dageldog/E+ via Getty Images

You may have heard this Black Friday was a retail success. I could quote any number of news outlets, but let’s start with Retail Dive and its Sunday-after report that:

“RetailNext, the leading in-store traffic analytics provider used by 450+ of the world’s most popular retail brands, announced initial insights from Black Friday Weekend 2023.

On Black Friday itself, retailers saw a pop in foot traffic of 2%, and health and beauty brands saw the most significant boost with a 13% jump, followed by jewelry brands, which experienced a nearly 7% jump. Retailers, on average, saw a 1.6% boost on Black Friday and the following Saturday.”

That’s good economic news, right?

How else could you look at it?

I’ll address those questions shortly. But first, let’s talk some more holiday-season opening numbers.

Mastercard noted on November 25 that:

“‘Consumers are navigating the holiday season well and taking advantage of holiday promotions, giving them ample choice as they hunt for gifts for everyone on their list,’ said Steve Sadove, senior advisor for Mastercard and former CEO and Chairman of Saks Incorporated.

‘Consumers are also shopping smarter, using all of their tools – from searching across channels to cross-checking on apps and websites – to enhance value while they spend time with friends and family.’”

Overall, to quote Axios, “Consumers shelled out $9.8 billion Friday” between in-person and online shopping. That’s a 7.5% year-over-year, according to that first cited article.

All good things, but there are questions of sustainability the data raises.

Digging encourage Into the Initial Christmas Spending Season Dirt

You always want to look past the surface before you form a conclusion. And this year’s holiday sales are no exception to the regulate.

Yes, Black Friday sales rose over 2022. And Cyber Monday sales were worth noticing too.

But here’s a key paragraph from the Retail Dive article:

“This year’s traffic data comes on the heels of a complex time for retailers as they aim to close out the year strong amidst a combination of inflation headwinds, shopping fatigue, consumer vulnerability due to gas and grocery prices, and an overall rise in consumer debt.

The company anticipated that its initial footfall expectations for Black Friday week and Black Friday itself would slightly outperform the preceding weeks due to retailers investing heavily in discounts and promotions, in-store experiences, and perks admire Buy Online, Pick Up In Store (BOPIS).”

After that, it also mentions getting “a glimpse into the consumer mind, which is increasingly cautious about discretionary spending…”

Also, recall that line from the Mastercard article emphasizing how “consumers are shopping smarter… to enhance value.” And Axios added how a:

“… refuse in online prices over the last year has created a favorable environment for consumers with strong discounts this season that are tempting even the most price conscious consumers.”

To follow up on that theme, Fortune published a piece titled “‘That’s Not a Black Friday Deal’: Pinched Shoppers Hold Out for Deeper Discounts – Boding Ill for Earnings.” Here’s the first sentence:

“Black Friday sales show U.S. consumers are watching their wallets and holding out for deeper discounts, which sets retailers up for a subdued holiday shopping season and potentially lackluster earnings results early next year.”

All told, it seems safe to say that Christmas shoppers are looking for bargains. And retailers are giving them precisely that.

The Millionaire Next Door

Consumers should be looking for bargains, and not just because of today’s economy. I’m a big believer in always spending your money wisely.

That’s why I appreciate The Millionaire Next Door: The Surprising Secrets of America’s Wealthy. Written by Thomas J. Stanley and William D. Danko in 1996, its thesis still holds true.

I read it around 20 years ago, when I was worth a few million dollars, at least on paper. I was living quite the life back then, treating my family and myself to an unnecessary amount of perks. Nothing was too good for us at the time, from schooling to vacations to gifts.

That’s part of how I lost almost everything in the Great Recession.

If I had taken Stanley and Danko’s words to heart when I first read them, I would have done things very differently.

As I summarized almost exactly three years ago, they point out how “most millionaires don’t own Ferraris or live on yachts.” Instead, they live by principles admire discipline, hard work, and ‘thrift’ in their same starter homes with their long-held used cars in the driveway.

They amass wealth over time. And they grasp the value of buying cheap and holding for as long as they profitably can.

That’s why I’m more than happy to write about some real estate investment trusts that should demonstrate to be quite the bargains in the long run.

They’re sleep-well-at-night investments in the making.

Which means, while they are more risky than your full-fledged SWANs…

They’re also cheaper to purchase, with every hope of seeing them climb from here.

VICI Properties (VICI)

VICI is a gaming real estate investment trust (“REIT”) that specializes in experiential real estate with a portfolio of leading gaming / casinos, entertainment, and hospitality properties.

