Man celebrating expected FFO growth after 5 years of declines.

lucigerma/iStock via Getty Images

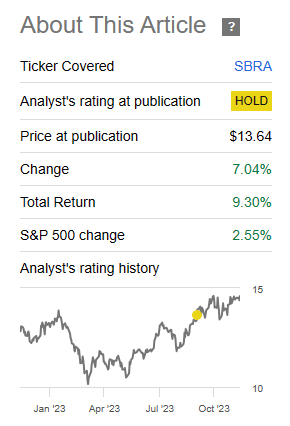

On our last coverage of Sabra Health Care REIT Inc. (NASDAQ:SBRA), we pointed out the issues with the company, and told you why we were not buying the 9% yielder.

We see the company as one of the weaker players in the space and don’t think the current price offers a compelling entry point. Yes the large dividend yield looks tempting, but it is really about considering the total returns investors have gotten from the company. More importantly, the bulk of the price loss over this timeframe was due to FFO declines and not due to a multiple compression. We rate this a hold while giving it a 6 on our potential pain scale at this price.

Source: A 9% Yielding Healthcare REIT

The stock proved to be one of the more resilient ones in the REIT sector and investors are probably unhappy at missing out on the up advance.

Seeking Alpha

Of course, we have maintained this negative stance for a long time and over the past few years, SBRA has not given investors much cheer. But things are indeed looking up for the sector. There are some good tailwinds for the REIT and today we will go over what the bull case could appreciate for 2024. We will also tell you where the better risk-reward lies if you want to play the rebound.

Q3-2023 & Outlook

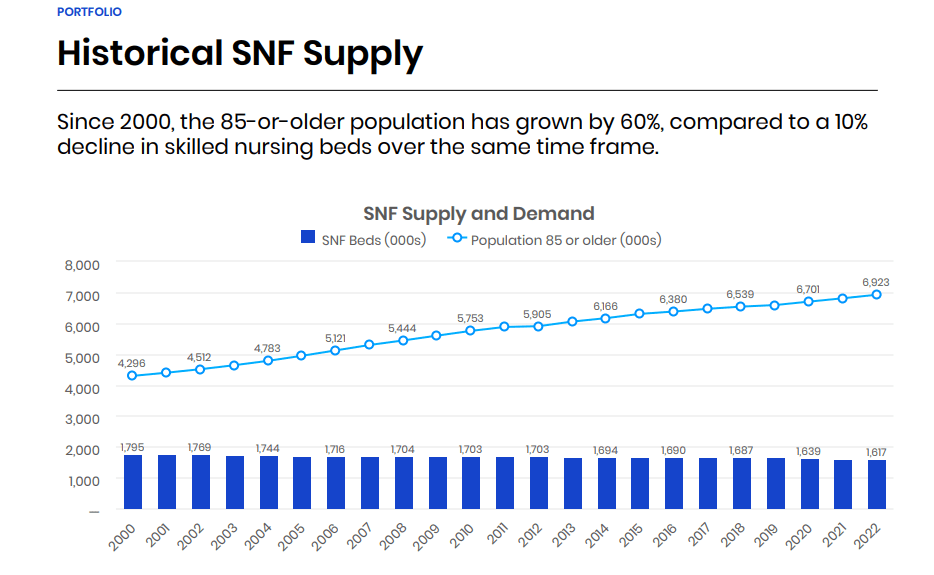

Senior housing and skilled nursing sectors took it on the chin during COVID-19 and it created a perfect storm for the sector. The three years were filled with crisis on multiple fronts including a high level of mortality in the elderly population, high supply from earlier construction starts and a very high level of inflation in wages. But we have begun to see all three recede and advance in the opposite direction. COVID-19 related mortality is now a past issue and the number of boomers retiring is quickly filling the demand gap. New constructions have fallen off and supply is slowly coming to a crawl in senior housing. On the skilled nursing side, available beds have been declining for some time and the REIT’s tenants will likely savor better pricing power on the private side.

SBRA Q3-2023 Information

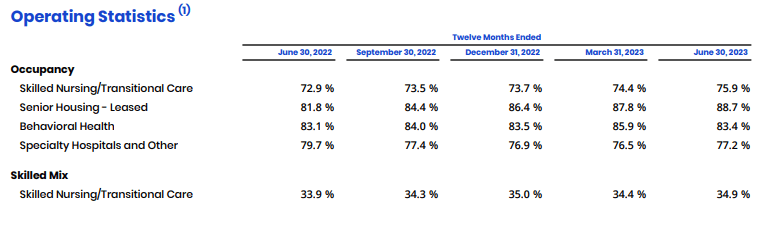

Wages have moderated. On SBRA’s portfolio we can see the small green shoots in the occupancy levels which have trended higher.

