primeimages

Introduction

In September, I wrote an article on SA about fruit and vegetable company Seneca Foods (NASDAQ:SENEA) (NASDAQ:SENEB) in which I said that the next two quarters could be challenging due to rising inventories and that high debt levels were starting to become a serious issue.

On November 9, Seneca Foods released its financial results for Q2 FY24 (ended on September 30) and I think they were decent as higher selling prices helped the company boost its FIFO EBITDA margin to 15.2% from 8.7% a year earlier and adjusted net income came in at over $30 million. However, I think that Q3 FY24 financial results are likely to be negatively impacted by the recently announced acquisition of the Green Giant U.S. shelf-stable vegetable product line of B&G Foods (NYSE: BGS) as well as a voluntary recall of mislabeled Hy-Vee Turkey gravy. I’m keeping my rating on the stock at neutral. Let’s review.

Overview of the recent developments

In case you aren’t unfamiliar with Seneca Foods or my earlier coverage, here’s a brief description of the business. The company specializes in the production of packaged fruits and vegetables, and it has a network of 26 processing facilities in the USA. Produce is sourced from more than 1,400 growers and the brands of Seneca Foods include Libby’s Aunt Nellie’s, and Green Valley among others. Canned vegetables usually account for over 80% of revenues and the company’s major market is the USA with more than 90% of sales. There is significant seasonality here as inventory levels typically peak in mid-autumn while sales are the highest during the third quarter of the fiscal year. Inventories tend to achieve their lowest point in the fourth quarter or the beginning of the first quarter of the fiscal year and Seneca Foods usually schedules repair and maintenance activities for the fourth quarter of its fiscal year.

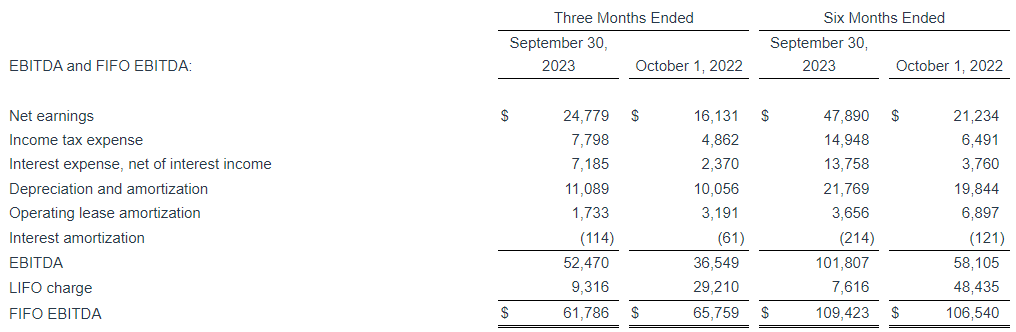

Looking at the Q2 FY24 financial results of the company, net sales went down by 9.3% year on year to $407.5 million as lower sales volumes were only partially offset by higher selling prices. Yet, the latter led to a significant improvement in EBITDA margins using the FIFO method of accounting, leading to a fall in FIFO EBITDA of just 6%.

Seneca Foods Seneca Foods

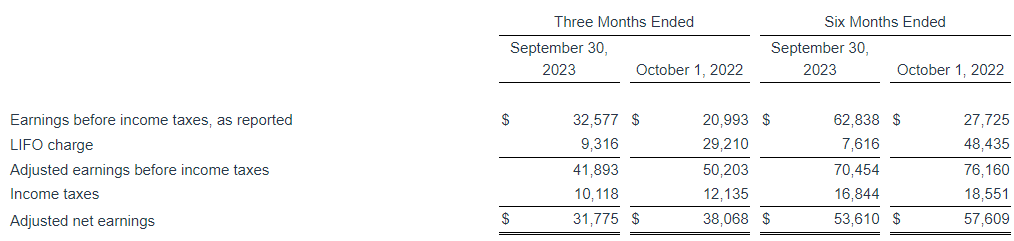

Yet, I find it concerning that interest expenses tripled to $7.2 million as higher interest rates are continuing to bite. The weighted average interest rate on the senior revolving credit facility of Seneca Foods was 6.93% in Q2 FY24 compared to 4.16% a year earlier (see page 10 here).