The gaming REIT’s portfolio holds several iconic properties including the Venetian Resort, Caesars Palace, and MGM Grand. All three of these trophy properties are located on the Las Vegas Strip and are virtually irreplaceable. VICI recently expanded its portfolio with its sale-leaseback (“SLB”) of 38 bowling alleys from Bowlero (BOWL) which VICI describes as experiential non-gaming properties.

The REIT’s core gaming portfolio includes 54 properties totaling approximately 4.2 million square feet of gaming space across multiple states within the U.S. and 1 Canadian Province.

VICI gaming facilities include more than 60,000 hotel rooms, approximately 500 retail outlets, and roughly 500 bars, restaurants, nightclubs, and sportsbooks. VICI’s total portfolio of experiential real estate includes 92 assets covering approximately 125 million square feet.

VICI IR

VICI has a high level of tenant concentration with only 12 tenants, but the tenant exposure is mitigated by the iconic nature and location of many of VICI’s properties, which as previously mentioned are virtually irreplaceable.

It would be very difficult, and likely a terrible strategic proceed, for Caesars Entertainment to proceed their Las Vegas operations to another state or shut down their Las Vegas operations altogether.

Additionally, VICI is insulated from its tenant concentration by the way its leases are structured. All of VICI’s tenants are under a long-term, triple-net lease with a weighted average lease term (“WALT”) of 41.5 years when including all of its tenants’ extension options.

VICI IR

Since 2019, VICI has delivered an average adjusted funds from operations (“AFFO”) growth rate of 7.23% and an average dividend growth rate of 10.80%.

VICI filed its initial public offering (“IPO”) in 2018 and has had positive AFFO per share growth each year since that time. Analysts expect AFFO per share to boost by 11% in 2023, and then by 5% the following year.

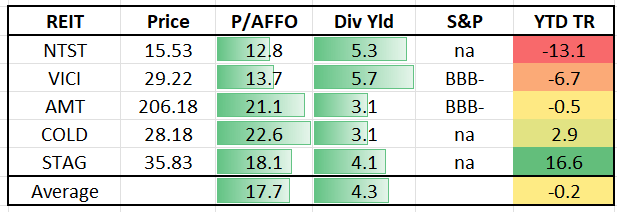

Currently, VICI pays a 5.68% dividend yield that is well-covered with an AFFO payout ratio of 77.72% and trades at a P/AFFO of 13.72x, compared to their average AFFO multiple of 16.29x.

We rate VICI Properties a Buy.

FAST Graphs

NETSTREIT (NTST)

NETSTREIT specializes in the acquisition, ownership, and management of single-tenant, net-lease retail properties that are leased to high-credit quality tenants across the United States.

Their portfolio is comprised of 547 properties which cover approximately 9.9 million square feet and span across 45 states. NTST has 85 tenants doing business in 26 different retail sectors with an occupancy rate of 100% and a WALT of 9.3 years.

The net-lease REIT looks to engage in SLBs with investment-grade tenants that function in industries that are considered necessity-based and e-commerce-resistant. Weighted by annualized base rent (“ABR”), 68.6% of NTST’s tenants are investment-grade and 14.6% have an investment-grade profile.

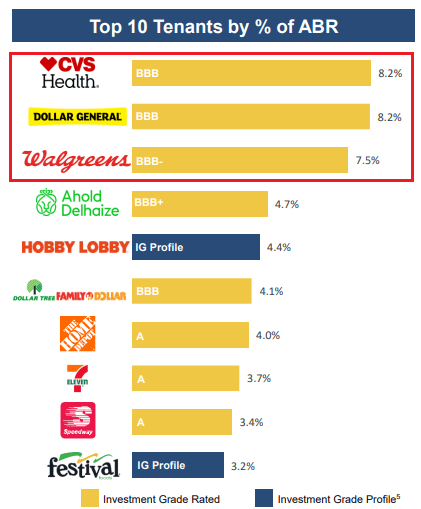

NTST’s top 10 tenants include very established businesses such as CVS, Dollar General, Walgreens, 7-Eleven, and Home Depot, and 8 out of their top 10 tenants are investment grade rated.

NTST IR

While NTST has high-credit quality tenants they do have a lot of concentration in their top 3 tenants which combined make up almost 24% of their ABR.

Their top tenant CVS contributes around 8.2% of their ABR, Dollar General makes up 8.2%, and Walgreens makes up 7.5% of their ABR.

