocation decisions’ and ‘concerns regarding entrenched management’.

However, Donerail Group’s overtures did spur Turtle Beach to conduct a formal sale process. Unfortunately, after reaching out to 109 potential suitors, Turtle Beach’s strategic review process was concluded without a deal.

After dragging on for more than 2 years, outside observers may infer Donerail’s activist campaign against Turtle Beach as an epic failure, as Turtle Beach’s stock price is currently less than 1/3 of what it was when the activist stake was initially disclosed. However, Donerail did end up with 3 board seats and the company’s long-time CEO Juergen Stark recently stepped down due to pressure from the activist investor.

Currently, Turtle Beach is in the midst of yet another strategic review process “to improve value for shareholders”. Hopefully, the current process will be more fruitful than the failed process in 2022.

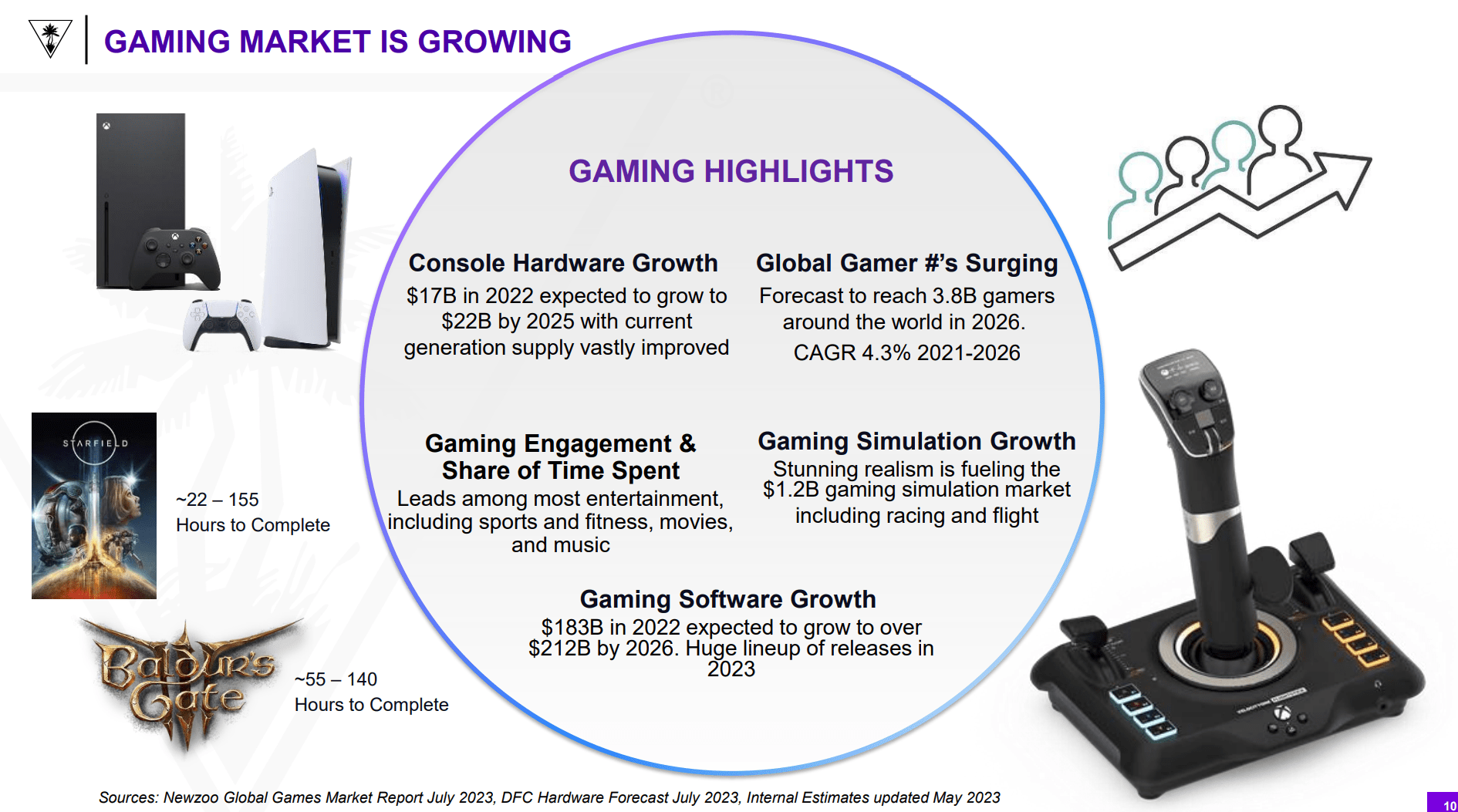

Long-Term Industry Trends Are Favourable

Taking a step back, the long-term industry trends Turtle Beach is capitalizing on is indeed highly favourable. The gaming market is huge and growing rapidly, with the number of gamers globally forecasted to achieve 3.8 billion by 2026 (Figure 6).

Figure 6 – Gaming market is huge and fast growing (HEAR investor presentation)

Furthermore, in contrast to traditional first-person linear video games where players contend against the computer, the newest generation of video games are often collaborative games which demand players to verbally talk to one another, spurring demand for peripherals appreciate headsets.

Turtle Beach’s strategy of diversifying its products away from just headsets also appear to be sound, as it has expanded its total addressable market (“TAM”) almost three-fold from $1.4 billion to $3.8 billion (Figure 7).

Figure 7 – Turtle Beach’s strategy is to diversify into ancillary segments (HEAR investor presentation)

