Darren415

Welcome to another installment of our CEF Market Weekly Review, where we converse closed-end fund (“CEF”) market activity from both the bottom-up – highlighting individual fund news and events – as well as the top-down – providing an overview of the broader market. We also try to supply some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the fourth week of November. Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

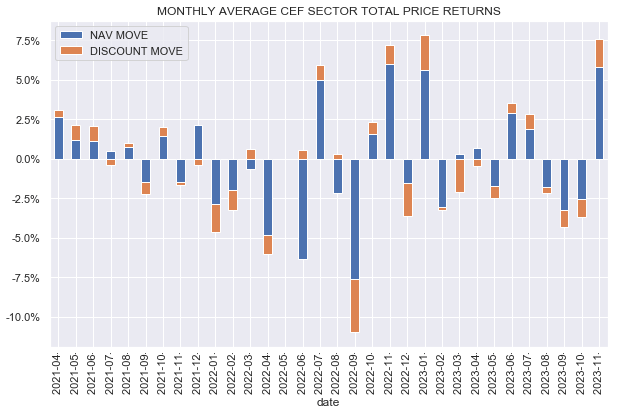

It was another good week for the CEF sector, as the market is enjoying relatively upbeat earnings and a likely end to the Fed hiking cycle. Utilities and REITs – two sectors very sensitive to interest rates – finished in the guide.

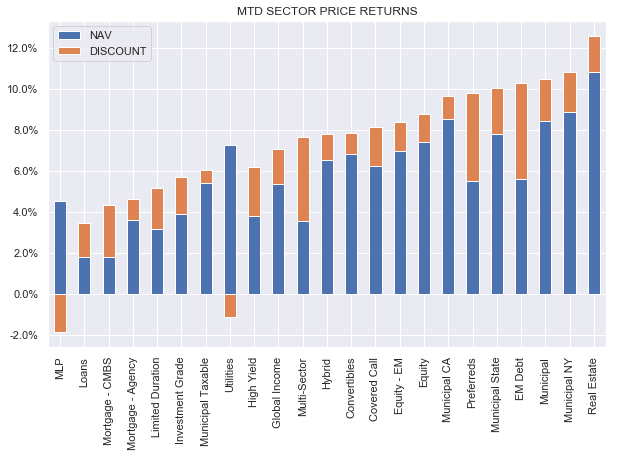

Month-to-date, five sectors are sporting double-digit returns.

Systematic Income

November is close to being the best month over the last 2+ years.

Systematic Income

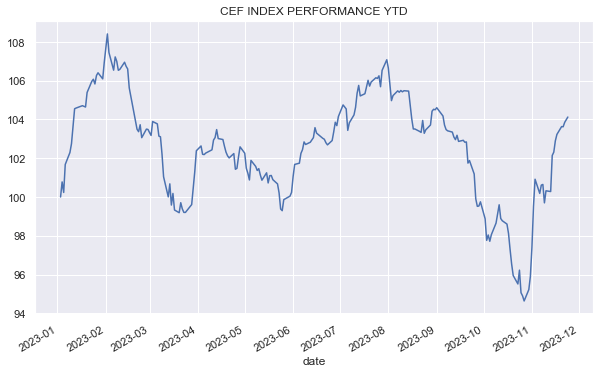

The recent bounce brought the CEF space into the green year-to-date.

Systematic Income

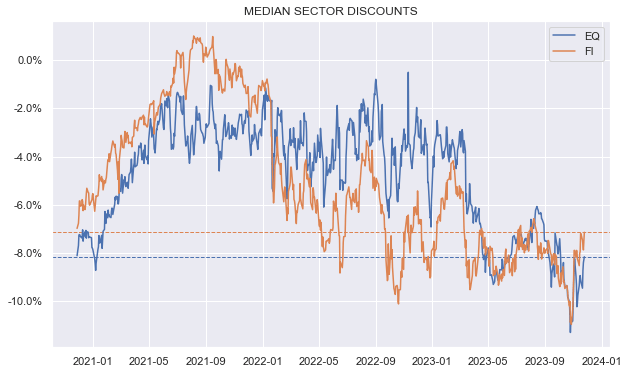

Although both fixed-income and equity CEFs have tightened somewhat in November, equity CEF discounts, in particular remain quite wide.