SBRA Q3-2023 Information

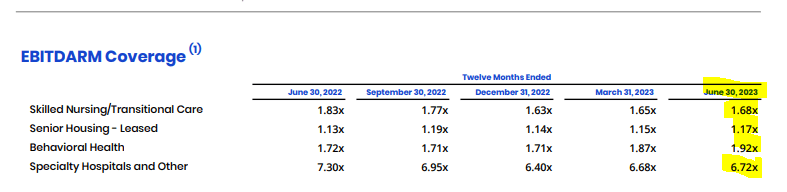

Skeptics may point to the EBITDARM (earnings before interest, taxes, depreciation, amortization and management fees) coverage of tenants still looking weak.

SBRA Q3-2023 Information

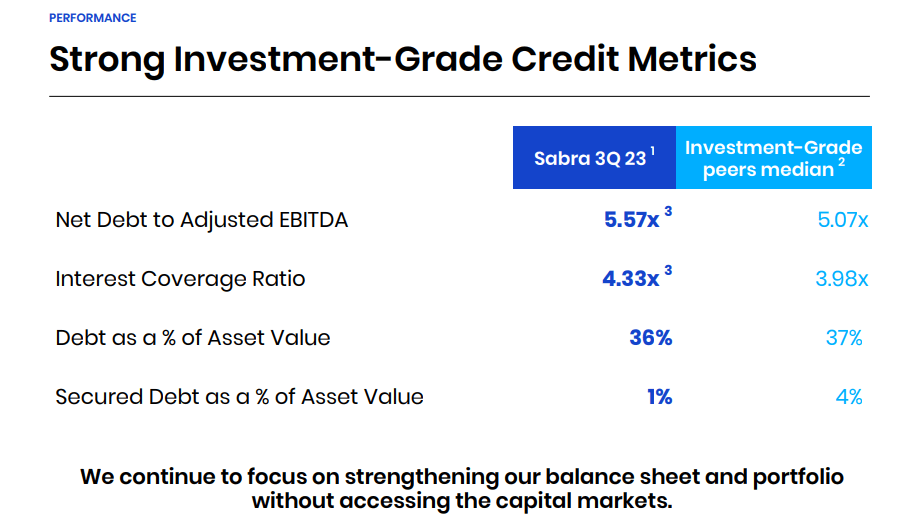

That is certainly true, but these better with a lag and since this is a trailing 12-month measure, you won’t see it here until well into 2024. More importantly for SBRA, it is actually in a good position to take advantage of it. Unlike some REITs that played fast and loose with their credit, SBRA has actually maintained a rather clean balance sheet.

SBRA Q3-2023 Information

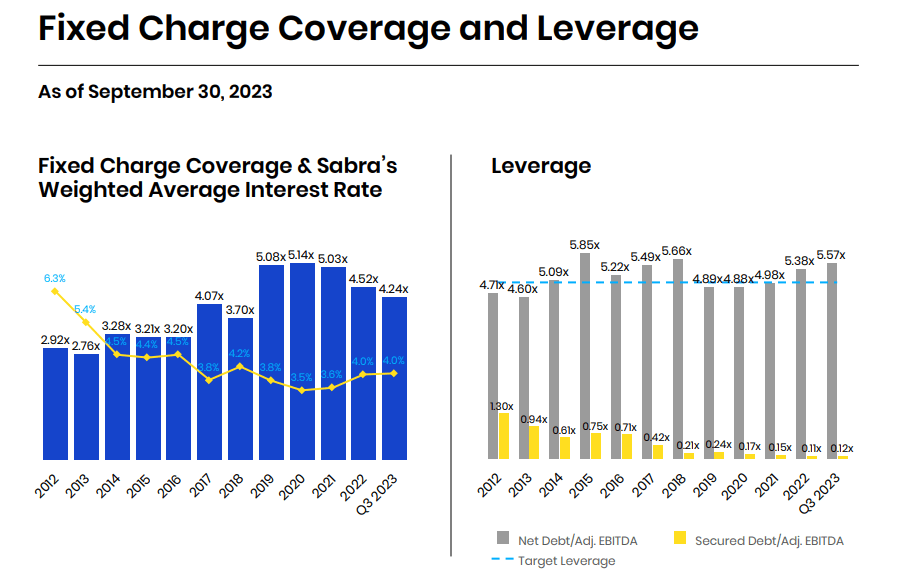

Fixed charge coverage did trend down from 2020, but remains rather robust at 4.24X.