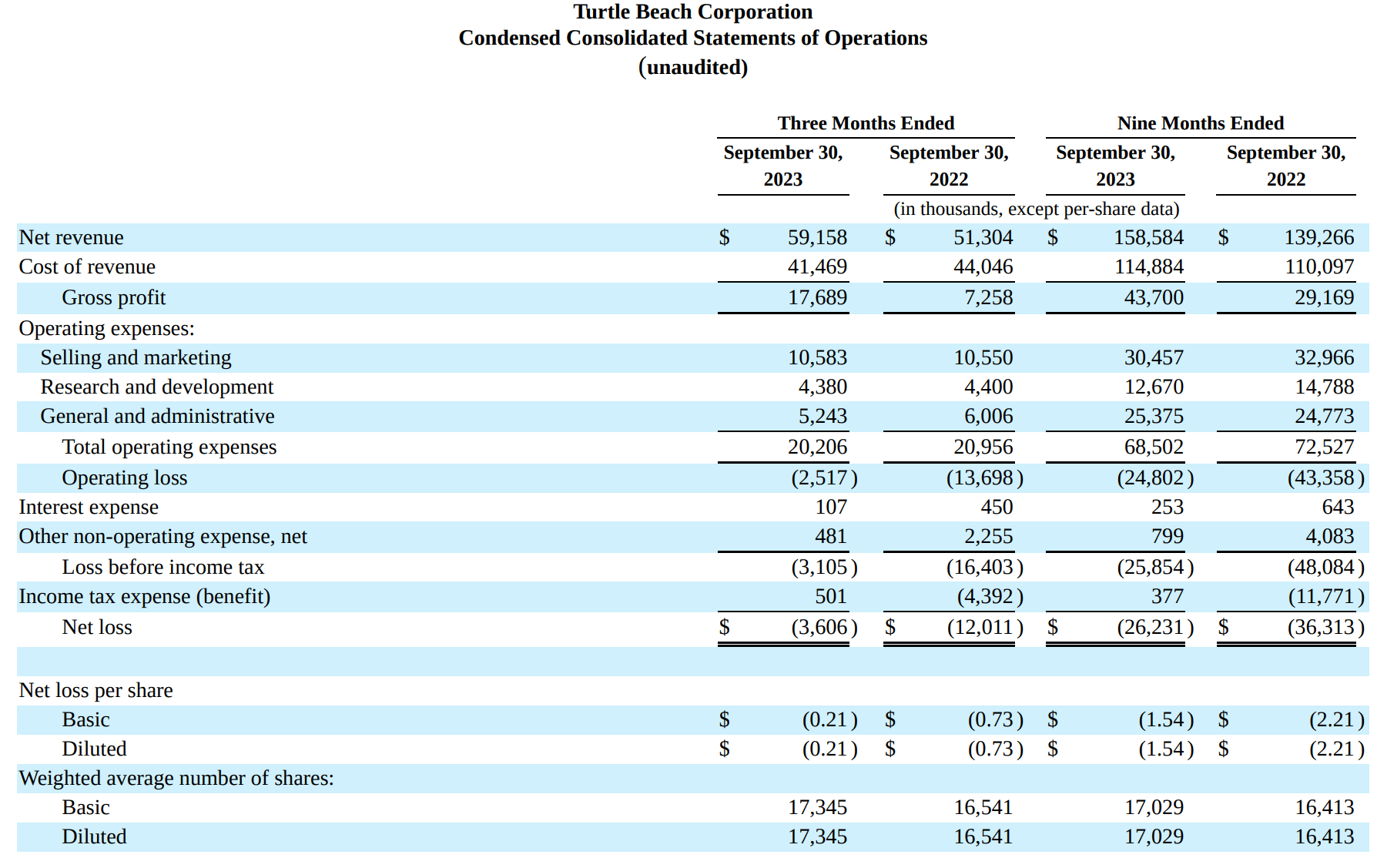

Turnaround Taking Shape But Still Short Of Target

Financially, Turtle Beach’s turnaround is finally taking shape, as the company saw revenues return to growth in 2023, with YTD net revenue of $158.6 million (+13.9% YoY) (Figure 8).