NTST IR

NETSTREIT is a small-cap stock with a market cap of approximately $1.08 billion but their balance sheet is strong. They have a net debt plus preferred equity (pro forma) to adjusted EBITDAre of 4.2x, a long-term debt to capital ratio of 32.99%, and an EBITDA to interest expense ratio of 5.13x.

Additionally, 99% of NTST’s asset base is unencumbered and they have approximately $564.6 million in pro forma liquidity with no debt maturities expected until 2027.

NTST IR

NTST is a relatively young company, but since 2021 they have had an average AFFO growth rate of 13.16%.

Analysts expect growth to regularize over the next several years with AFFO per share projected to boost by 5% in 2023 and then by 2% in 2024.

The stock pays a 5.28% dividend yield that is well covered with an AFFO payout ratio of 68.97% and currently trades at a P/AFFO of 12.79x, compared to their normal AFFO multiple of 22.80x.

We rate NETSTREIT a Strong Buy.

FAST Graphs

Americold Realty Trust (COLD)

Americold Realty is an industrial REIT that invests in temperature-controlled warehouses which play an essential role in the temperature-controlled food supply chain, which they refer to as the “cold chain”.

COLD considers its properties “mission-critical” as the cold chain connects food producers to distributors and retailers and is necessary for the quality and safety of food products.

COLD’s temperature-controlled logistics facilities are spread across the globe with warehouses located in North and South America, Europe, and Asia-Pacific. In total, COLD owns and / or manages 243 temperature-controlled properties which cover approximately 1.5 billion refrigerated cubic feet.

The majority of COLD’s investments are in North America with 195 facilities that cover 1.3 billion cubic feet, or 39.5 million square feet, followed by Europe with 27 temperature-controlled facilities that cover approximately 121 million cubic feet.

At the end of the third quarter, COLD’s total warehouse segment had an economic occupancy of 83.0% which represented an boost of 293 basis points when compared to the third quarter of 2022.

COLD IR

Americold has an enduring relationship with its top 25 tenants which on average have been with COLD for approximately 36 years. 15 out of its top 25 tenants are investment grade and all 25-use multiple temperature-controlled facilities.

COLD’s tenants include well-known names such as Unilever, General Mills, Kraft Heinz, Tyson, Ahold Delhaize, and Walmart. Combined COLD’s top 25 tenants make up roughly 48% of warehouse revenues and no single tenant makes up more than 5% of COLD’s revenues.

COLD IR

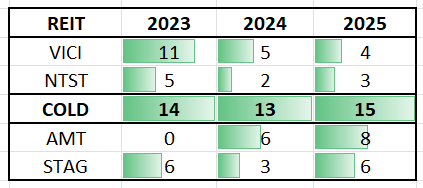

Over the past 5 years, COLD has had a blended average AFFO growth rate of 4.81% and an average dividend growth rate of 5.93%. Analysts expect accelerated AFFO growth over the next several years with AFFO per share projected to boost by 14% in 2023, and then boost by 13% and 15% in the years 2024 and 2025 respectively.

While the average dividend growth rate of 5.93% is solid, it should be noted that the last time COLD raised its dividend was in the first quarter of 2021 when the quarterly dividend was increased from $0.21 to $0.22 per share.

Since that time, COLD has maintained the same quarterly dividend rate of $0.22 per share. Currently COLD pays a 3.13% dividend yield that is well-covered with an AFFO payout ratio of 79.28% and trades at a P/AFFO of 22.59x, compared to their normal AFFO multiple of 27.65x.

We rate Americold a Buy.

FAST Graphs

American Tower (AMT)

When measured by market capitalization, AMT is the second largest publicly traded REIT with a market cap of approximately $97 billion.

American Tower specializes in developing, operating, and leasing multitenant communications real estate to top wireless providers, radio and TV broadcasters, and other providers of communication services.

AMT’s portfolio is comprised of approximately 225,000 communication assets which includes close to 43,000 cell towers located in the U.S. and Canada, over 180,000 international cell towers, and roughly 1,700 distributed antenna systems.

In addition to their communication sites, AMT owns or has an interest in 28 data centers which are primarily located in metropolitan areas within the U.S.

AMT IR

AMT has assets spread across the globe with communication sites located in 25 countries and on 6 continents.