SBRA Q3-2023 Information

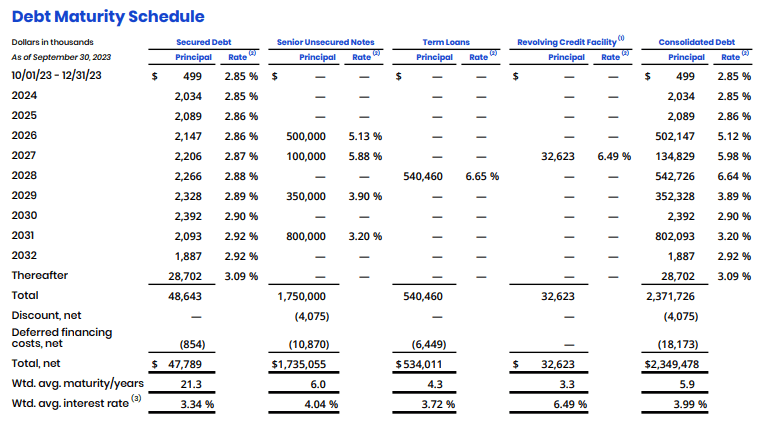

The debt maturity profile is superlative and there is no big refinancing until 2026. The 2026 and 2027 maturities are also at relatively high interest rates so refinancing will not be a big burden on funds from operations (FFO).

SBRA Q3-2023 Information

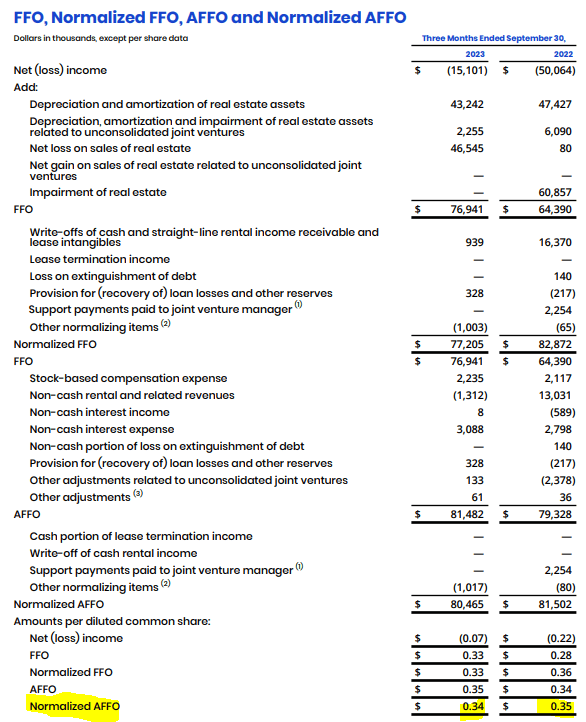

Speaking about FFO and adjusted FFO (AFFO), the REIT showed yet another quarter of declining normalized AFFO year over year.

SBRA Q3-2023 Information

This has been a thorn in the side of the bull case and SBRA’s AFFO has declined from over $2.00 a share (2018) down to $1.36 now (expected 2023). But as it stands, FFO should grow in 2024, albeit off a low base. Analysts have always been predicting growth every single year and then have had to backtrack around mid year. So in that sense, 2024 does not sound any different than the past few years. But we believe that the coming year actually has a good chance of proving the analysts correct for once. So you are looking at about a 3-4% growth and then you add the 8.22% dividend yield, and suddenly you are excited about the stock.

