hapabapa

Workday, Inc. (NASDAQ:WDAY) just reported its third quarter results for the current fiscal year, and the initial reaction was to say the least a very positive one.

The stock jumped 11% on the day following the release, as Non-GAAP Earnings Per Share came in at $1.53 when analysts were expecting $1.41. To be fair, this is not an unusual event for the company, as earnings surprises for the past 1-year have been much higher.

Seeking Alpha

Once again, we should not overlook that we are still dealing with Non-GAAP numbers here, and all the positive news come with strings attached for long-term investors.

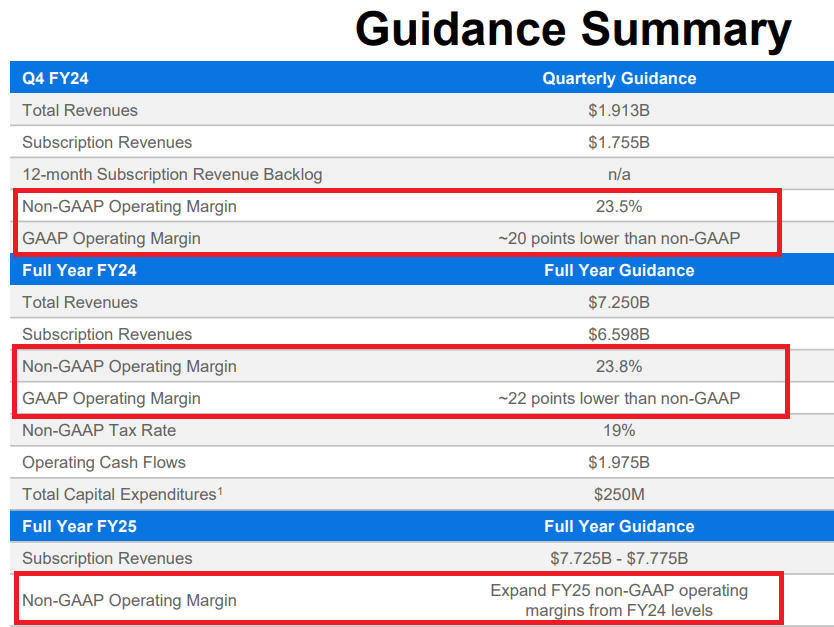

Nonetheless, Workday’s management has also upgraded its guidance for the full fiscal year to be at the top-end of the range, with Non-GAAP operating margin expected to come in at 23.8%, up from 23.5% previously guided.

As a result, sell-side analysts are now in a rush to upgrade their ratings and adjust their future estimates.

Seeking Alpha

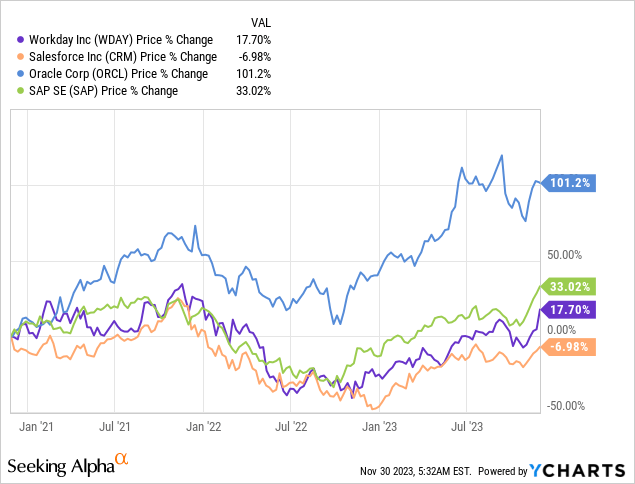

In the coming days and weeks, this is likely to give Workday’s share price a boost and might even be enough to close the performance gap with one of its major peers – SAP SE (SAP).

Over the past 3-year period, however, WDAY has not delivered an outstanding shareholder returns, in spite of the strong industry-wide tailwinds on the back of increased digitalization and adoption of cloud-based Human Capital Management (HCM) and Enterprise Resource Planning (ERP) suites.