Systematic Income

Market Themes

BlackRock has redeemed a big chunk of its variable-rate term preferred shares across 9 Muni CEFs. The proportion is very high – around 40%+. The preferreds make up nearly all the leverage (i.e. borrowings / liabilities) for these funds.

It’s not clear whether the preferreds will be replaced by something else – some of the funds in question have a small amount of tender option bonds which can be used as well and are cheaper than the preferreds.

The timing suggests the funds were forced to deleverage. The jump in rates at the end of October pushed up leverage to likely uncomfortable levels. Longer-term rates hit a recent peak (at least since 2007) on 31-Oct, which neatly coincides with the 2-Nov announcement date.

A deleveraging has two implications for the funds – for income and for returns. Let’s focus on the income portion, as the impact on future returns is a theme we have discussed many times.

Because a given fund now has fewer assets (a deleveraging requires the fund to sell assets in order to raise cash to redeem the liabilities), it has less investment income. However, recall that in a deleveraging the fund also sheds borrowings, which reduces the fund’s interest expense. Furthermore, the fund no longer accrues a management fee on the sold assets, which advance mitigates the drop in investment income.

Net income on leveraged assets is roughly investment income – leverage cost – management fee.

Each Muni CEF is different, however a rough idea for investment income is the S&P Long Intermediate TErm Taxable Municipal Bond Index, which has a yield of 5.4%. For leverage cost, we can use the monthly numbers published by the large Nuveen CEF Quality Municipal Income Fund (NAD) of 4.57%. Finally, we can use a management fee (including sundry expenses) of 0.6% which is roughly what these funds charge.

Once we plug everything in, we get to 0.23%. In other words, by deleveraging, Muni CEFs are getting rid of assets that were contributing a negligible amount of additional yield to the fund. In fact, it’s mathematically possible that some of the funds, particularly those with relatively high leverage costs or relatively low-yielding assets (perhaps because they are higher-quality than the index) saw an boost in net income from a deleveraging. In short, from the perspective of net income, this is not a big deal.

Market Commentary

The MFS High Yield Municipal Trust (CMU) completed its tender offer. 10% of the fund’s shares were bought back at $3.32 (98% of NAV in 6-Nov) which is 15% above the $2.89 price on the day. Oddly, only 25% of shares were tendered – well below the typical run rate of close to 50%. This is excellent news for shareholders who were able to get a much higher prorated amount of close to 40% from 10% had everyone tendered.

Obviously, shareholders who want to preserve the previous level of CMU shares could repurchase their shares near $3 where the fund was trading shortly after the tender – a great roundtrip. This, once again, highlights the lack of efficiency in the CEF market, which continues to reward high-information investors.

Elsewhere, the Allspring (formerly Wells Fargo) Income Opportunities Fund (EAD) – a high-yield corporate bond CEF – updated its managed distribution policy. Previously, the fund had a managed distribution policy of 8% of the trailing 12-month NAV.

This may have made sense when bond yields were lower, however it makes less sense now when High Yield corporate bond yields are above this figure. The distribution multiplier was raised from 8% to 8.75% or a 9% rise in the distribution. This hike should guide to discount outperformance over the medium term. The fund has outperformed the sector on a total NAV basis across various longer-term periods. It remains in the High Income Portfolio.

Stance and Takeaways

CEFs enjoyed a nice run through November. What is important for the second leg of the rally is not just a pause in the Fed stance but a series of rate cuts, however. Rate cuts can happen in two different environments – an onset of a recession that saps demand and drives inflation down or continued disinflation in response to healing supply chains and a rebalancing in consumer demand. These two outcomes can be fairly called hard landing and soft landing, respectively.

A soft landing environment is much more likely to guide to tighter discounts, whereas a hard landing is more likely to push discounts wider from current levels. A hard landing would also likely drive NAVs lower for most funds, even if longer-term interest rates fall from current levels.

A hard landing environment of wider discounts and lower NAVs, perhaps counterintuitively, would make CEFs much more attractive than they are today, particularly as net income would advance higher as a result of lower leverage costs. For that reason, it makes sense to preserve some dry powder in the form of relatively resilient securities that investors could put to work in that eventuality.

At the moment, we continue to admire funds admire the CLO Equity Carlyle Credit Income Fund (CCIF) and the PIMCO Dynamic Strategy Fund (PDX), among others.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")