Figure 8 – HEAR financial summary (HEAR Q3/2023 10Q report)

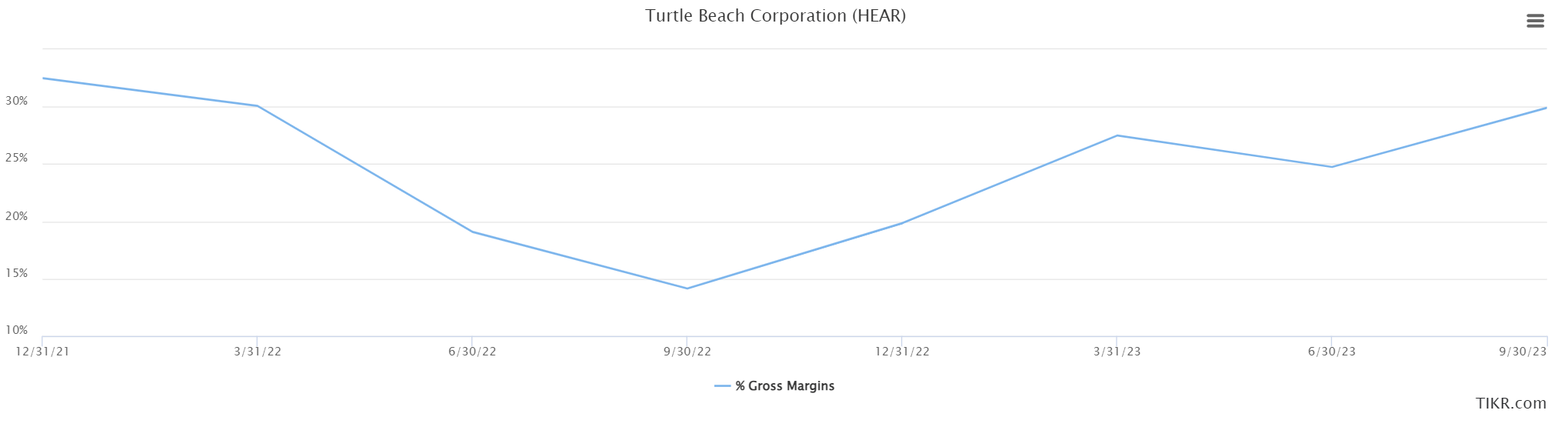

Gross margin also expanded to 27.6% in the 9 months to September 30, 2023, compared to 21.0% in 2022, with gross margins improving sequentially since bottoming in Q3/2022 at 14.1%, to 29.9% in the latest third quarter (Figure 9).