Beyond the very immediate future, I see a twofold problem for Workday and I expect the stock to continue to underperform its peers in the coming years. The first problem is associated with Workday’s ability to preserve its growth and the company’s competitive positioning and the second one is directly linked to achieving high and sustainable GAAP profitability.

Growth And Competitive Positioning

The first major problem for Workday is related to sales growth and the company’s inferior competitive positioning against its direct peers.

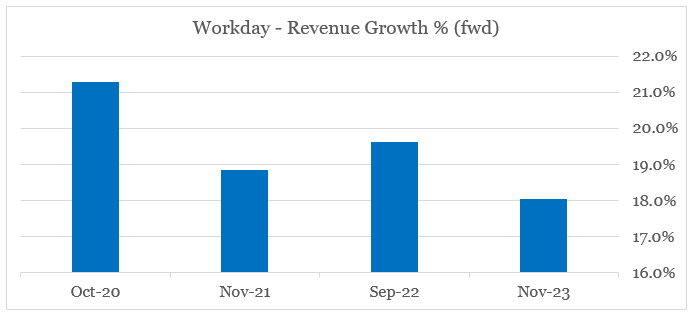

In the near-term, Workday is expected to retain a revenue growth rate of around 18%, which is impressive. As of October of 2020, the company’s sales were expected to grow at around 21%, which although higher is not materially different from the currently expected growth rate.

prepared by the author, using data from Seeking Alpha

For the upcoming fiscal year ending in January of 2025, Workday’s management expects its subscription revenues, which represent the majority of sales, to boost within the range of 17% to 18% on an annual basis.

Workday Investor Presentation

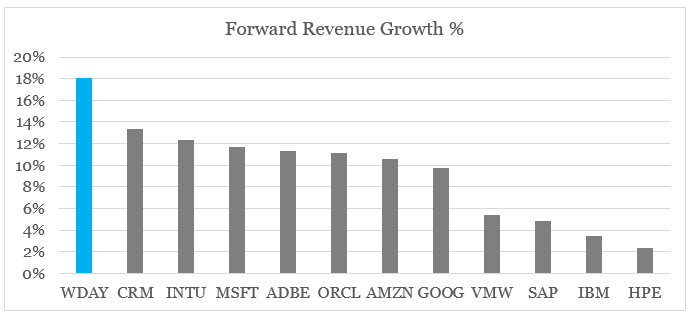

This has now given investors a piece of mind that the company continues to win business and that it is so far immune to the slowing growth rates within the cloud space. The fact that WDAY is also one of the highest-growth companies in its expanded peer group is more than enough to uphold the company’s premium valuation for the time being.

prepared by the author, using data from Seeking Alpha

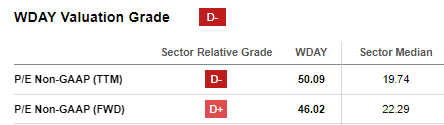

With a Non-GAAP forward Price/Earnings multiple, Workday has one of the highest premiums within the broader peer group above, but as long as the high top line growth rate could be sustained the risk of a multiple contraction remains low.

Seeking Alpha

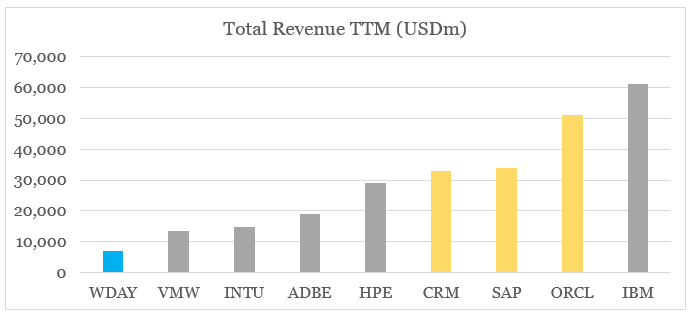

The expectation is that at such a high revenue growth rate, the company would be able to reach high GAAP profitability, before it enters a more mature growth phase. This scenario is appealing enough for most investors, given Workday’s much smaller size to its broader peer group and more importantly to its direct competitors marked in yellow on the graph below.

