reklamlar/iStock via Getty Images

Sprinklr (NYSE:CXM) is a company that develops SaaS for customer go through management across various channels, including social media. In the last four years, Sprinklr has been consecutively named in Gartner’s Magic Quadrant for Content Marketing Platforms, highlighting its capabilities in optimizing content management and maximizing client engagement. Unsurprisingly, CXM reported robust results in Q2 with total revenue of $178.5 million with an 18% YoY growth and subscription revenue of $163.5 million with a 23% YoY growth. Most of this success came after CXM’s capabilities synergized after extending AI services throughout its suite of solutions that allowed for enhanced customer experiences. In this context, CXM’s business appears robust with promising growth prospects, which leads me to deduce it deserves a premium relative to the rest of its sector. My valuation analysis suggests that CXM trades at a good price for new investors as long as they know the inherent risks.

Business Overview

Sprinklr Inc. is a company that produces Software as a Service [SaaS] for customer go through management in different channels, including social media, which encompasses marketing, advertising, collaboration, customer care, and monitoring. CXM is based in New York City, and it was established in 2009 with a successful IPO in June 2021. It currently has 3,511 employees.

For context, in March 2015, the company undertook its go through Cloud platform to ease brand interaction with different social media channels, enabling clients to engage with their customers. Then, in April 2017, CXM started eight new products integrated with its Cloud, including access to Twitter’s data platform, content marketing, research cloud with ratings and reviews, and social care. In April 2018, CXM advance improved its capabilities, adding an AI layer to its cloud platform to rank social posts related to client care. According to the company, 80% of customers contact the brands via social media.

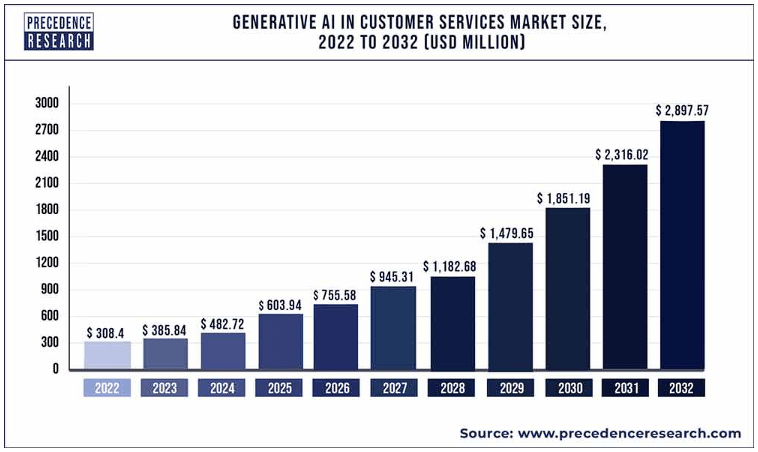

Precedence Research

The new AI layer, Intuition, could process over 700 million messages across 26 social platforms. Thus, what came about this confluence of technologies was a new way to holistically engage with customers through the initial awareness stages to the sale and customer maintain. It also fosters a new way of doing community management for brands. Overall, CXM developed a suite of functionalities vital for modern businesses, especially those that rely on social media.

A Holistic Approach To Customer go through

Moreover, in May 2022, AI services were extended to assist customer experiences using generative AI for conversational self-service with an impact assessment to exclude bias. The bots’ understanding is powered using the existing brand’s knowledge base of documents, with mechanisms to impede hallucinations using guardrails admire ethical and safety guidelines to decrease the risk of erroneous or unsavory answers. The bots also have voice enhancements for text-to-speech capabilities. These added capabilities humanize bots and make customer engagement and community management much more cost-efficient, increasing their effectiveness and lowering costs compared to bloated HR, Marketing, and Customer maintain teams.

Sprinklr also offers four product suites in its cloud platform with a single user interface, all AI-powered. CXM has the Contact Center as a Service [CCaaS]. This cloud-based platform allows companies to utilize contact center software hosted on a provider’s servers rather than maintaining the software on their internal infrastructure. The second product is marketing with campaigns, content workflows, advertising, and customer care automation. As you might expect, Sprinklr Insights also monitors results for brand content, detecting potential areas for improving ad and marketing effectiveness. Finally, Sprinklr Social customizes customer go through in social networks for clients and their customers.