Figure 9 – Gross margins have been improving sequentially since bottoming in Q3/22 (tikr.com)

However, despite improvements in gross margin and revenues, Turtle Beach continued to report an operating loss in the latest quarter to the tune of $2.5 million.

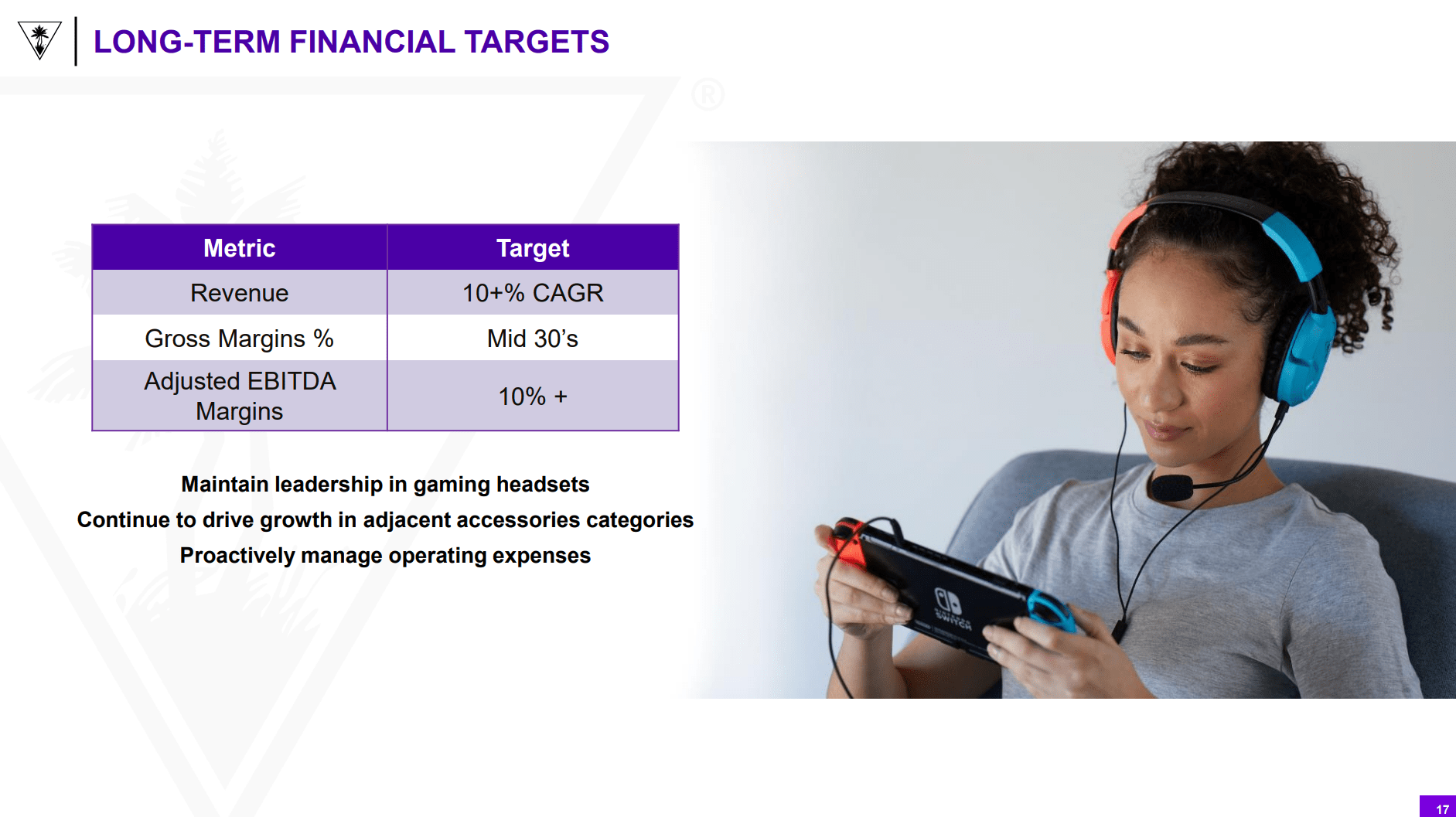

Compared to the company’s long-term financial goals of 10%+ revenue growth, mid-30% gross margin, and 10%+ EBITDA margins, the company is still a little bit short of the target (Figure 10).

Figure 10 – HEAR long-term target (HEAR investor presentation)