prepared by the author, using data from Seeking Alpha

Having said that, it is exactly this much smaller size that will be a major obstacle for Workday’s competitiveness going forward. As I elaborated in advance detail a couple of months ago, Workday’s service offerings and the breadth of its ecosystem is very limited in comparison to the likes of Salesforce, Oracle and SAP.

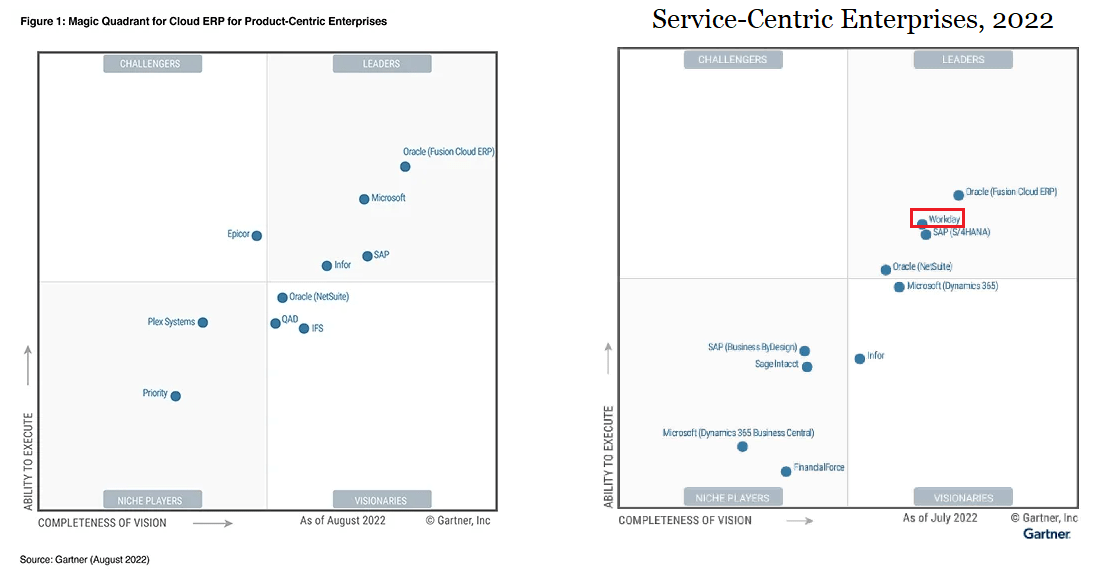

In the ERP space, for example, Workday is among the leaders when it comes to service-centric enterprises, but contrary to Oracle and SAP is nowhere to be found for product-centric enterprises (the left-hand quadrant below).

Gartner

In HCM Suites, Workday is toe-to-toe with the leader Oracle, but SAP and Ceridian HCM Holding (CDAY) are very close within Gartner’s rankings.

In addition to the lower total addressable market and the limited ability for economies of scale, differentiation is another key issue associated with Workday’s more limited ecosystem. As of late, it has become apparent that generative AI would be a major differentiation factor for cloud-based services and Workday’s peers are taking advantage of this opportunity.

Next week, we have Oracle CloudWorld, which will showcase the latest innovations, including AI on OCI, the progress of Oracle Autonomous Database, our multi-cloud strategy, the use of Oracle Analytics throughout our portfolio to drive better decision-making and the use of generative AI to differentiate Fusion, NetSuite and our industry application.

Source: Oracle Q1 2024 Earnings Transcript (emphasis added).

The major competitive advantage here is about having more data to train these AI models and execute more functionalities across the whole service offering. As we saw in the extract above, Oracle is in a very good position here given its strong SaaS and database ecosystem. Salesforce’s recent large acquisitions are also now giving the company a significant advantage in this field.