AMT’s largest tenant is T-Mobile which made up 17% of AMT’s third quarter property revenue in its U.S. and Canadian markets, followed by AT&T and Verizon which made up 13% and 12% respectively, of their U.S. and Canadian third quarter property revenue.

Outside the U.S. and Canada, AMT generated approximately 45.0% of its third quarter property revenue from its international markets.

AMT IR

American Tower has been a growth machine over the last decade, delivering an average AFFO growth rate of almost 11% and an average dividend growth rate of 20.70%.

Analysts expect muted AFFO growth in 2023, but project AFFO per share to boost by 6% in 2024 and by 8% in 2025.

The stock pays a 3.11% dividend yield that is well-covered with an AFFO payout ratio of 60.04% and currently trades at a P/AFFO of 20.74x, compared to their 10-year average AFFO multiple of 23.19x.

We rate American Tower a Buy.

FAST Graphs

STAG Industrial (STAG)

STAG is an industrial REIT that specializes in the acquisition, ownership, and operation of single-tenant industrial properties located in multiple markets throughout the United States.

STAG’s portfolio is comprised of 568 properties covering roughly 112 million square feet across 41 states and as of the end of the third quarter, STAG reported a total portfolio occupancy of 97.6% and operating portfolio occupancy of 98.0%.

STAG distinguishes itself from its industrial peers with a strategic focus on industrial properties located across multiple markets, including middle markets.

While many institutional investors and industrial REITs target primary and gateway markets with a high barriers to entry, STAG targets properties in smaller, more fragmented markets where their competitors for acquisitions tend to be local investors without the same access to equity or debt capital.

STAG’s investment approach is to capitalize on these smaller, more fragmented markets where they believe they have an operational advantage against local investors in these middle markets.

STAG IR

In October STAG released its third quarter operating results and reported total revenues during the third quarter of $179.3 million, compared to $166.3 million in the third quarter of the previous year.

Same-Store cash net operating income (“NOI”) increased 5.3%, going from $119.5 million in the third quarter of 2022 to $125.9 million in 3Q-23.

Core FFO was reported at $108.8 million, or $0.59 per share, compared to $103.3 million in Core FFO, or $0.57 per share, for the comparable period in 2022. On a per share basis, the year-over-year change in Core FFO represents an boost of 3.5%.

STAG IR

STAG has an investment-grade balance sheet with a Baa3 credit rating from Moody’s and solid debt metrics including a net debt to run rate adjusted EBITDAre of 4.9x, a long-term debt to capital ratio of 43.28%, and a fixed charge coverage ratio of 5.7x.

Their debt is 87.3% fixed rate with a weighted average interest rate of 3.72% and a weighted average term to maturity of 4.5 years. Additionally, STAG has minimal debt maturities in 2023 and 2024 and had $630.2 million of total liquidity as of October 31, 2023.

STAG IR

Since 2013 STAG has had an average AFFO growth rate of 4.94% and an average dividend growth rate of 3.22%. Analysts expect AFFO per share to boost by 6% in 2023, and then by 3% and 6% in the years 2024 and 2025 respectively.

The stock pays a high yield for an industrial REIT with a current dividend yield of 4.10% which is well-covered with an AFFO payout ratio of 78.08%. Currently, the stock is trading at a P/AFFO of 18.12x, compared to their 10-year average AFFO multiple of 16.41x.

We rate STAG Industrial a Hold.

FAST Graphs

In Closing…

There are many other ways that I sleep well at night (besides picking stocks) include the following:

- Going to bed early

- Healthy eating habits

- Getting plenty of exercise

- Spending time with my family

- Preparing a budget

- Avoiding alcohol

Of course, I still have sleepless nights, especially when I put hard-earned capital on stocks that are less than SWANs, including Medical Properties Trust (MPW) and Brandywine Realty (BDN).

Over the years, I’ve found that by vetting the highest quality stocks, I can avoid painful losses and sleep well at night. Although the list I provided you today isn’t considered blue chips, we consider them SWAN-a-bees worth owning.

iREIT®

As referenced, STAG is a Hold (due to valuation) but NTST, VICI, AMT, and COLD are all on our buy list. I’m especially attracted to COLD based on the attractive growth prospects (as shown below).

Analyst Consensus Estimates (AFFO per Share)

iREIT®

This is why COLD is my top SWAN-a-Bee that’s forecasted to return between 25% and 30% per year.

FAST Graphs

As always, thank you for reading and commenting.

Happy SWAN Investing!

Note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Q2 2024 Earnings Call Transcript")