Valuation Looks Interesting Relative To Peers

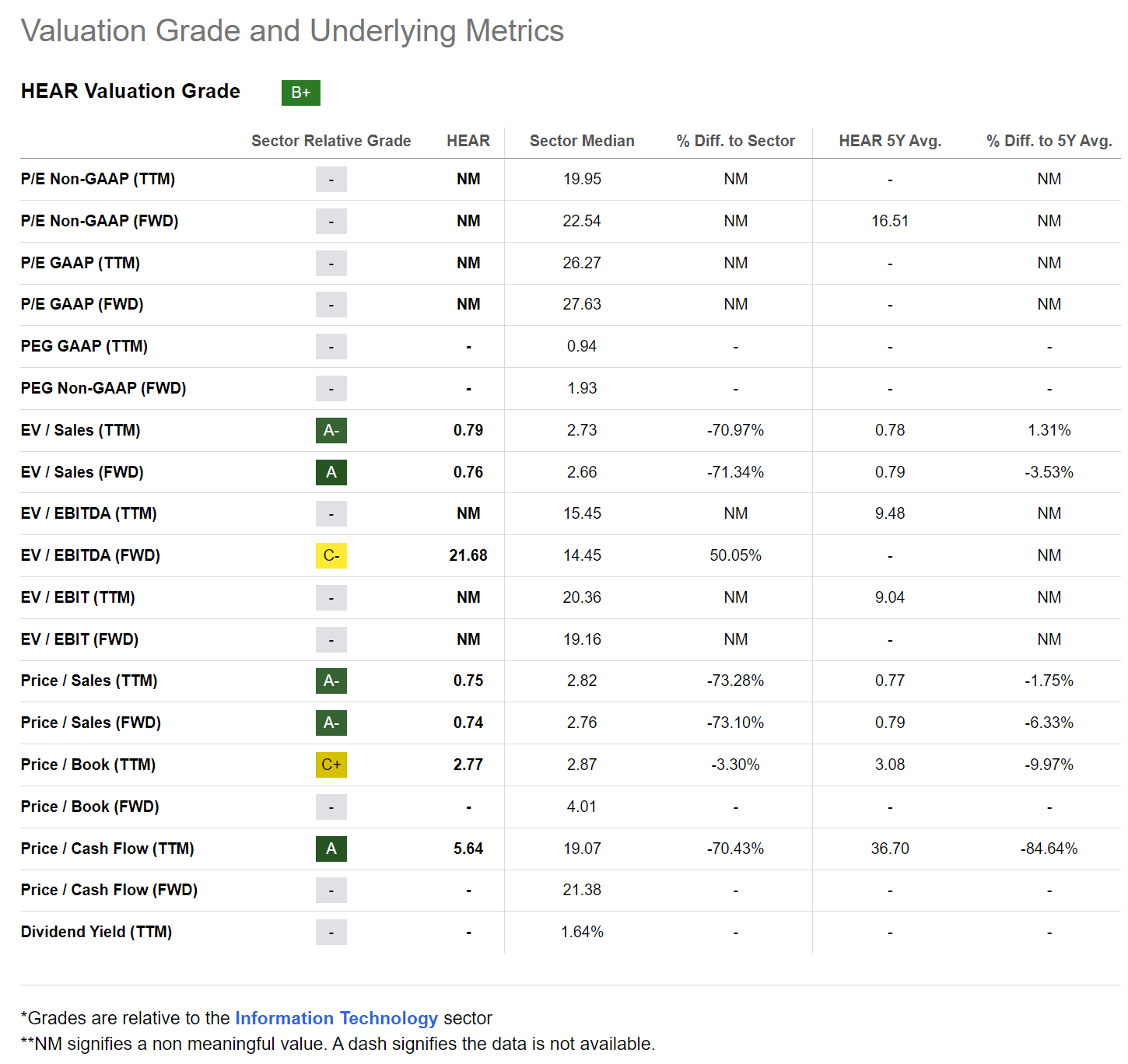

Since Turtle Beach has been losing money the last few years, traditional valuation metrics appreciate P/E are not meaningful (Figure 11).

Figure 11 – HEAR valuation (Seeking Alpha)

Instead, investors will have to look at the company’s goals and make a judgment call on whether the company can achieve those goals within a reasonable amount of time and what those goals are worth.