(…) Einstein with predictive and generative combined, is doing 1 trillion transactions a week, that’s amazing. But more amazing is that 17% of the Fortune 100 are now Einstein GPT Copilot customers. And this is a product that is just coming to market. Everyone is so excited about buying this product.

Source: Salesforce Q3 2024 Earnings Transcript (emphasis added).

SAP is not far behind and the management has recently emphasized the importance of having enough consent from customers to use their data for AI use cases.

Earlier this year, we also introduced our business AI strategy to the market, bringing together our existing AI capabilities with the new potential of generative AI to modify how businesses run. We have already made a lot of progress over the last few months. We have consent from thousands of customers to use their anonymized data to evolve and train our AI use cases and foundational data model.

Source: SAP Q3 2023 Earnings Transcript (emphasis added).

Obviously, Workday is working on similar functionalities itself, however, at the end of the day the quality of generative AI depends on the amount of data available to train the model and as we saw above, Workday’s much smaller size and limited service offerings could end up being yet another major competitive disadvantage.

What About GAAP Profitability?

The second problem of WDAY builds upon the one presented in the previous section. It is related to achieving high and sustainable GAAP profitability, without risking to derail top line growth rate and shareholder returns.

The good news for WDAY and the reason why the company is likely to be an M&A target is that it already has one of the highest gross margins in the industry, which has increased even advance in most recent quarters.

prepared by the author, using data from Seeking Alpha

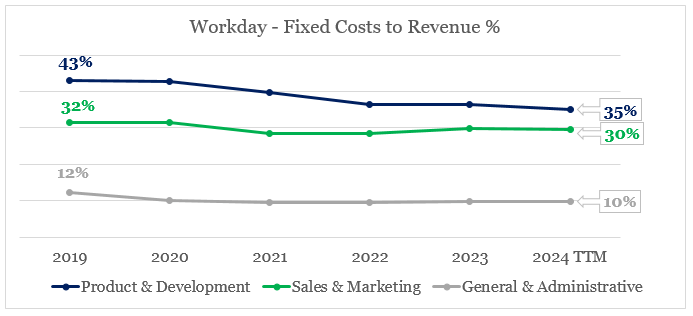

All else being equal, this should result in industry-leading operating and net margins as well, but the smaller size of the company does not allow for meaningful economies of scale to be realized. This is illustrated on the graph below, where we could see that all major fixed costs for Workday have been relatively stable as a share of the company’s growing revenue.

prepared by the author, using data from SEC Filings

Given the massive boost in WDAY’s top line figure since FY 2019, this lack of progress on the fixed costs side of the equation is troubling.

prepared by the author, using data from SEC Filings

Some progress has been made during all these years, however, as the company’s GAAP operating income/loss has changed from a loss of $438m in FY 2019 to a tiny profit of $15m during the past 12-month period. To a large extent, however, this has been a result of the gross margin boost we saw above and the company’s growing reliance on stock-based compensation (see the graph below). As a matter of fact, Workday’s share-based compensation has grown so much that it still represents the vast majority of the company’s cash flow from operations.

prepared by the author, using data from SEC Filings

As encouraging as the most recent quarterly results were, the guidance for FY 2024 does not include a meaningful improvement in GAAP operating margin and none was included for FY 2025.

Workday Investor Presentation

Conclusion

Given the strong business momentum and the upcoming sell-side analysts’ ratings upgrades, Workday, Inc. stock is likely to deliver strong risk-adjusted returns in the coming weeks. For anyone with a longer investment time horizon, however, future returns are at risk. On one hand, Workday is at a disadvantage to its larger peers and the management would have to demonstrate that it could preserve the current revenue growth rates beyond FY 2025. The issue of GAAP profitability is yet another risk factor for anyone looking to remain a WDAY shareholder in the long-run.

Q2 2024 Earnings Call Transcript")