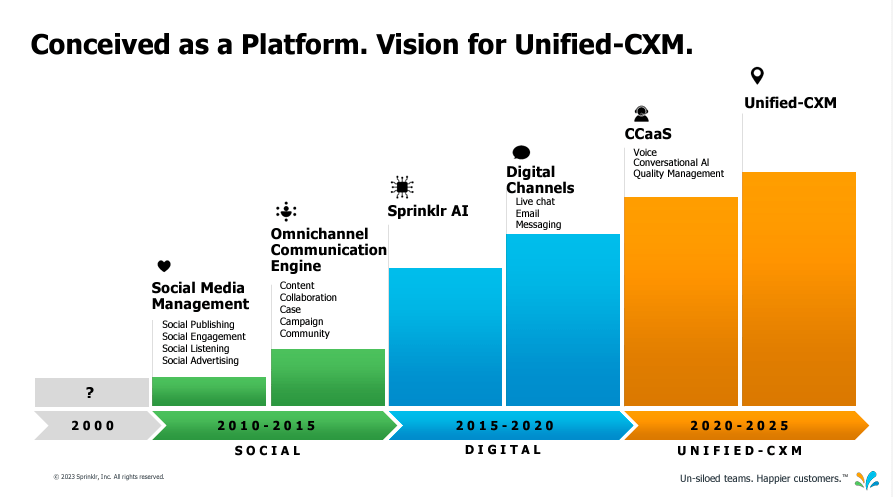

Source: 2024 Q2 earnings call presentation

Gartner’s Magic Quadrant uses a standard methodology to supply insights into a technology market direction. Accordingly, CXM was named again for the fourth year in the 2023 Gartner Magic Quadrant for Content Marketing Platforms. In 2023, CXM was recognized as a Challenger for its ability to overcome content marketing problems and enhance management to accomplish maximum client engagement for each piece of content produced. As such, CXM’s gamut of offerings is celebrated in the industry and appears highly cost-effective for brands and companies.

CXM’s Innovative AI and Market Strategies Fuel Growth

In CXM’s latest earnings call, management reported robust results in Q2 with total revenue of $178.5 million with an 18% YoY growth and subscription revenue of $163.5 million with a 23% YoY growth. The executives highlighted that integrating the Cloud’s Vertex AI includes generative AI with brand-level governance and security. With this new addition, CXM is focused on market expansion and specific solutions. With this objective, the company has made new key hires in service specialist teams to progress vertical solutions in various sectors. In the following years, the company aims to build a unified Customer go through (Unified-CXM) to incorporate the different aspects of managing customer interactions across diverse channels such as social media, chat, email, and phone calls.

In my opinion, three principal components are the key to the success of CXM’s products: the possibility of access to the platform and taking advantage of the intuitive and easy-to-use self-service option. This alternative allows CXM’s services to appeal to a broader audience, making it viable for smaller businesses to communicate directly with the software. I think this intuitive and accessible nature of CXM’s offerings drives adoption.

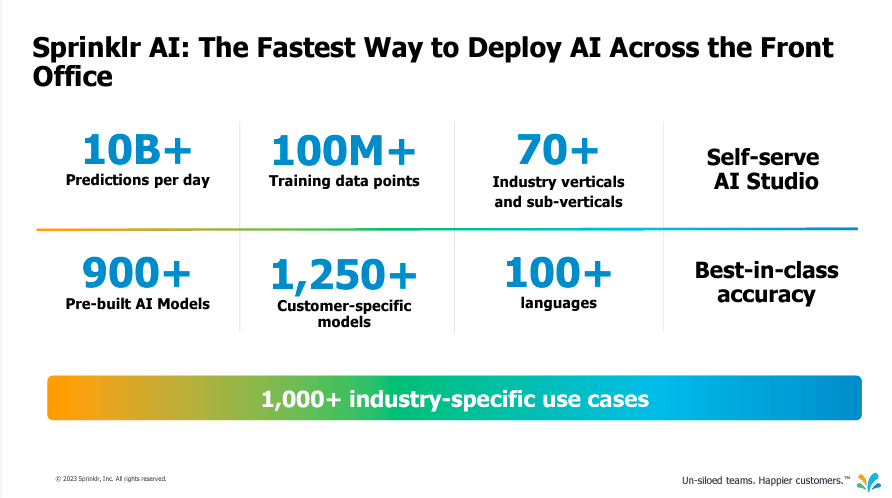

Source: 2024 Q2 earnings call presentation

Secondly, the key component of CXM’s success is the ability to take advantage of the ongoing trend of large customers consolidating solutions into CXM’s platform, growing large subscription revenues from top players in different sectors. Thirdly, the products are boosted by AI based on product expansions, enabling and optimizing the customer go through. This last AI layer is what I believe brings it all together, as it humanizes CXM’s services and can potentially disrupt existing community management approaches.