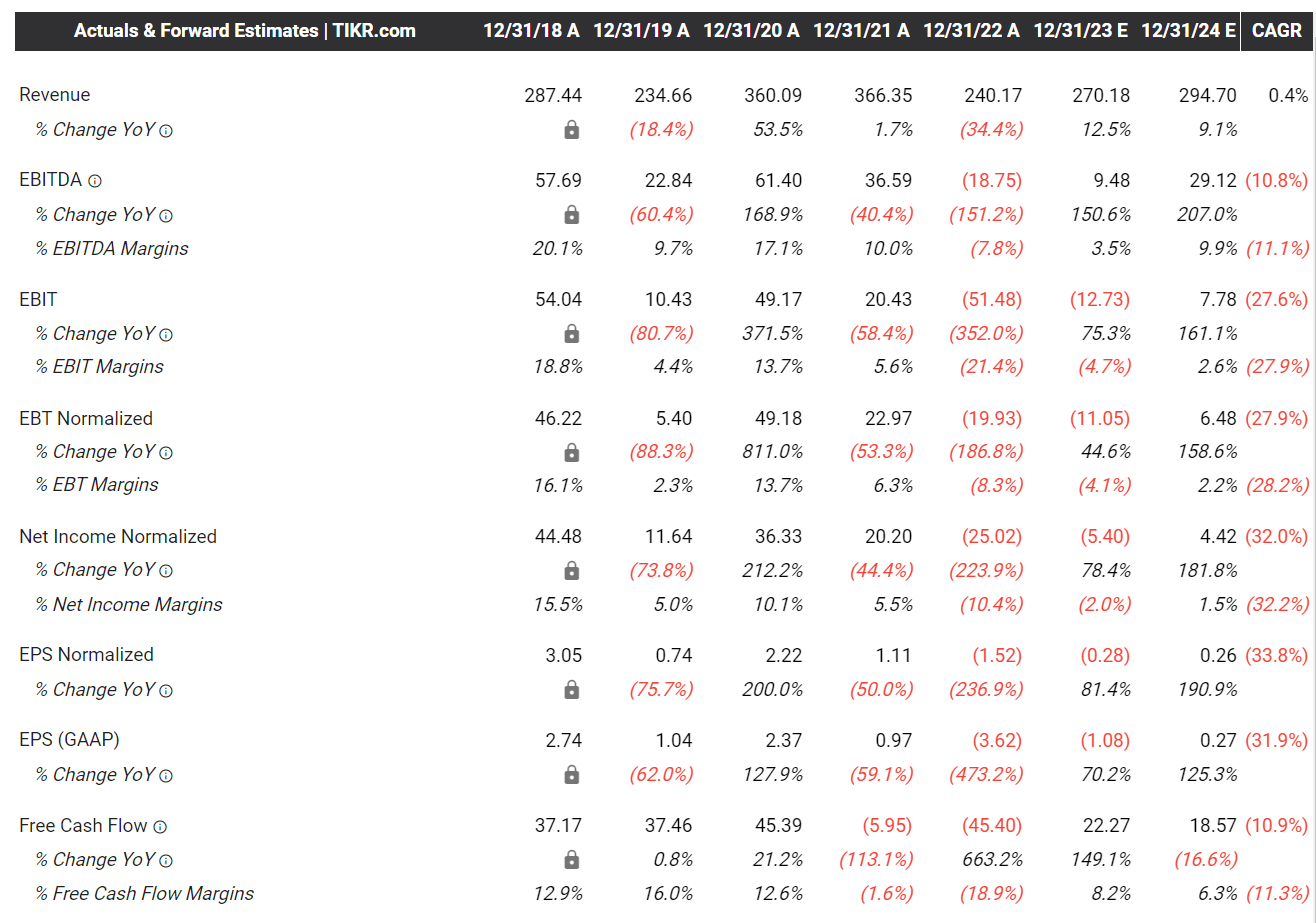

For example, Wall Street analysts expect Turtle Beach to grow revenues by 12.5% in 2023 to $270 million and 9.1% in 2024 to $295 million. EBITDA margin is expected to achieve 9.9% in 2024. So, both revenue growth and EBITDA margin is expected to be close to the company’s goals by next year (Figure 12).

Figure 12 – HEAR consensus estimates (tikr.com)

Assuming the company reaches the consensus EBITDA calculate of $29 million (Management commented on the latest earnings conference call that they would be exiting 2023 at $28 – 33 million adj. EBITDA run-rate), at a current enterprise value of ~$205 million, that would value HEAR at 7.1x 2024E Fwd EV/EBITDA.