Seneca Foods

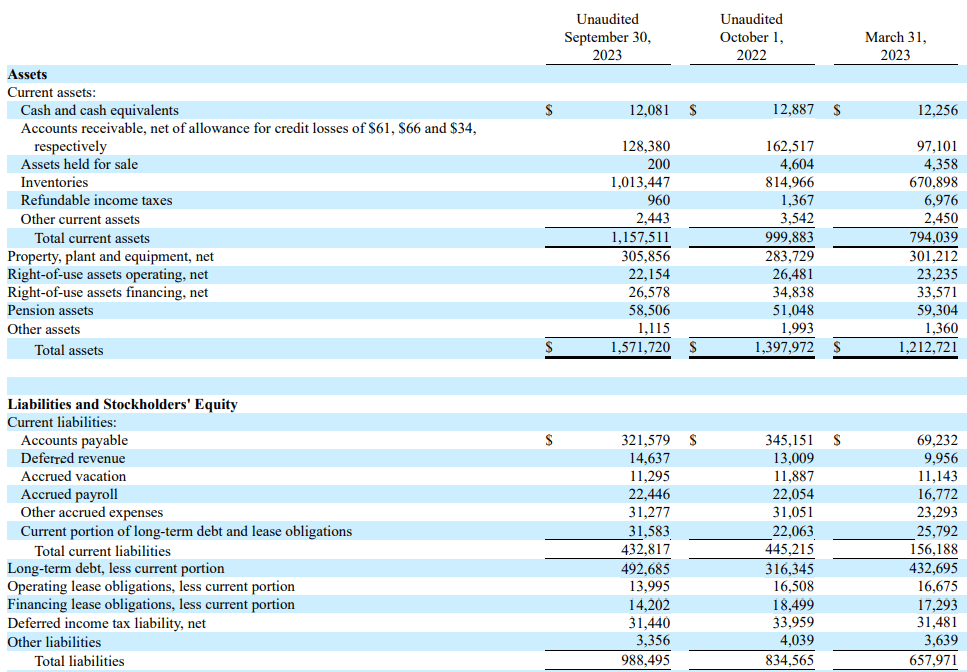

This is also higher than the 6.72% in Q1 FY24 and another issue is that the company’s net debt is growing rapidly. It stood at $526.4 million at the end of September 2023 compared to $344 million a year earlier as inventory levels continued to be high due to inflation.

Seneca Foods

In my view, the net debt is likely to boost advance in Q3 FY24 as Seneca Foods announced on November 8 that it bought the Green Giant U.S. shelf-stable vegetable product line of B&G Foods. While the sum of the deal was not disclosed in the announcement, Seneca Foods revealed in its Q2 FY24 financial report that it paid $55.6 million in cash for this business which was funded from borrowings under its revolver facility (see page 14 here).

Looking at the impact of the Green Giant deal on the income statement of Seneca Foods, I don’t think there are meaningful synergies here and it seems that this business is likely struggling considering B&G Foods booked a $133 million impairment in Q3 2023 (see page 25 here).

B&G Foods

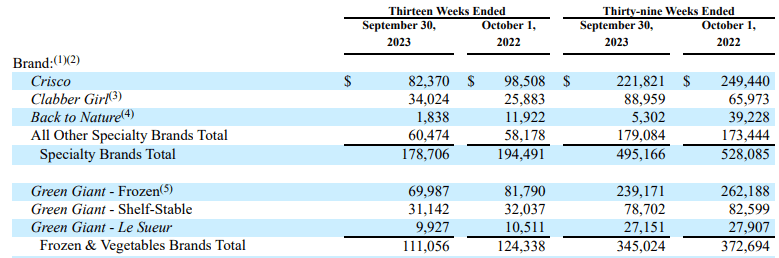

In Q3 2023, the Green Giant shelf-stable business booked net sales of $31.1 million which is 2.8% lower than a year earlier (see page 24 here)

B&G Foods

In my view, a voluntary recall of mislabeled Hy-Vee Turkey gravy in glass jars that was announced on November 21 could also have a minor negative impact on Q3 FY24 financial results. While the recall affects less than 1% of this product sold in Hy-Vee stores, I think that it causes notable reputational damage for the company which could guide to a small short-term fall in sales.