Premium For Quality: Valuation Analysis

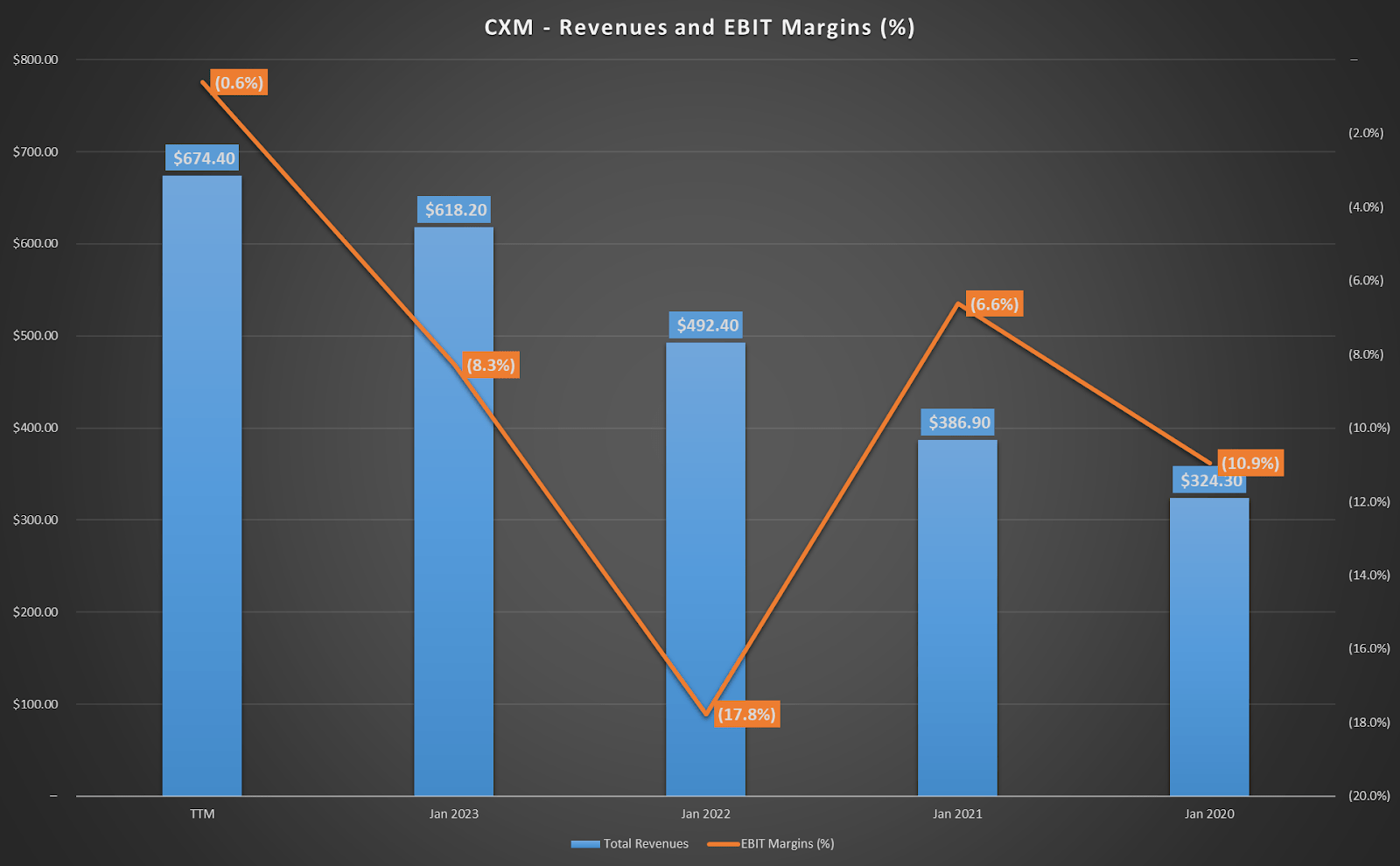

From a valuation perspective, the company is a rather straightforward analysis. As you might visualize, CXM’s revenues are consistently trending higher, especially after the latest wave of AI interest in 2023. Companies are now quickly realizing that AI will revolutionize and disrupt every aspect of business and society in the future, so integrating with this technology is paramount for their future. I assess its revenues have increased at a commendable CAGR of 24.0% since 2020, reflecting the success of its strategies and value proposition in the market.