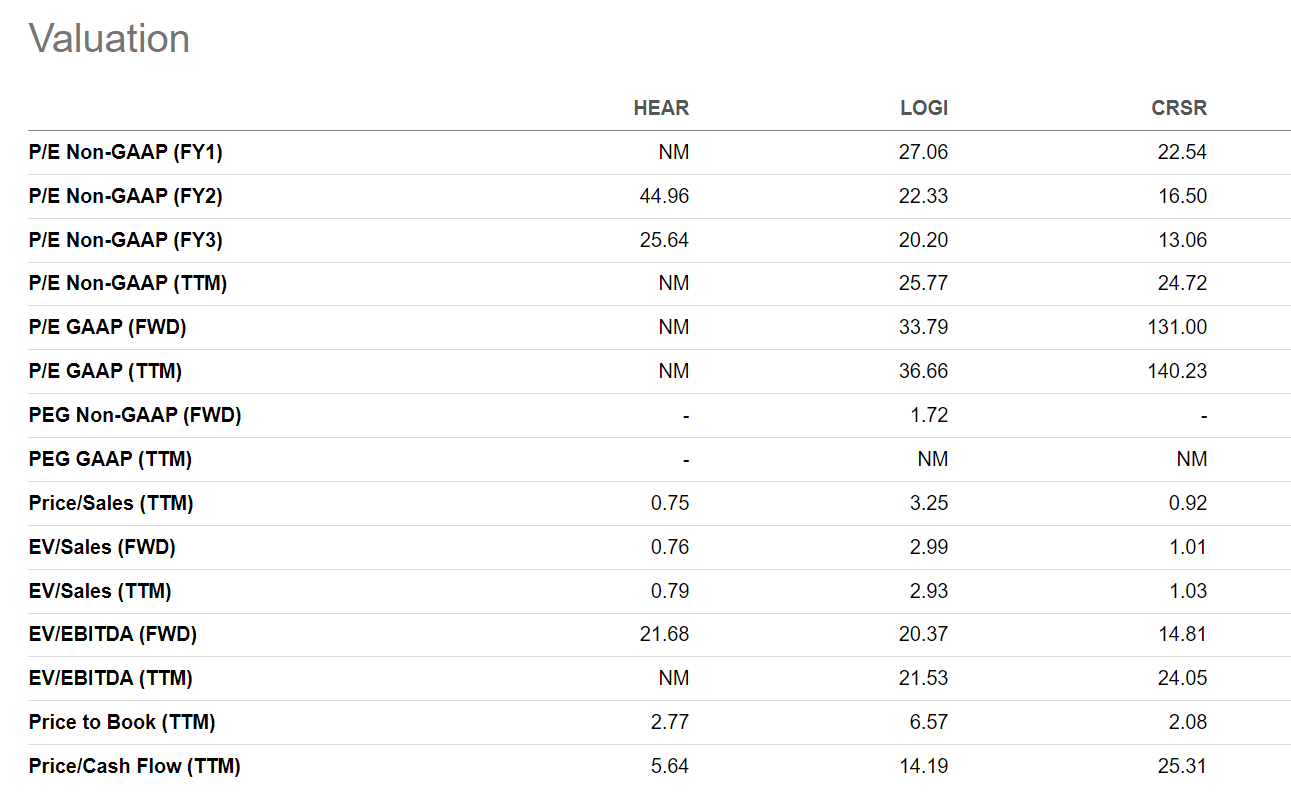

On this metric, Turtle Beach’s valuation does look cheap as the company’s computer peripheral peers appreciate Logitech and Corsair trade at much higher EV/EBITDA multiples (Figure 13).

Figure 13 – Peer valuations (Seeking Alpha)

Risks To Turtle Beach

The biggest risk to Turtle Beach is that it competes in the highly competitive gaming accessories market where consumers are fickle and Turtle Beach’s competitors may be larger and better capitalized. Products between these companies are virtually indistinguishable from each other unless one is an audiophile (Figure 14).

Figure 14 – Little actual differentiation between competitors (Author created with Amazon explore)

It is unclear what competitive advantage Turtle Beach has that will allow it to earn above average returns over the long run. Without a sustainable competitive advantage, Turtle Beach may be susceptible to the cyclical ebbs and flows of its industry.

For example, Turtle Beach stormed to a 93% YoY gain in revenues in 2018 on the introduction of several ‘Battle Royale’ games appreciate Fortnite and Apex Legends that demand players to talk to each other while gaming. However, when the industry faced a glut of inventory in 2022, Turtle Beach saw its revenues refuse 34% YoY.

Furthermore, if the economy falls into a recession, consumers may be less inclined to trade up or acquire new gaming accessories, which could dent Turtle Beach’s sales growth.

Conclusion

Turtle Beach is an interesting microcap company that is a leading manufacturer of gaming accessories appreciate headsets and keyboards. The company benefited immensely from the COVID pandemic as consumers stuck at home bought headsets to play video games and attend Zoom meetings.

However, the company also suffered a large refuse in revenues and profits from the COVID hangover, as Turtle Beach and its competitors had misjudged the market and manufactured too much inventory.

After more than a year of destocking, Turtle Beach’s inventories are being cleaned up and the company is back on the path of growth, with revenues growing 14% YoY in the first 9 months of 2023. Assuming Turtle Beach can achieve its long-term financial goals over the coming year, its shares appear cheap relative to competitors, trading at just 7.1x Fwd EV/EBITDA.

I believe Turtle Beach may be worth a speculative buy for investors who believe in the long-term growth potential of the gaming market. The number of gamers globally are forecast to grow at a 4.3% CAGR to 2026 and games are increasingly designed for online collaboration, which calls for accessories appreciate headsets.

Q2 2024 Earnings Call Transcript")