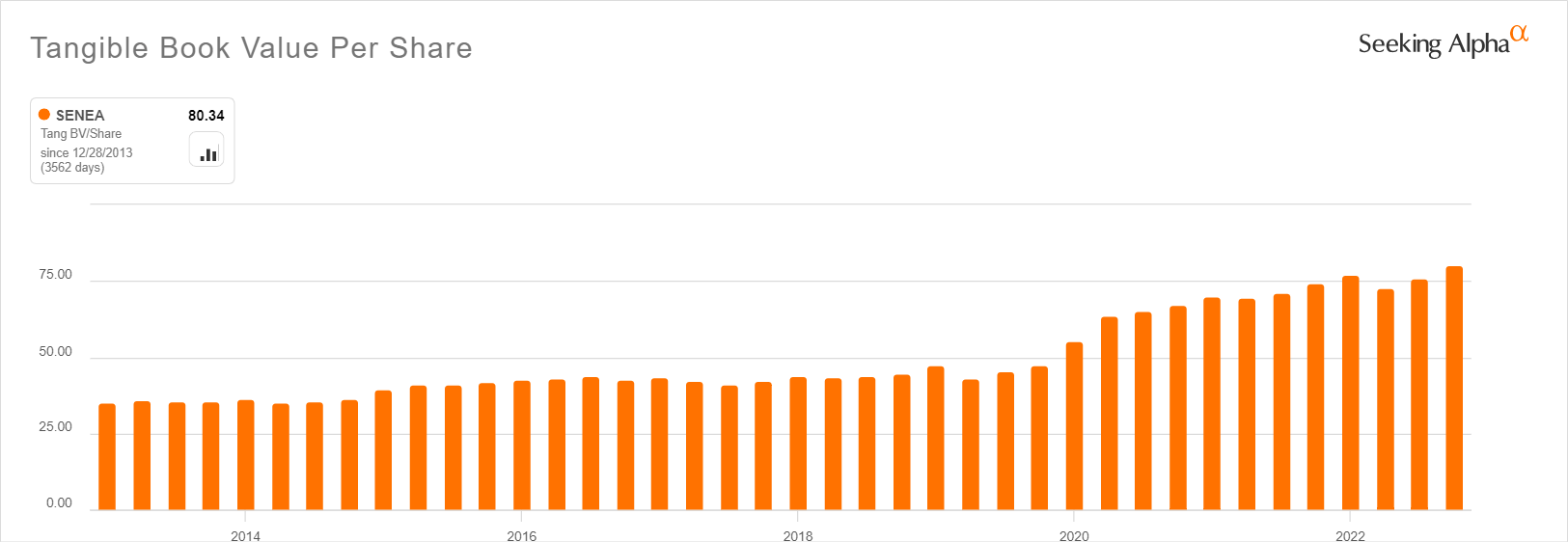

Overall, I think that Q2 FY24 was a strong quarter for Seneca Foods as it was able to pass on cost increases to customers with a just moderate decrease in sales. That being said, I don’t think that this is sustainable as the EBITDA margin of the company has historically been in the single digits. In addition, I’m growing increasingly concerned by the rising net debt level in today’s high interest rate environment. This is likely to become an even greater issue with the purchase of the Green Giant U.S. shelf-stable vegetable product line and could negatively impact the share price in the near future if Seneca Foods shifts its focus to strengthening its balance sheet. The company doesn’t pay dividends but it typically makes large share buybacks during strong years and in Q2 FY24 it invested $17 million in share repurchases (see page 24 here). This has pushed the tangible book value per share to just above $80.

Seeking Alpha

Investor takeaway

The financial results of Seneca Foods for Q2 FY24 were stronger than I expected as the company was able to pass cost increases on to consumers, but I doubt the high margins are sustainable. While Seneca Foods is valued at less than 0.6x tangible book value, I think it could become a value trap as rising net debt levels could limit share repurchases. In addition, I’m not thrilled with the acquisition of the Green Giant U.S. shelf-stable vegetable product line, and I continue to think that risk-averse investors should avoid this stock.

Q2 2024 Earnings Call Transcript")