Author’s elaboration

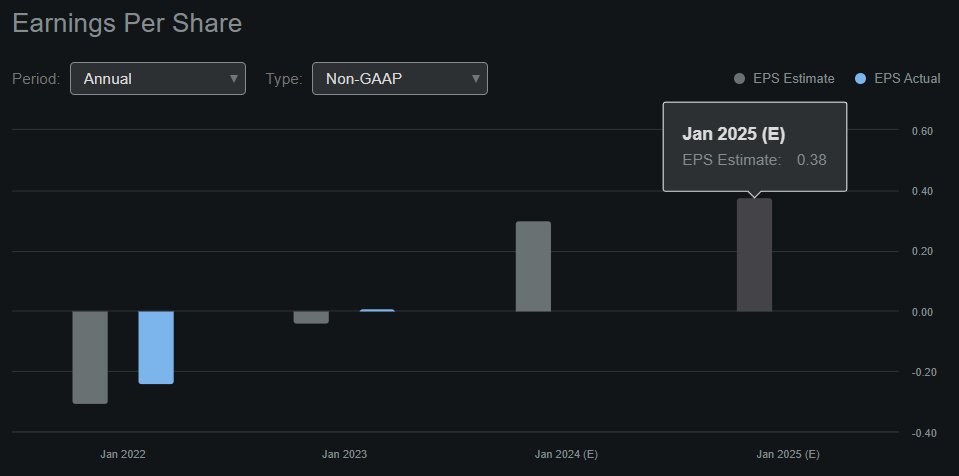

Moreover, CXM’s profitability is improving, as measured by its EBIT margins. In fact, for the TTM period, CXM’s EBIT margins are barely negative at -0.6%, and I believe it’ll soon turn that corner into positive EBIT. In fact, analysts expect revenues to grow into 2024 and 2025 at 16.6% and 15.8%, respectively. Also, in 2024 and 2025, they forecast CXM will report EPS of $0.30 and $0.38 for 2024 and 2025, respectively. This paints a picture of a company quickly becoming profitable after reaching and moving beyond its breakeven point.

We can get a feel for CXM’s EBIT for 2025 using these forecasted figures. Currently, the company has 283.9 million diluted shares, which have been increasing over time, and so far in 2023, it has increased by 4.9%. So, let’s say that by 2025, this dilution rate remains, leading to this figure growing to approximately 312.4 million diluted shares in 2025. This would imply a net income of $118.71 million. Then, we can also use the standard 21% tax rate along with CXM’s TTM net interest income of $8.20 million. Hence, I assess CXM’s 2025 EBIT to be $158.47 million. Furthermore, since the company currently trades at a market cap of $4.23 billion, with $628.41 million in cash and just $31.85 million in debt, that implies an enterprise value of $3.63 billion.

Seeking Alpha

For reference, the sector’s forward EV/EBIT ratio is 19.0. Therefore, this would price CXM’s 2025 EBIT at an EV of $3.01 billion, which makes its current EV approximately 20.6% more expensive than the average if we use this valuation metric. However, let’s not neglect that CXM is certainly not average. Gartner estimates CXM’s sector should grow at approximately 9.3% in 2023. Yet, during the same year, CXM is expected to grow 16.6%, 1.8 times greater than the rest of its sector. Thus, there’s an argument to pay a premium for CXM because it seems to be a premium investment in the industry. In fact, I believe such a premium could be greater than it is today, as showcased by the superior growth CXM has compared to the rest of its industry. Hence, I think it’s safe to consider CXM a good “buy” due to its stellar business, innovative AI approach, and relatively attractive valuation multiple.

Investment Thesis Risks

Nevertheless, investors should know that much of CXM’s future is now dependent on AI. This is a rapidly evolving tech, and while it holds a lot of potential, any significant lag on CXM’s part could derail its competitive advantages. Moreover, the SaaS sector, in general, is extremely competitive, ranging from big companies admire Microsoft (MSFT), Salesforce (CRM), and Oracle (ORCL) to smaller consulting firms providing tailored solutions for companies. So it isn’t easy to assure a long-term business moat on CXM, although I’d argue its consistently increasing revenues offer some reassurance.

Lastly, it’s possible that as a tail risk, regulatory risks could hit CXM. As previously noted, AI is rapidly advancing, and it’s uncertain what could happen on the regulatory front. Also, governments could heavily regulate AI and AI applications in a way that limits CXM’s effectiveness or makes it costly, potentially hindering its ongoing margin expansion. Alternatively, regulations could make AI IP difficult to protect or enforce, detracting from its competitive profile.

CXM’s sustained growth over time is reflected in its steadily appreciating shares (TradingView)

Conclusion

Overall, CXM is a prime example of a great business trading at a fair price. Its fundamentals continue strengthening, and the company also holds a sizeable treasury. This gives it strategic value, and its cash position makes it attractive from an M&A point of view. Naturally, speculating about its M&A potential is beyond the scope of this article, but I wouldn’t regulate out consolidation in this sector that could payoff for current shareholders. CXM appears poised for sustained revenue growth and margin expansion even in the standalone company scenario. It is trading at a relatively reasonable EV/EBIT multiple, leading me to believe this is a good investment in the sector and AI.

Q2 2024 Earnings Call Transcript")