Look For Value

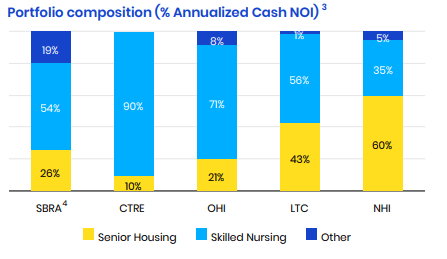

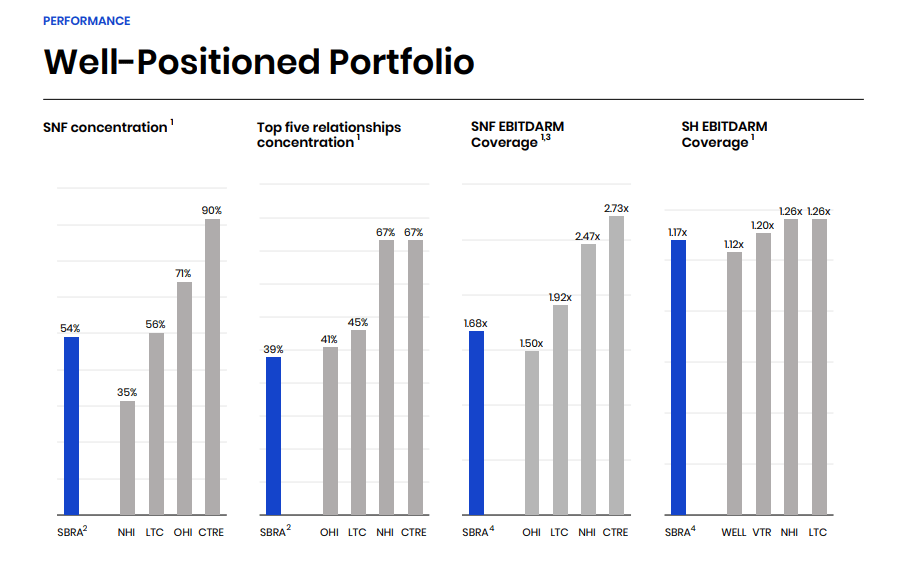

While there is a legitimate case for some upside here, we would still be skeptical that the long term trends here have been firmly reversed. What bothers us most about this sector is that the underlying tenant health has been extremely poor. Having EBITDARM coverages near 1.2X is essentially what we are referring to. That poor level of rent coverage (after you exclude every single relevant expense) is not found anywhere else in the REIT space. Even if you “buy” the bull case, let us tell you why we think National Health Investors, Inc. (NHI) is a superior pick here.

NHI does bear a lot of similarity to SBRA and even SBRA throws in this one as a comparative in presentations.

SBRA Q3-2023 Information

We actually appreciate the NHI leaning on senior housing versus skilled nursing as the latter is still struggling with Medicare reimbursement issues. For the skilled nursing that both have, NHI has far better rent coverage from its tenants (2.47X vs 1.68X). Senior housing rent coverage is similar.

SBRA Q3-2023 Information

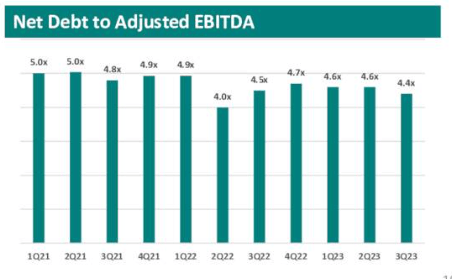

NHI has held up its FFO far better in the 2018 to 2023 timeframe (20% reject versus over 35% for SBRA). NHI is also running leverage at 4.4X EBITDA versus 5.57X for SBRA.

NHI Q3-2023 Presentation

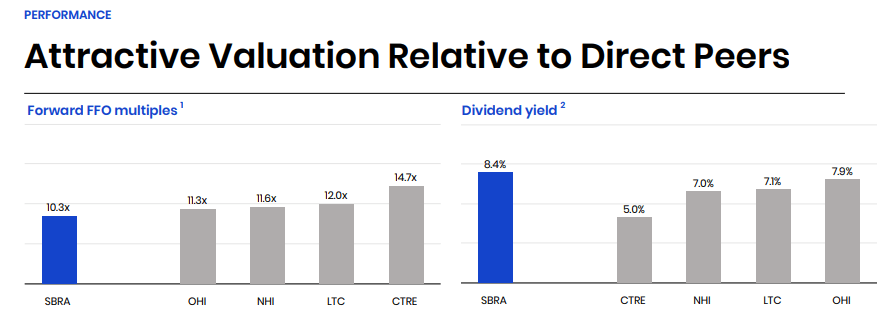

On a price to NAV basis, both stocks are trading at about 10% over consensus NAV. So neither side gets an advantage there. SBRA does sport a higher dividend yield and also a slightly lower FFO multiple.

SBRA Q3-2023 Information

We think this will not sway the overall outcome much in terms of returns. We would continue avoiding SBRA and consider NHI as a play on the sector.

Q2 2024 Earnings Call Transcript")